Venture Capital: From Doriot to the Power Law

The history of venture capital is fundamentally a history of the institutionalization of risk. It is a story that begins not in the silicon-saturated offices of modern Sand Hill Road, but in the industrial heart of pre-war France and the hallowed, buttoned-up classrooms of Harvard Business School. The metamorphosis of this industry, from the paternalistic, institution-building vision of Georges Doriot to the aggressive, mathematical outlier-hunting of the modern Silicon Valley power-law model, represents more than just a shift in financial tactics.

It reveals a profound evolution in how human society identifies talent, allocates capital to the unknown, and ultimately constructs the future. By tracing this arc through the primary lenses of Spencer E. Ante’s Creative Capital and Sebastian Mallaby’s The Power Law, we uncover the shifting dynamics of power between those who possess ideas and those who possess the means to realize them.

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. To explore it, contact: office@insights4.vc

The Epistemology of Risk

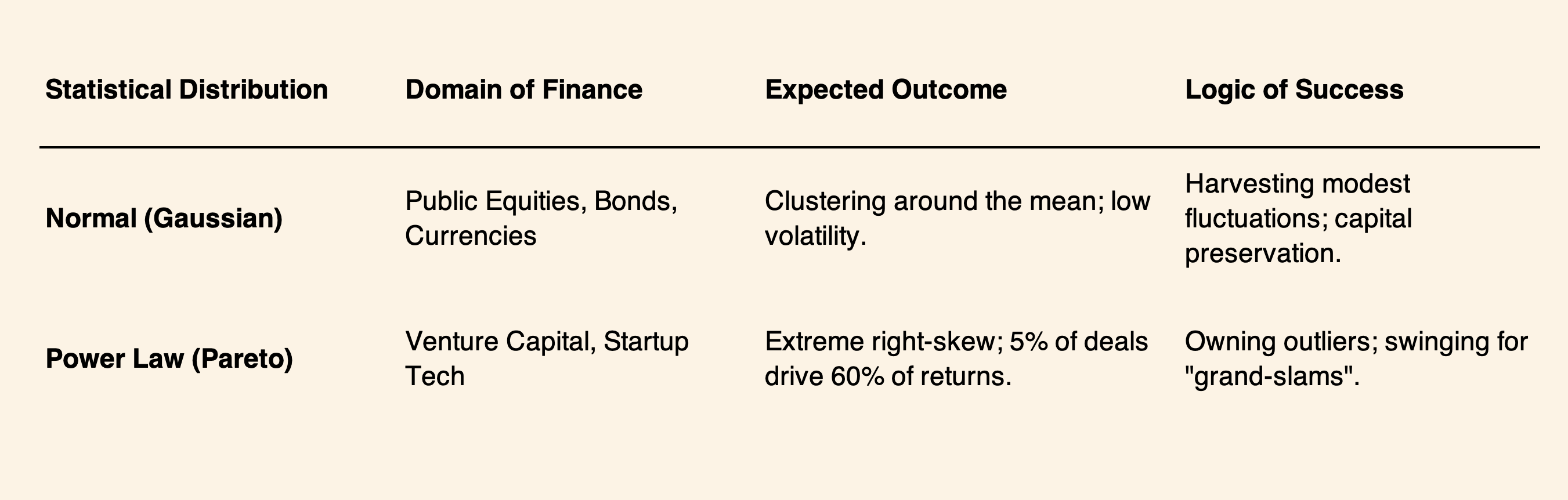

The foundational logic of venture capital rests upon a radical departure from traditional finance. Most financial domains, be they currency markets, bond trading, or the public stock exchanges, operate within the safe confines of the normal distribution. In these systems, observations cluster around a mean, and extreme “tail” events are statistically rare enough to be managed as outliers. A bond trader seeks steady yields; a hedge fund manager celebrates a portfolio that doubles in three years as a spectacular achievement. Venture capital, however, is a “grand-slam business” rather than a home-run business. It functions in a world where the outliers do not just influence the average, they are the average.

The power law, as Mallaby delineates, is the pervasive rule where winners advance at an accelerating, exponential rate. In a typical venture fund, a tiny minority of investments, perhaps only 5 percent of the capital deployed, generates upwards of 60 percent of the total returns. This mathematical reality dictates a unique epistemology: most ideas are unimportant, and only the improbable ones carry true value. This requires a specific type of investor, one who is comfortable with a 90 percent failure rate if the remaining 10 percent can fundamentally alter the human predicament.

The evolution of venture capital is the story of moving from a qualitative, mentorship-based approach to this quantitative, mathematical embrace of the outlier. As Vinod Khosla famously observed, progress depends upon the “unreasonable man”. This philosophy was evident when Patrick Brown, a Stanford geneticist, approached Khosla in 2010 with a “ridiculous” slide deck proposing the total elimination of the meat-industrial complex via plant-based heme. Khosla’s response, “That’s impossible!” followed by a $3 million check, encapsulated the modern venture mindset: if there is a one-in-a-hundred chance that an idea works, and that idea has a trillion-dollar market, the risk is not just acceptable; it is mandatory.

Industrial Roots and the Birth of ARD

To understand the modern “sovereign founder” era, one must first reconcile with the paternalistic origins of the industry embodied by Georges Doriot. As Spencer Ante meticulously details in Creative Capital, Doriot was a product of the French industrial elite. His father, Auguste Doriot, was a pioneer at Peugeot who helped build one of the first automobiles and won the 1894 Paris-Rouen Trial, a grueling test of mechanical reliability. This upbringing instilled in the younger Doriot an obsession with “the resourceful man”, the individual who could not only conceive an idea but make it practical.

Doriot’s arrival in America in 1921 led him to Harvard Business School, where he became its most influential professor over a forty-year career. He taught a legendary course called “Manufacturing,” which was less about industrial logistics and more about a philosophy of life and business. Doriot viewed himself as a builder of men. He demanded punctuality, formal dress (”Sport coats are for newspaper boys”), and a commitment to “noble” ideas rather than mere profit.

The formalization of venture capital began in 1946 when Doriot was recruited by a group of New England luminaries, including the presidents of MIT and the Boston Federal Reserve, to lead the American Research and Development Corporation (ARD). The motivation was civic and regional: New England was suffering an industrial decline as textile mills moved South, and there was a perceived “gap” in the capital markets. Banks were too conservative, and the New Deal financial reforms had dampened the risk appetite of wealthy families. ARD was created to solve this imperfection by providing both capital and professional management to unproven, science-based startups.

The Paternalistic Model and the DEC Breakthrough

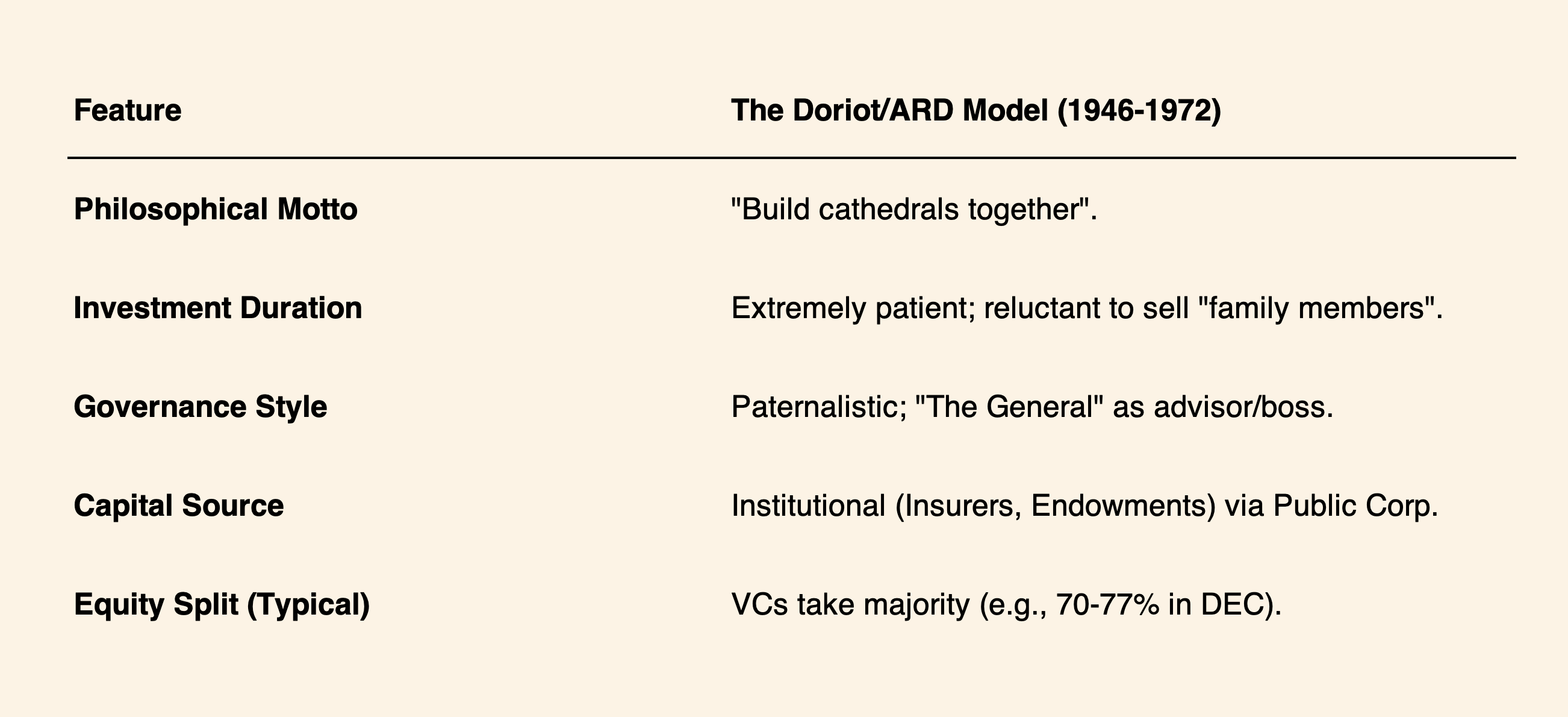

Doriot’s investment style was profoundly different from the hands-off, board-seat-avoiding growth equity of the 21st century. He viewed his portfolio companies as “children” and famously stated that “when you have a child, you don’t ask what return you can expect... you hope they become President of the United States”. This paternalism was institutionalized in the way ARD operated. The firm was structured as a publicly traded closed-end fund, meaning it had permanent capital and faced no redemption pressure, allowing Doriot to be exceptionally patient.

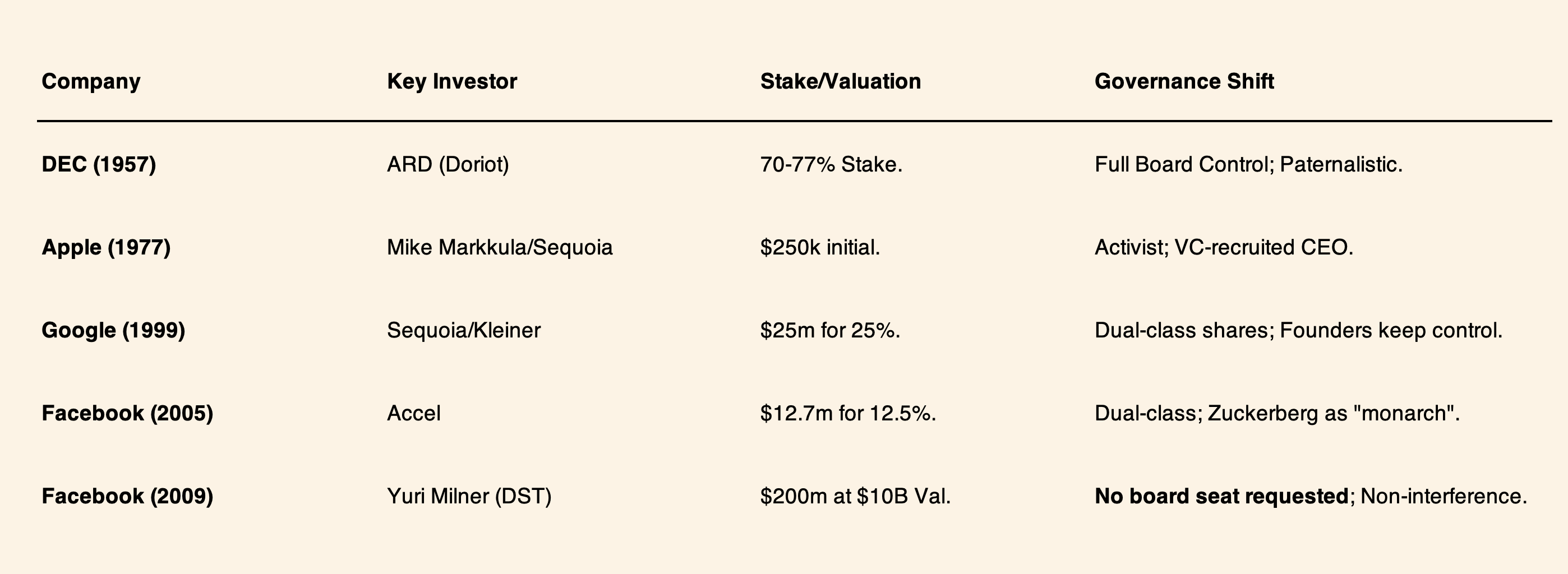

The defining success of the Doriot era was the 1957 investment in Digital Equipment Corporation (DEC). Two young MIT engineers, Ken Olsen and Harlan Anderson, had been rejected by established companies for their idea of building interactive, affordable “minicomputers” that challenged the glass-encased mainframes of IBM. Doriot saw the “resourceful man” in Olsen and authorized a $70,000 investment for a 70 percent equity stake. This deal, which gave ARD nearly total control, would have been viewed as usurious by modern founders, but in the capital-starved 1950s, it was the only path forward.

Over the next fourteen years, Doriot acted as a mentor, father figure, and occasionally a stern taskmaster to Olsen. He advised DEC to present their circuit boards on purple velvet to emphasize their quality and famously expressed displeasure the first time DEC reported a profit, fearing they were not reinvesting enough in R&D. The result was the industry’s first true grand slam: by 1971, ARD’s $70,000 stake was worth $355 million. This single investment accounted for more than half of all the gains generated in ARD’s twenty-five-year history, providing an early, albeit unintended, validation of the power law.

Arthur Rock and the Fairchild Defection

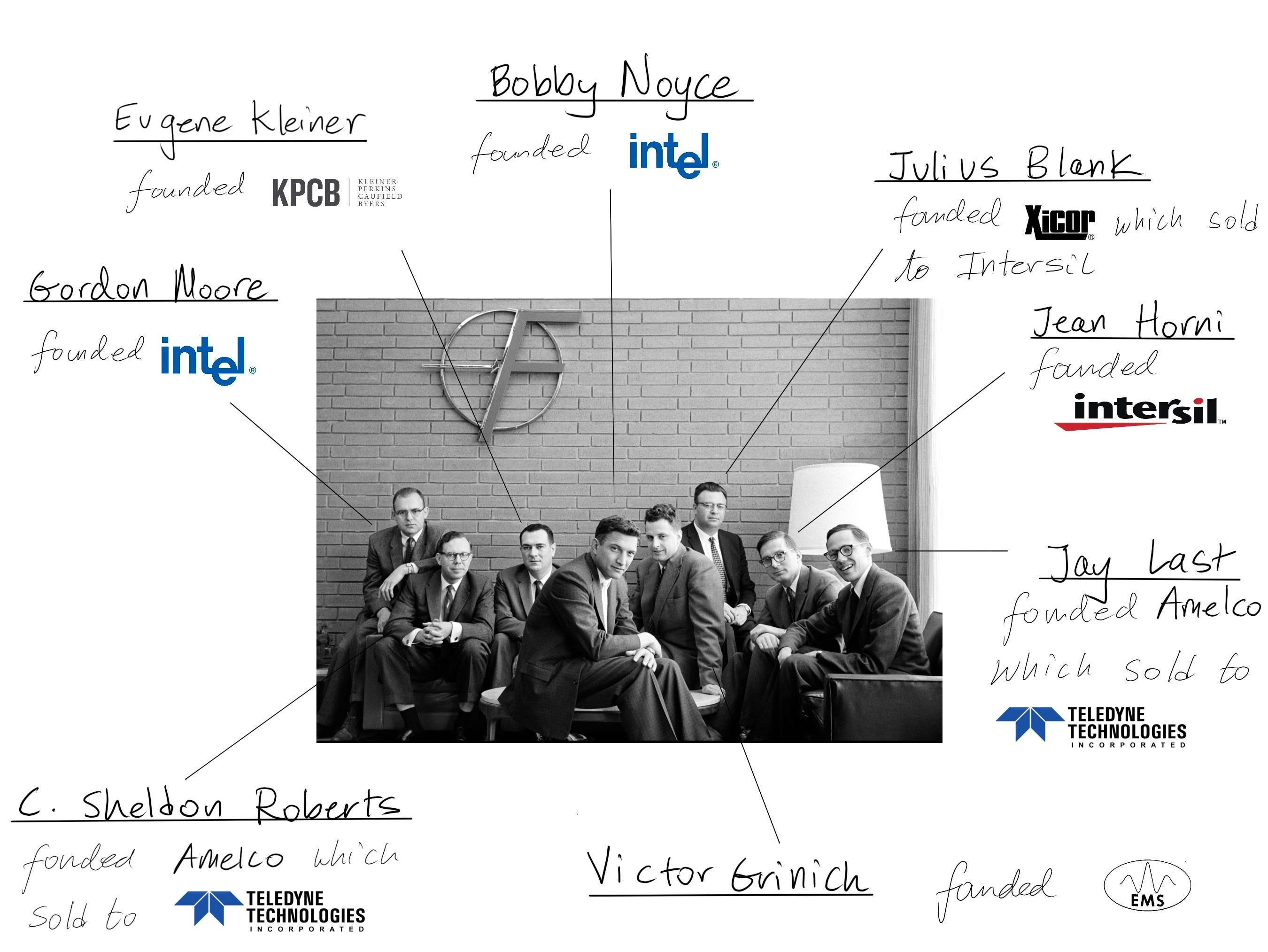

While Doriot was building cathedrals in Boston, a different and more radical form of finance was emerging in the West. The defining moment for what Mallaby calls “liberation capital” occurred in the summer of 1957, the same year as the DEC deal, at Shockley Semiconductor Laboratory in Mountain View, California. William Shockley, a Nobel laureate and the father of the semiconductor, was also a “maniacal despot” who subjected employees to lie detector tests and belittled their intelligence.

We highly recommend Mario Gabriele’s piece on Arthur Rock in The Generalist:

Eight of Shockley’s top PhD researchers, including Gordon Moore and Robert Noyce, resolved to quit. In the 1950s era of the “Organization Man,” such a collective defection was unheard of; loyalty was the supreme corporate virtue. The “Traitorous Eight” did not originally intend to start a company; they merely wanted to be hired as a team by a firm with better management. Their letter reached Arthur Rock, a young MBA at Hayden, Stone in New York.

Rock recognized that the combination of elite scientific talent and the character shown by their mutiny was an unprecedented commercial opportunity. He convinced them not to look for an employer, but to start their own enterprise. He secured $1.4 million in financing from Sherman Fairchild to launch Fairchild Semiconductor. This was the birth of “adventure capital”, finance that liberated talent from traditional hierarchies to create an organizational form that best suited their innovation. Fairchild became the primary engine of the Silicon Valley miracle; by 2014, an astonishing 70 percent of publicly traded tech firms in the Valley could trace their lineage back to this single act of defiance.

Arthur Rock further refined this model in 1961 by partnering with Tommy Davis to form Davis & Rock, the first venture capital firm structured as a private limited partnership. This structural shift was the death knell for Doriot’s public corporation model.

The Triumph of the Limited Partnership

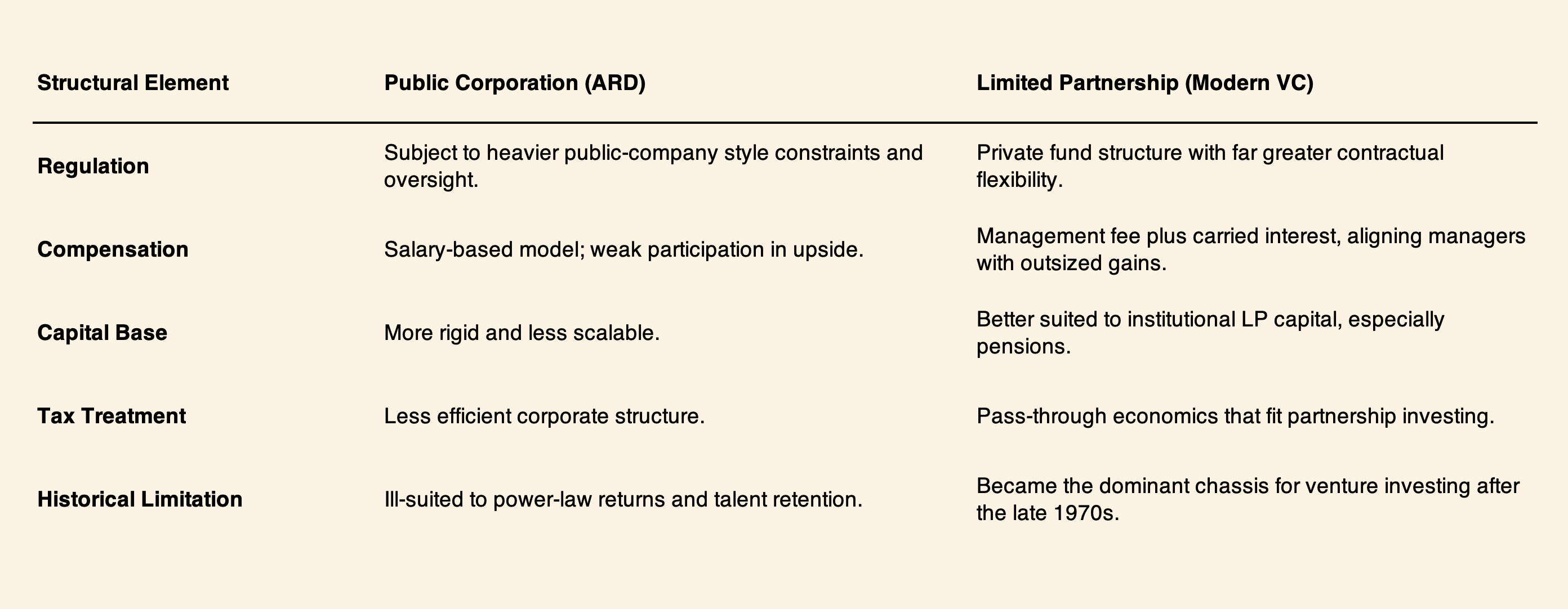

The failure of ARD to survive as the dominant template for venture finance reveals that the history of venture capital was shaped not only by investor psychology, but by legal and fiscal architecture. As a publicly traded investment company, ARD operated under the heavy constraints of the Investment Company Act era and under close SEC scrutiny. That structure made experimentation cumbersome, compensation inflexible, and incentives weak. In a business where a tiny number of outliers can generate the majority of total returns, the inability to reward investment professionals with a meaningful share of upside was not a minor design flaw. It was a fatal one.

The private limited partnership offered a superior architecture. Instead of a public corporation with dispersed shareholders, the new venture firm became a private contractual arrangement between limited partners, who supplied capital, and general partners, who sourced deals, governed portfolio companies, and earned a share of the gains. This solved several problems at once. It reduced regulatory drag, tightened incentive alignment, and allowed venture capitalists to be compensated through carried interest rather than fixed salary. In effect, the LP model created a structure better suited to a power-law business, one in which the economics of the asset class could finally be matched by the economics of the people running it.

Yet the triumph of the LP model was not a purely private-sector achievement. It was reinforced by a series of public-policy decisions that gradually transformed venture capital from a niche financing craft into a scalable institutional asset class. The first major signal came with the Small Business Investment Act of 1958. The U.S. Small Business Administration traces the law directly to a 1957 Federal Reserve study showing that small businesses lacked access to the credit needed to keep pace with technological change. In response, Washington created the SBIC program, under which the SBA would license, regulate, and help fund privately managed investment firms providing long-term debt and equity to high-risk small businesses. In other words, the federal government did not invent venture capital, but it did explicitly recognize the existence of a structural financing gap and began to build institutional machinery to address it.

Tax policy then improved the economics of entrepreneurial and investment risk. The maximum federal tax rate on long-term capital gains fell sharply in the late 1970s and early 1980s: Treasury records show the top rate dropping from 49 percent before the 1978 reform to 28 percent after the Revenue Act of 1978, and then to 20 percent after the Economic Recovery Tax Act of 1981. These changes did not single-handedly create the modern venture industry, but they materially increased the after-tax attractiveness of backing high-upside equity investments. In a field where returns are highly concentrated in a few spectacular exits, lower taxes on realized gains strengthened the incentive to fund risky innovation rather than safer, yield-based assets.

The decisive inflection point, however, came with pension capital. As Paul Gompers and Josh Lerner note, money flowing into new U.S. venture funds between 1946 and 1977 never exceeded a few hundred million dollars annually and usually remained well below that level. The critical change came in 1979, when the Department of Labor reinterpreted ERISA’s “prudent man” rule. Before that shift, many pension fiduciaries avoided venture capital because an investment in an individual start-up could be judged imprudent on its own. The 1979 clarification allowed prudence to be assessed in the context of the entire portfolio and its diversification, rather than at the level of a single risky position. That doctrinal change opened the door for pension funds to become major limited partners in venture partnerships.

The impact was immediate and transformative. As your original draft rightly notes, venture fundraising rose from roughly $450 million in 1979 to more than $5 billion by 1983. That was not just growth. It was a regime change. Once pension money entered the asset class, venture capital ceased to be a semi-amateur activity financed by wealthy families, industrial patrons, and scattered institutions. It became a repeatable financial industry with enough scale to support specialist firms, larger rounds, longer holding periods, and increasingly ambitious technological bets. The modern venture ecosystem, with its dedicated funds, formal LP-GP relationships, and institutionalized search for outliers, depended as much on this regulatory opening as on the talents of any individual investor.

If the Doriot era gave venture capital moral legitimacy, the LP era gave it financial scalability. The crucial lesson is that venture capital did not become dominant simply because investors got smarter. It became dominant because organizational form, tax treatment, and public policy finally aligned with the economics of high-risk innovation. The state did not replace private judgment, but it decisively shaped the conditions under which private judgment could be exercised at scale. That is why the rise of venture capital should be understood not merely as a market story, but as a story of institutional design.

Culture and the Social Network

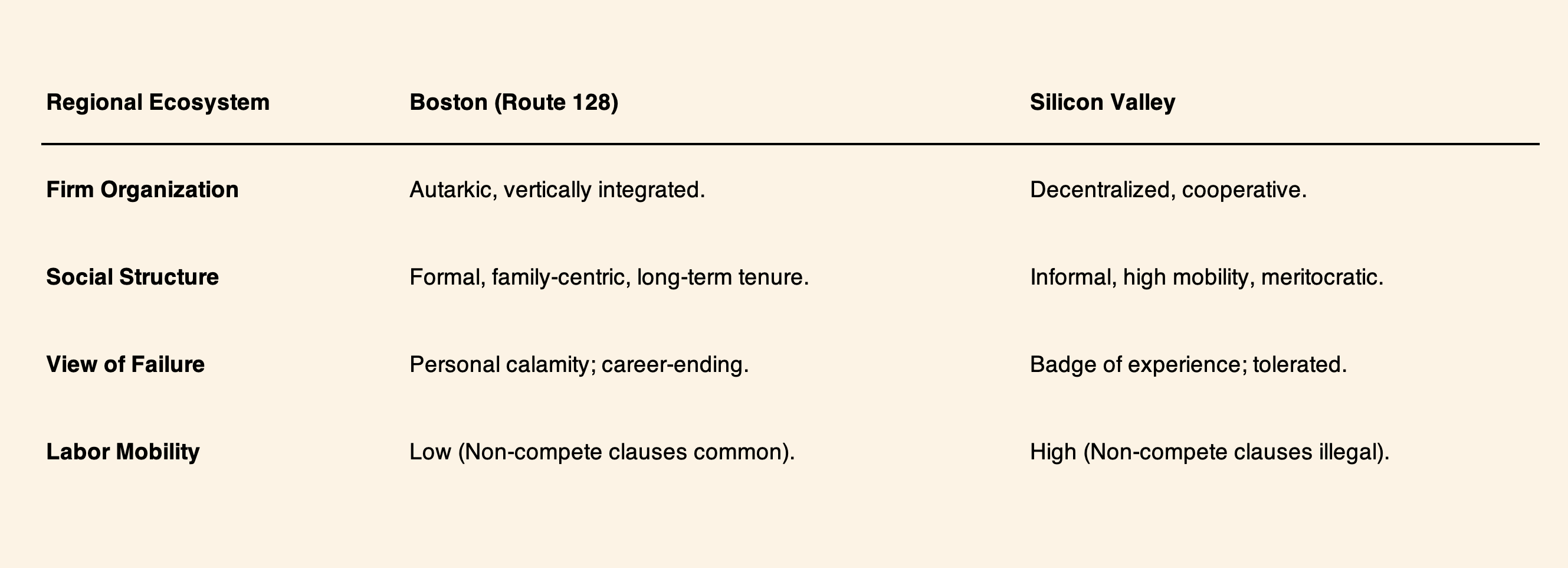

The geographic shift of venture capital’s gravity from Boston to Silicon Valley in the 1980s was driven by what AnnaLee Saxenian calls “Regional Advantage”. Boston’s Route 128 was an established center of high technology long before the Valley had a name; in 1965, it employed three times as many tech workers. However, the cultures were diametrically opposed. Boston’s firms, led by Harvard-educated leaders, modeled themselves after General Motors, emphasizing self-sufficiency and hierarchy.

In contrast, Silicon Valley developed a decentralized industrial system where firms outsourced component parts and shared information freely at watering holes like Walker’s Wagon Wheel. This “networked” culture was amplified by the lack of enforceable non-compete agreements in California law. Venture capitalists were the primary pollinators of this network. Professionals like Bill Younger of Sutter Hill Ventures would take the “smartest guys” to lunch, asking them to identify the next “best guy,” systematically weaving a web of connections that could be rapidly activated when a new opportunity arose.

Sequoia and Kleiner Perkins

In the 1970s, the “activist capital” model replaced Doriot’s “paternalistic” one. Led by Don Valentine (Sequoia) and Tom Perkins (Kleiner Perkins), this era was defined by venture capitalists who had been successful managers at firms like Fairchild and Hewlett-Packard. They didn’t just provide money; they “stamped their will” on portfolio companies.

Tom Perkins famously utilized “risk-stage” financing. At Tandem Computers, he brought in consultants to eliminate technical risks before committing more capital. At Genentech, the first major biotechnology firm, he pressed the founders to contract research to existing labs to preserve cash, a hands-on intervention that generated a 200x return for Kleiner Perkins. Don Valentine was similarly aggressive with Atari, forcing the company to focus on the “Home Pong” market and later facilitating its sale to Warner Communications.

This was “finance without finance”, a model where investors skipped the spreadsheets and focused on evaluating character, fiber, and “intellectual book value”. Arthur Rock would ignore financial projections to flip straight to the founders’ résumés, asking open-ended questions and waiting through long silences to see if the entrepreneur would break under pressure. If the founders were “seeing things the way they wanted them to be rather than the way they are,” Rock would pass.

The Youth Revolt and the Sovereign Founder

The most recent evolution of venture capital, beginning around the turn of the millennium, represents a dramatic rebalancing of power toward the entrepreneur. This “Youth Revolt” was sparked by the success of Google and Facebook, companies that did not just achieve scale but achieved total market dominance. In the earlier era, VCs like Don Valentine had the power to fire founders; in the case of Cisco, the founders were eventually ousted after a clash with Valentine’s professional CEO hire.

But by 2005, the abundance of capital and the emergence of “branded” growth equity changed the leverage dynamics. Sean Parker, having been “burnt” by Sequoia in his earlier venture Plaxo, advised Mark Zuckerberg on how to maintain control of Facebook. Peter Thiel’s Founders Fund codified this shift into an ideology. Thiel argued that VCs should stop “polishing” founders through mentorship and instead embrace “corporate monarchism,” finding “rough diamonds” and letting them reign unchallenged.

This era introduced the “dual-class share” structure, where founders retained super-voting rights even after going public. This shift was accelerated by the arrival of “kingmaker” capital from Masayoshi Son of SoftBank and Yuri Milner of DST Global. In 2009, Milner offered Facebook $200 million at a $10 billion valuation without requesting a board seat, an offer Zuckerberg could not refuse. This “non-interference” model signaled that for the most promising outliers, the venture capitalist was no longer a parent or a boss, but a service provider.

Governance Failures and Blitzscaling

The shift to a founder-centric, risk-seeking model has produced both the greatest successes of the digital age and its most infamous disasters. The “blitzscaling” model, hiring without vetting and bringing unfinished products to market to achieve rapid dominance, thrives in a “founder-friendly” ecosystem where monitoring is deliberately skipped. Mallaby highlights how this obsession with the “lone genius” fostered hubris at WeWork and Uber.

At Uber, founder Travis Kalanick’s aggressive culture eventually led to a “Shakespearean” depiction of ambition and ego, where investor Bill Gurley of Benchmark had to launch a campaign to oust the very founder he had empowered. Similarly, the SoftBank-fueled expansion of WeWork demonstrated that an avalanche of venture money could sustain unprofitable business models for too long, destroying economic value in the process. These failures suggest a “director contagion,” where the lack of board oversight allows the reputation of a company to be ruined by the unchecked impulses of its leader.

The Ethics and Geopolitics of the New Future

As venture capital has evolved into a global force, it has faced increasing scrutiny regarding its social impact. The industry remains a tight-knit “clique” that is profoundly lack-of-diverse: as of 2020, women account for only 16 percent of investing partners, and Black partners account for just 3 percent. This “social clustering” along demographic lines ensures that funds flow disproportionately to founders who share the same profiles as the investors, systematically excluding massive talent pools.

However, the “positive case” for venture capital remains compelling. While critics argue that VCs only show up for success, academic research confirms that VC-backed companies generate 89 percent of R&D spending among public firms and are far more likely to successfully reach IPO than non-backed peers. Venture-backed firms accounted for 47 percent of U.S. non-financial IPOs between 1995 and 2019.

Furthermore, the model has become a pillar of national power. The rise of China as a technology rival is directly attributable to the importation of Silicon Valley’s venture model. Sequoia China and other partnerships applied the power-law logic to the Chinese internet, creating a digital economy that now rivals the United States. In a world shifting from tangible assets (factories and machines) to intangible assets (software and data), the hands-on venture model is increasingly the only effective way to allocate capital.

Conclusion

The evolution of venture capital from Georges Doriot’s “cathedrals” to the modern power-law era reveals a fundamental transformation in the human approach to innovation. Doriot provided the moral and institutional legitimacy for the industry, teaching that financing “noble” ideas was a worthy pursuit for a mature society. Arthur Rock provided the “liberation capital” that broke talent free from the stultifying hierarchies of the 1950s. Valentine and Perkins refined the activist tools needed to eliminate “white-hot risk” and build industrial pillars.

Today, the industry has pushed the logic of the outlier to its mathematical extreme. While the shift to founder-monarchism and blitzscaling has created significant governance challenges, it remains the most productive crucible for technological discovery ever devised. It operates as a “third institution” between the market and the corporation, combining the strategic vision of the latter with the ruthless price-signal discipline of the former.

The evolution of venture capital demonstrates that the future cannot be predicted by analyzing patterns of the past; it must be discovered through high-risk experiments led by “unreasonable” people. By backing the improbable, this strange tribe of financiers has made the modern world possible. As Doriot’s father Auguste once asked his second-placed son, “And why not first?” venture capital has institutionalized that question for an entire global economy, refusing to accept anything less than the total transformation of the human predicament.

Sources:

Sebastian Mallaby - The Power Law: Venture Capital and the Making of the New Future (2022)

Spencer E. Ante - Creative Capital: Georges Doriot and the Birth of Venture Capital (2008)

Cover Artwork

A visit to the Art Dealer

Frans Francken the Younger , c. 1636

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.

Good piece. The part that sticks is the honesty about what game venture actually is. It’s not about being right often, it’s about being right where it matters.

The shift from Doriot to today reads like control slowly slipping away from the investor and concentrating in the outlier. Early on it was about building companies. Now it’s about not missing the one that bends everything else around it.

Also like the framing around structure. People talk about vision and talent, but the real unlock was the system that let those bets scale. Once the incentives matched the reality of the power law, everything accelerated.

Big takeaway is simple. Most bets don’t matter. The few that do carry everything, and the whole system is built around finding them without knowing which one it is ahead of time.