Inside Circle’s Stablecoin Economics

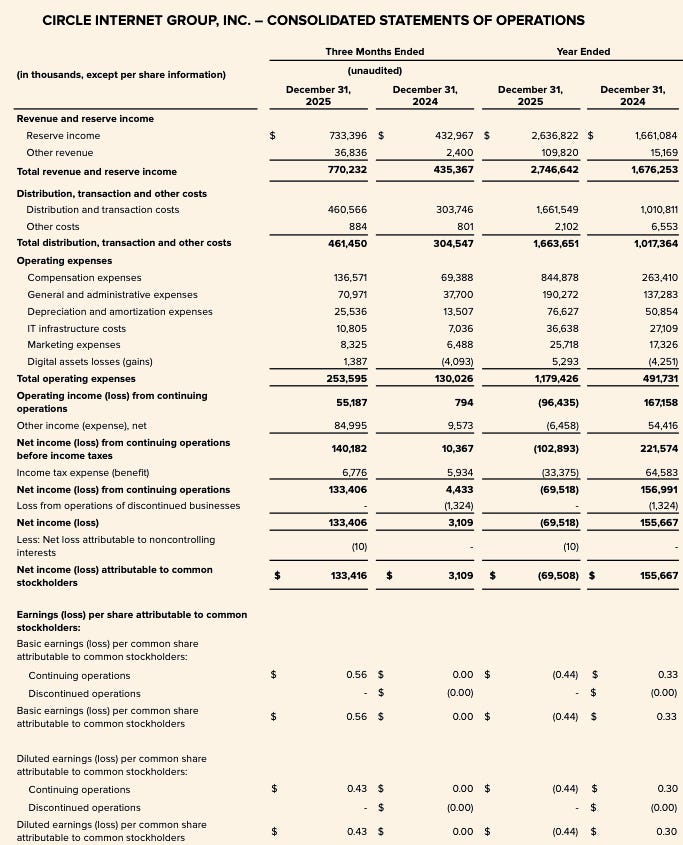

Circle should still be understood primarily as a reserve-income business, not yet as a scaled software or payments-fee platform. Its earnings model remains closely tied to stablecoin balances, short-duration interest rates, and the portion of reserve income retained after substantial distribution payments. FY2025 illustrates that clearly: reserve income accounted for $2.637 billion of $2.747 billion in total revenue and reserve income, while other revenue contributed only $110 million. The company’s near-term financial profile therefore remains driven mainly by average USDC in circulation, realised reserve yields, and the economics of partner revenue-sharing arrangements, particularly with Coinbase.

FY2025 showed strong growth in headline revenue, with total revenue and reserve income increasing to $2.747 billion from $1.676 billion in FY2024. Reserve income rose to $2.637 billion from $1.661 billion, while other revenue increased to $110 million from $15 million. Even so, Circle reported a FY2025 net loss attributable to common stockholders of $70 million and a sharp increase in operating expenses, including $845 million of compensation expense.

The key debate for 2026 is not whether Circle is expanding strategically, but whether that strategic expansion is becoming financially material. The main variables remain whether USDC balances continue to grow, how reserve yields evolve in a lower-rate environment, whether distribution costs remain structurally heavy, and how quickly newer revenue streams such as CCTP, CPN, and USYC-related activities scale relative to the reserve-income base.

At this stage, Circle’s strategic perimeter is clearly widening, but the core investment framework remains unchanged: it is still a rate-sensitive, balance-sensitive financial infrastructure company whose earnings are dominated by reserve income rather than by diversified platform monetisation.

Circle Overview

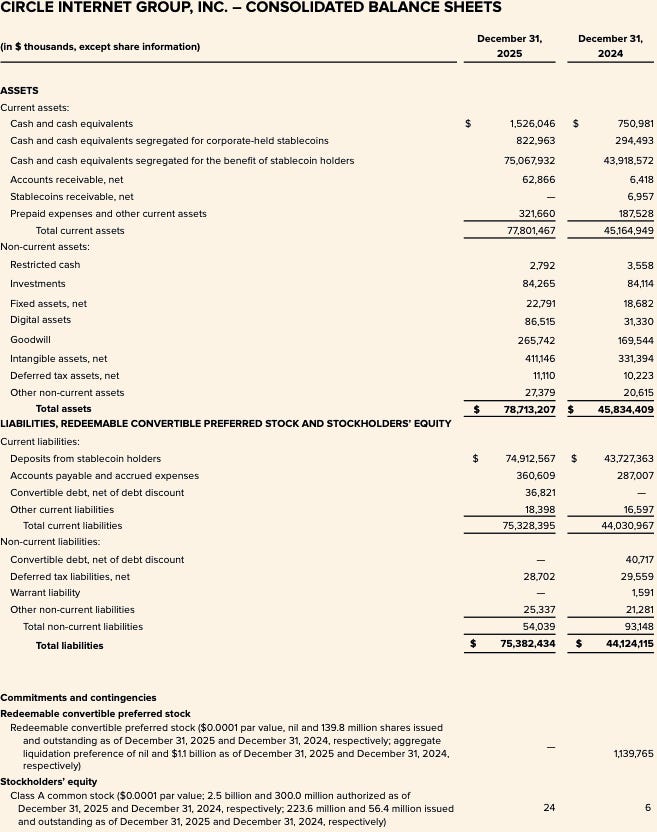

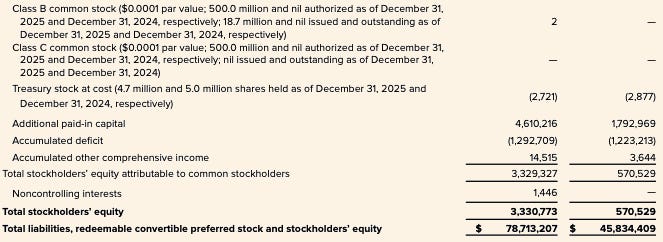

Circle is a publicly listed financial technology company whose equity trades on the NYSE under the ticker CRCL. The company filed its FY2025 Annual Report on Form 10-K for the period ended December 31, 2025 on March 9, 2026. Circle’s FY2025 balance sheet reported $74.9 billion of “deposits from stablecoin holders,” highlighting that the company’s economic core remains tied to the scale and management of reserve-backed stablecoins rather than to a traditional software-only model.

Analytically, Circle can be framed across four layers. First, it is a stablecoin issuer, principally through USDC and EURC, with liabilities linked to outstanding stablecoins and segregated reserve assets held for users. Second, it is a reserve-income business, monetising reserve assets through interest and dividend income. Third, it is building a developer, payments, and infrastructure layer intended to increase the utility and transaction density of its stablecoins. Fourth, it is assembling a broader strategic stack around an “internet financial system,” including Arc, the Circle Payments Network (CPN), and tokenised asset infrastructure. However, disclosed results indicate that the financially material engine today remains the reserve-income model rather than a scaled software or transaction-fee business. Circle reported FY2025 total revenue and reserve income of $2.747 billion, of which reserve income contributed $2.6368 billion, leaving only a relatively modest share attributable to non-reserve activities.

This distinction is important for valuation. Circle’s strategic narrative is clearly broadening, but the revenue mix still argues against treating the company primarily as a software-platform re-rating story. In Circle’s earlier disclosure set, “other products” represented only 1% of total revenue in 2024, although management separately indicated other revenue accelerated materially in 2025, with Q4 2025 other revenue of $37 million, up $34 million year over year. That supports a directionally positive platform narrative, but it does not yet displace the central role of reserve balances, reserve yields, and partner economics in shaping earnings power.

A further strategic pillar is regulatory architecture. Circle disclosed that it received conditional approval from the Office of the Comptroller of the Currency in December 2025 to establish a national trust bank, referred to as First National Digital Currency Bank, N.A. Management has framed this as an important step in strengthening USDC infrastructure and potentially expanding regulated custody and reserve-management capabilities. Analytically, this could improve perceived regulatory durability and institutional confidence in reserve governance, but it should not yet be viewed as a disclosed earnings driver.

Business Model and Economics

Circle’s business model is driven primarily by the interaction of two variables: stablecoins in circulation and the yield earned on reserve assets. The company explicitly defines reserve income as a function of reserve balances and the reserve return rate. In FY2025, Circle reported $2.6368 billion of reserve income, up from $1.6611 billion in FY2024. By contrast, other revenue totaled $109.8 million in FY2025, compared with $15.2 million in FY2024, with subscription and services revenue of $84.8 million representing the largest non-reserve component in FY2025. This confirms that Circle’s earnings profile remains overwhelmingly sensitive to interest rates and balance growth, even as ancillary revenue streams begin to scale from a relatively small base.

The reserve base is managed conservatively by design. Circle disclosed that, as of June 30, 2025, approximately 87% of USDC reserves were held in the Circle Reserve Fund, a government money market fund governed under Rule 2a-7, managed by BlackRock, and custodied at BNY. The remainder was held as cash in accounts maintained for the benefit of USDC holders, primarily at global systemically important banks. Circle also states that its reserve management framework is designed to align with relevant regulatory requirements, including NYDFS guidance for USDC and MiCAR-related reserve requirements for EURC. The implication is that reserve construction is optimized first for liquidity, principal preservation, transparency, and regulatory compliance, rather than for yield-maximizing portfolio risk.

Circle’s economics are also shaped heavily by distribution arrangements, most notably with Coinbase and other ecosystem partners. While reserve income is recorded on a gross basis, the company makes substantial downstream payments through distribution and transaction costs. Prior disclosures make clear that these costs are tied to reserve income generation and platform balances, meaning that a meaningful portion of gross reserve economics is contractually shared rather than fully retained. This is visible in the cost structure: in FY2025, Circle reported revenue less distribution costs (RLDC) of $1.083 billion on $2.747 billion of total revenue and reserve income, implying that a large share of gross monetization is paid out through the distribution layer before operating expenses.

This point is critical for modeling. Circle is not simply a pure-play beneficiary of higher interest rates or larger USDC balances, because growth in reserve monetization does not translate one-for-one into retained profitability. In Circle’s earlier sensitivity disclosure, a +100 basis point change from an average reserve yield of 4.26% as of June 30, 2025 implied an estimated $618 million change in reserve income, but also a $315 million change in distribution and transaction costs. This suggests that a substantial portion of gross reserve upside is shared away, with only the residual flowing through to RLDC before operating expenses. For institutional analysis, RLDC is therefore a more useful intermediate earnings measure than reserve income alone, although it remains inherently sensitive to rates and balances.

Reported earnings quality in FY2025 was also materially affected by non-core and non-cash items. Circle disclosed a FY2025 net loss from continuing operations of $70 million, despite reporting $582 million of adjusted EBITDA, with the gap driven in part by unusually large stock-based compensation linked to IPO-related vesting conditions. In its FY2025 earnings release, Circle stated that results were significantly affected by $424 million of stock-based compensation related to IPO vesting. In the filing, Circle further disclosed $423.8 million of stock-based compensation expense associated with the relevant RSU performance condition becoming probable upon the commencement of NYSE trading. This means GAAP net income is not the cleanest lens through which to assess underlying unit economics or earnings power.

The most important reason is Circle’s arrangement with Coinbase, which remains one of the most significant and underappreciated aspects of its business model.

When USDC launched in 2018, Circle and Coinbase formed a joint consortium to govern the stablecoin. That structure was dissolved in 2023, with Circle assuming full control over issuance. However, Coinbase retained a highly favorable revenue-sharing arrangement.

Under this agreement, Coinbase receives 100% of reserve income on USDC held on its own platform and 50% of reserve income generated elsewhere. In 2024, $908 million of Circle’s $1.01 billion in total distribution costs was paid to Coinbase. In practical terms, this means that roughly $0.54 of every dollar Circle earned was paid out to a company that neither issues USDC nor manages its reserves. By early 2025, Coinbase held 22% of total USDC supply, up from 5% in 2022. As the share of USDC concentrated on Coinbase continues to rise, Circle’s payout burden increases accordingly.

The broader analytical conclusion is that Circle should, at present, be viewed as a rate-sensitive financial infrastructure company built around a stablecoin-led reserve income engine, rather than as a software platform whose economics are primarily driven by subscription or transaction revenue. The platform optionality is becoming increasingly visible, particularly through Arc, CPN, and the expansion of non-reserve revenue streams. However, Circle’s disclosed FY2025 revenue mix still supports a framework centered on reserve balances, reserve yield, and distribution-sharing mechanics. Until non-reserve revenue becomes materially more significant as a share of the total, the reserve income model will remain the primary driver of Circle’s earnings sensitivity and the central issue in its valuation debate.

USDC and EURC Deep Dive

The regulatory backdrop for Circle’s flagship stablecoins improved materially in 2025. In the United States, the White House states that President Donald Trump signed S. 1582, the GENIUS Act, into law on July 18, 2025, creating a federal framework for payment stablecoins. Reuters similarly reported that the law requires issuers to back stablecoins with liquid assets such as U.S. dollars and Treasury bills and to disclose reserve composition monthly. Circle’s FY2025 10-K describes the GENIUS Act’s reserve-asset expectations, including cash, deposits, short-term Treasuries, and repo or reverse repo, as broadly consistent with Circle’s existing reserve management practices for USDC. Analytically, that alignment reinforces Circle’s regulation-first positioning, although the company’s earnings power is still shaped more by distribution agreements and market structure than by regulation alone.

USDC

USDC remained the core economic engine of the Circle model entering 2026. Circle reported USDC in circulation of $75.266 billion at December 31, 2025 in its FY2025 10-K. Circle’s USDC product page later showed $79.2 billion in circulation as of March 16, 2026. On that basis, USDC circulation increased by roughly $3.9 billion, or about 5.2%, between year-end 2025 and mid-March 2026. That is not an explosive step-change, but it does indicate continued net expansion after an already strong 2025 base.

Circle’s own FY2025 disclosures point to a very strong growth year for USDC. In Q4 2025, the company reported that USDC in circulation rose 72% year over year to $75.3 billion, while USDC on-chain transaction volume rose 247% year over year to $11.9 trillion. For the full year, Circle reported average USDC in circulation of $64.870 billion, up from $33.342 billion in FY2024, while the FY2025 reserve return rate was 4.1%, down from 5.0% in FY2024. The key inference is that the company’s 2025 revenue expansion was driven more by balance growth than by yield tailwinds, since reserve return rate moved lower year over year rather than higher.

Circle also disclosed operating indicators that suggest USDC is a high-velocity monetary instrument rather than a static store of collateral. Management reported FY2025 USDC minted of $257.5 billion and redeemed of $226.1 billion, alongside a year-end stablecoin market share of 28% based on third-party market-cap data and 6.8 million meaningful wallets at period end, using Circle’s own definition. The scale of mint and redeem activity relative to the end-period supply suggests significant transactional churn, likely linked to exchange settlement, liquidity routing, collateral management, and DeFi-related flows, rather than a simple buy-and-hold reserve asset profile. Circle does not, however, publicly provide a clean segmentation of USDC usage across these categories, which limits precision in attribution.

The payments narrative around USDC is becoming more credible, although it is still early relative to the reserve-income model. Visa has publicly launched USDC settlement capabilities in the United States for selected issuer and acquirer partners, enabling settlement of certain VisaNet obligations in USDC on supported blockchains and outside traditional banking hours. Circle has highlighted this as evidence that USDC can function as a continuous settlement asset rather than only as a crypto-native trading instrument. The analytical significance is high even if the current scale remains small relative to Visa’s total network volumes: this is one of the clearest public signals that USDC is being positioned as part of real-world back-office payments infrastructure.

Partner-led distribution into consumer and SMB-facing ecosystems is also widening. Circle announced a partnership with Intuit on December 18, 2025 to enable USDC capabilities across products including TurboTax, QuickBooks, and Credit Karma. Strategically, this strengthens the case that Circle is trying to move USDC beyond trading venues and crypto-native users into mainstream financial workflows. Economically, however, the monetisation path remains opaque. Circle has not disclosed pricing, take rates, or revenue-sharing mechanics tied to that integration, so the existence of distribution progress should not yet be confused with proof of high-margin payments revenue.

A separate strategic issue is market structure. Circle and Polymarket announced on February 5, 2026 that Polymarket would transition in coming months from bridged USDC on Polygon (USDC.e) to native USDC. That development matters because it illustrates Circle’s broader effort to reduce dependence on bridged liquidity and to increase the footprint of natively issued USDC across chains. Native issuance improves redemption clarity, reduces some operational complexity around wrapped or bridged representations, and is more aligned with a regulation-first model. At the same time, the need for such transitions underlines a structural challenge for stablecoins: fragmented liquidity across bridges and chains remains an adoption friction, not just a technical footnote.

Taken together, USDC is best characterised as a hybrid instrument. It is, first, a major exchange and venue settlement asset; second, a high-velocity on-chain dollar used for collateral, liquidity routing, and crypto market plumbing; and third, an emerging institutional settlement rail in selected integrations. The evidence for payments-rail growth is improving, particularly through Visa settlement, Intuit integration, and Circle’s broader infrastructure build-out. But the dominant disclosed economic driver for Circle remains reserve income on USDC reserves rather than explicit transaction-fee monetisation from payments activity.

EURC

EURC is strategically important even if it remains small in direct economic terms. The European regulatory backdrop is especially relevant here. MiCA, Regulation (EU) 2023/1114, entered into force in 2023, with the rules for asset-referenced tokens and e-money tokens applying from June 30, 2024, and the broader regime becoming fully applicable from December 30, 2024. That sequencing matters because euro-denominated stablecoins became “regulatory-gradable” earlier than many adjacent cryptoasset services, improving the ability of regulated issuers and exchanges to support compliant euro stablecoin products with greater institutional confidence.

Circle reported EURC in circulation of 309,608,590 at December 31, 2025. By March 16, 2026, Circle’s EURC page showed €382.8 million in circulation. That implies growth of roughly €73 million, or about 23.6%, from year-end to mid-March. In absolute terms this remains small relative to USDC, but the growth rate is meaningful and suggests EURC is gaining traction from a still modest base.

The broader euro stablecoin market is still very small. Reuters reported in September 2025, citing figures released by the Bank of Italy, that euro-denominated stablecoins totalled only about $620 million, versus roughly $300 billion of global stablecoin issuance at the time. Even allowing for subsequent growth, Circle’s reported €382.8 million EURC circulation by March 2026 suggests that EURC is likely one of the dominant euro stablecoins by supply. That said, I would avoid stating a precise market share unless using a fresh, high-quality consolidated market dataset as of March 2026, which is not evident from the sources reviewed here.

Circle positions EURC as MiCA-compliant, with availability across Avalanche, Base, Ethereum, Solana, and Stellar, and states that it publishes monthly attestations. Strategically, EURC’s value to Circle likely exceeds its current direct financial contribution. It helps anchor Circle’s European regulatory posture, supports euro-dollar on-chain workflows alongside USDC, and gives the company optionality if euro stablecoin policy priorities intensify further in Europe. Reuters reporting through late 2025 also indicates that European institutions and policymakers were increasingly focused on building alternatives to U.S.-dominated stablecoin infrastructure, which supports that optionality argument.

Over the next 12 to 24 months, EURC is more plausibly viewed as an enabling layer than as a standalone profit driver. Its base remains below €0.5 billion, and Circle does not separately disclose EURC-specific revenue. For EURC to become financially meaningful, it likely needs three things: materially larger euro-denominated float, evidence of payments and treasury adoption beyond crypto-native capital markets, and distribution pathways that avoid recreating the same heavy economic sharing that characterises parts of the USDC model. In other words, EURC may already matter strategically, but it does not yet appear financially central.

2025 Financial Analysis and Key Metrics

Circle’s FY2025 financial profile reinforces the view that the company remains, first and foremost, a reserve-income business. The company reported FY2025 total revenue and reserve income of $2.747 billion, up from $1.676 billion in FY2024. That FY2025 figure consisted of $2.637 billion of reserve income and $110 million of other revenue, versus $1.661 billion and $15 million, respectively, in FY2024. The year-on-year step-up was therefore driven overwhelmingly by expansion in reserve income rather than by a broad-based mix shift toward software or transaction-fee monetisation.

Cost structure is equally important to the underwriting framework. Circle reported distribution and transaction costs of $1.662 billion in FY2025, up from $1.011 billion in FY2024. Operating expenses rose to $1.179 billion from $492 million, with compensation expense of $845 million versus $263 million a year earlier. This confirms that the gross earnings power created by higher reserve income is materially shared out through partner economics and then further absorbed by a sharply higher operating cost base.

A useful way to frame operating leverage is through revenue less distribution costs (RLDC) rather than top-line revenue alone. Circle’s disclosed RLDC was $1.083 billion in FY2025, up from $659 million in FY2024, while RLDC margin remained 39% in both years. That flat margin is important: it suggests that distribution costs scaled broadly in line with reserve-income expansion, limiting the degree to which higher rates and larger balances translated into structurally better retained economics. Put differently, Circle showed growth, but not meaningful improvement in the core share of economics it retains after distribution.

The clearer operating leverage signal appears in management’s adjusted framing rather than in headline GAAP results. Circle disclosed FY2025 adjusted operating expenses of $508 million and guided to FY2026 adjusted operating expenses of $570 million to $585 million under a revised definition beginning in Q1 2026. That guidance implies Circle is planning to continue investing into growth initiatives rather than shifting into a near-term harvest mode. In other words, even if reserve-income conditions remain supportive, management appears willing to carry a higher expense base to build out products, infrastructure, and distribution.

The balance sheet also supports a specific interpretation of the business model. As of December 31, 2025, Circle reported $75.068 billion of cash and cash equivalents segregated for the benefit of stablecoin holders and $74.913 billion of deposits from stablecoin holders. That structure is consistent with a reserve-backed issuance model built around segregated balances rather than a conventional lending-based balance-sheet model. Analytically, this makes Circle look structurally closer to a narrow spread business than to a high-take-rate fintech, with the important qualification that the reserves are described as held for the benefit of token holders and intended to be bankruptcy remote under Circle’s disclosed structure.

Q1 2026 Preview and FY2026 Bull, Base, Bear

The rates backdrop entering Q1 2026 is less favourable than the peak conditions Circle enjoyed earlier in the cycle. The effective federal funds rate was 3.64% on March 16 and March 17, 2026, while SOFR was 3.65% on March 17, 2026. Circle’s own sensitivity framework uses an average yield of 3.64% in December 2025 as a reference point. The implication is that the reserve-return environment in early 2026 remains well below FY2024’s disclosed 5.0% reserve return rate and is closer to late-2025 levels, meaning balance growth has to do more of the work if Circle wants to keep reserve income expanding.

The starting point for Q1 2026 is at least directionally constructive on balances. Circle disclosed USDC circulation of $79.2 billion as of March 16, 2026, above the $75.266 billion reported at year-end 2025. EURC also rose from 309.6 million at year-end to €382.8 million by March 16, 2026. That setup suggests Q1 average stablecoin balances likely improved versus Q4 exit levels, partially offsetting the lower-yield regime.

Management guidance for FY2026 points to continued mix diversification, but not a fundamental change in the economic model. Circle guided to other revenue of $150 million to $170 million, RLDC margin of 38% to 40%, and adjusted operating expenses of $570 million to $585 million. The signal here is twofold: first, management expects non-reserve revenue to grow; second, even on its own guidance, those revenues remain small relative to the reserve-income engine.

Bull case. In the bullish scenario, USDC circulation continues to expand through Q1 and Q2, supported by growing institutional settlement use, higher on-chain velocity, and incremental distribution wins. In that outcome, reserve income can remain resilient even if realised yields stay around late-2025 and early-2026 short-end levels. Distribution costs would also rise, but retained economics after distribution could still grow enough to absorb the higher operating-expense plan while keeping margins within or near guided levels. This is essentially a “float growth offsets rate compression” case. Supported by current balance trends and the still-expanding ecosystem, it is plausible but still dependent on continued volume and adoption momentum.

Base case. In the base case, USDC circulation growth moderates to low single digits sequentially as trading activity and DeFi usage normalise. Reserve return remains anchored around the mid-3% short end, broadly in line with EFFR and SOFR. In that setup, reserve income is likely stable to modestly higher depending on average balances, but distribution costs remain structurally high because the partner-sharing model does not go away. RLDC margin therefore stays within the company’s guided 38% to 40% range, with modest top-line progress but limited structural margin expansion.

Bear case. In the bearish scenario, USDC circulation stalls or declines because of risk-off flows, exchange-driven outflows, or market-share pressure, while rates drift lower from already reduced levels. Under Circle’s own sensitivity framework, lower yields would reduce reserve income and mechanically reduce some distribution costs, but the net effect would still be negative to RLDC. That would matter more because Circle is entering FY2026 with a higher planned expense base, meaning weaker float and weaker yields would expose the business more directly to partner concentration and operating-cost rigidity.

Strategic Positioning and Competition

Circle is best underwritten as a regulated digital-currency network operator with two layers: an issuer and reserve-management core that is financially dominant today, and a broader application, interoperability, and developer-services perimeter that is strategically important but not yet economically dominant. That distinction matters because Circle’s valuation, earnings sensitivity, and risk profile remain closely tied to monetary policy and stablecoin market structure until non-reserve revenue becomes materially larger.

The most important current example of strategic optionality is the Circle Payments Network (CPN). Circle launched the concept in April 2025 and disclosed that, as of February 20, 2026, 55 financial institutions were enrolled, 74 were in eligibility review, and annualised transaction volume on a trailing-30-day basis had reached $5.7 billion. These are meaningful early indicators of network formation and institutional interest. However, without disclosed take rates, revenue contribution, or margin profile, CPN is still easier to justify strategically than financially.

A second credible non-reserve vector is interoperability tooling. Circle disclosed that it launched CCTP V2 in March 2025 and that the fast transfer feature can generate transaction fees when customers elect it. This is one of the stronger non-reserve monetisation paths because it prices a specific technical capability rather than simply hoping usage eventually converts into value. Even so, Circle’s disclosed FY2025 transaction revenue line was still small, so the contribution remains immaterial relative to reserve income at this stage.

Circle’s acquisition-led adjacency through Hashnote and USYC is also strategically notable. Circle has described USYC as an on-chain representation of money market fund shares intended primarily for collateral use in digital asset markets, and has disclosed that it earns fees including performance fees. This is a sensible adjacency to USDC because it serves yield-bearing collateral and margining needs that stablecoins alone do not fully address. But the market still lacks separate public disclosure for USYC assets, revenue, or profitability, so it remains more of a strategic building block than a fully underwritable standalone driver.

On competition, Circle’s most direct dollar-stablecoin rival remains Tether. Reuters reported in February 2026 that USDT had about $184 billion in issue, underscoring Tether’s substantial scale advantage. Circle’s differentiation remains clear, though: public-company disclosure, reserve-asset constraints more closely aligned with emerging regulation, and stronger positioning with regulated institutions and payment networks. In that sense, Circle’s competitive edge is less about absolute scale than about institutional credibility and regulatory legibility.

A separate competitor is PayPal’s PYUSD, which PayPal announced on March 17, 2026 would be made available in 70 markets worldwide. PYUSD is strategically relevant because it is embedded inside a global consumer and merchant payments distribution network, which is a very different go-to-market advantage from Circle’s exchange and infrastructure-heavy footprint. Circle’s current advantage remains deeper USDC liquidity, larger scale, and stronger crypto-market integration; PYUSD’s differentiation is native wallet and merchant distribution within a mainstream payments platform.

In Europe, the competitive picture may become more challenging over time. Reuters reported that a group of major European banks, including ING, UniCredit, and later BNP Paribas, formed a company to launch a euro stablecoin in the second half of 2026, while policymakers have openly discussed strengthening euro-denominated digital money to counter dollar dominance. That is a meaningful medium-term competitive threat to EURC because bank-led euro stablecoins could combine regulatory credibility with embedded corporate and banking distribution. As of March 2026, however, this remains more of a future competitive risk than an immediate supply-side displacement.

Conclusion

Circle’s FY2025 results still support viewing the company primarily as a reserve-income business, with earnings driven far more by stablecoin balances, reserve yields, and partner economics than by software or payments monetisation. While USDC and EURC continue to expand and newer initiatives such as CCTP, CPN, and USYC improve the strategic narrative, these businesses are not yet financially material relative to the reserve-income base. As a result, the core underwriting framework remains centered on float growth, interest-rate sensitivity, and the structural weight of distribution costs, especially those linked to Coinbase.

Sources:

Cover Artwork

Jankówka

Józef Mehoffer, c. 1913

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.