2024 Crypto Venture Capital Trends

The crypto market experienced significant growth in 2024, driven by key milestones such as the launch of spot-based Bitcoin ETFs in January and the election of a pro-crypto U.S. President and Congress in November. The market cap of liquid crypto surged by $1.6 trillion (+88% YoY) to close the year at $3.4 trillion, with Bitcoin accounting for $1 trillion of this growth, ending near $2 trillion. Bitcoin’s rise, responsible for 62% of the total market gains, was complemented by trends in memecoins and AI-powered tokens, which dominated on-chain activity, particularly on Solana.

Despite the market's resurgence, the crypto VC landscape remained challenging. Key trends—Bitcoin, memecoins, and AI agent tokens—offered limited venture opportunities as they predominantly utilized existing on-chain infrastructure. Former hot sectors like DeFi, gaming, metaverse, and NFTs failed to attract significant new attention or capital. Infrastructure plays, now largely mature, face increasing competition from traditional financial services intermediaries in anticipation of regulatory changes under the new U.S. administration.

Emerging trends such as stablecoins, tokenization, DeFi-TradFi integration, and crypto-AI intersections showed promise but remained nascent. Meanwhile, macroeconomic pressures, including high interest rates, discouraged risk-heavy allocations, disproportionately impacting the crypto VC sector. Generalist VC firms largely stayed away, cautious after the high-profile collapses of 2022.

We invite you to explore our latest report: "300+ Crypto Predictions for 2025 from ETF Issuers, VC Funds, and Industry Experts"

Based on data from Galaxy Research, venture capitalists invested $3.5 billion in Q4 2024 into crypto and blockchain-focused startups, marking a 46% quarter-over-quarter increase. However, the number of deals declined by 13% QoQ, with 416 transactions recorded during the quarter.

")

For the entirety of 2024, venture capital investment in crypto and blockchain startups totaled $11.5 billion, distributed across 2,153 deals.

According to PitchBook's 2025 Enterprise Technology Outlook, senior analyst Robert Le forecasts that annual investment in the crypto market will exceed $18 billion in 2025, with multiple quarters surpassing $5 billion. This marks a substantial percentage increase compared to 2024 but remains notably below the levels observed in 2021 and 2022.

The growing institutionalization of Bitcoin, the rise of stablecoins, and potential regulatory advancements toward DeFi-TradFi integration highlight areas for future innovation. These factors, combined with emerging trends, could catalyze a recovery in venture capital activity.

Capital Invested and Bitcoin Price

Historically, there has been a strong correlation between Bitcoin's price and the amount of capital invested in crypto startups. However, since January 2023, this correlation has weakened significantly. Bitcoin has reached new all-time highs, while VC investment activity has struggled to keep pace.

Possible Explanations:

Weak Allocator Interest: Institutional investors may be hesitant due to regulatory uncertainties and market volatility.

Shift in Market Narratives: Current market narratives favor Bitcoin, potentially overshadowing other crypto investment opportunities.

Venture Capital Landscape: The broader venture capital market is experiencing a downturn, which impacts crypto investments.

Top VC-Funded Sectors in Crypto

Infrastructure dominated crypto VC funding in 2024, attracting $5.5 billion across 610+ deals—a 57% YoY increase and the sector's highest funding to date, according to The Block. Investments focused on scaling blockchain networks through Layer-2 solutions, improving speed, cost, and scalability. Modular technologies, including data availability, shared sequencers, and rollups-as-a-service, secured significant funding, while liquid staking protocols and developer tooling remained key priorities.

NFTs and gaming startups raised $2.5 billion, slightly surpassing 2023’s $2.2 billion. Despite stable funding, NFT marketplace activity declined as memecoins gained traction. With 610+ deals, NFTs and gaming retained focus, though activity has matured since the 2022 peak of 936 deals. Enterprise blockchain funding fell sharply, plummeting 69% YoY to $164 million from $536 million in 2023.

Web3 funding showed resilience, raising $3.3 billion over two years, close to the $3.4 billion raised in 2021–2022. Growth was driven by emerging areas such as SocialFi, crypto-AI, and decentralized physical infrastructure networks (DePINs). DePINs emerged as a fast-growing vertical, attracting over 260 deals and nearly $1 billion in funding.

DeFi experienced a strong resurgence in 2024, with 530+ deals (+85% YoY) compared to 287 in 2023. Bitcoin-based DeFi use cases, including stablecoins, lending protocols, and perpetual swaps, were key drivers of this growth.

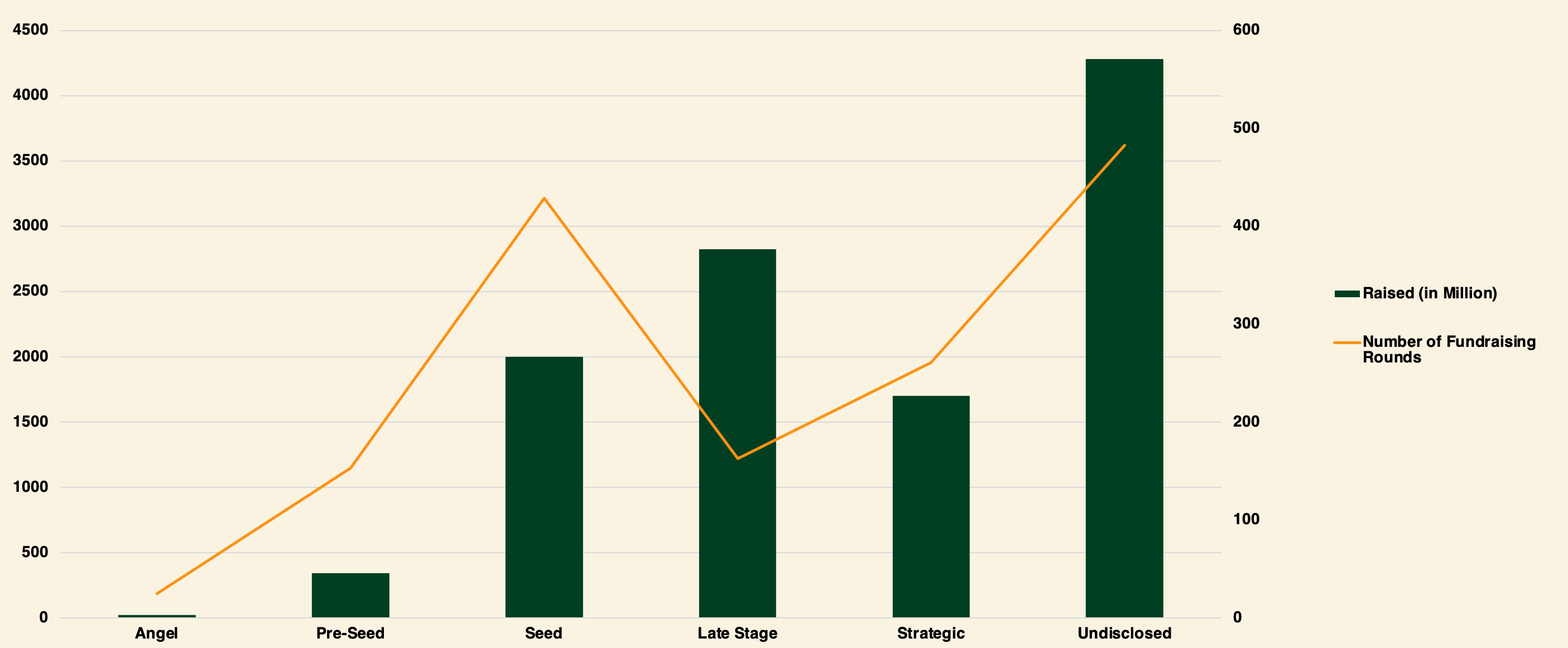

The chart above clearly demonstrates that, excluding undisclosed rounds, the crypto sector remains heavily concentrated in early-stage funding. Early-stage deals attracted the majority of capital investment, accounting for 60%, while later-stage deals represented 40% of the total capital—a notable rise from 15% in Q3.

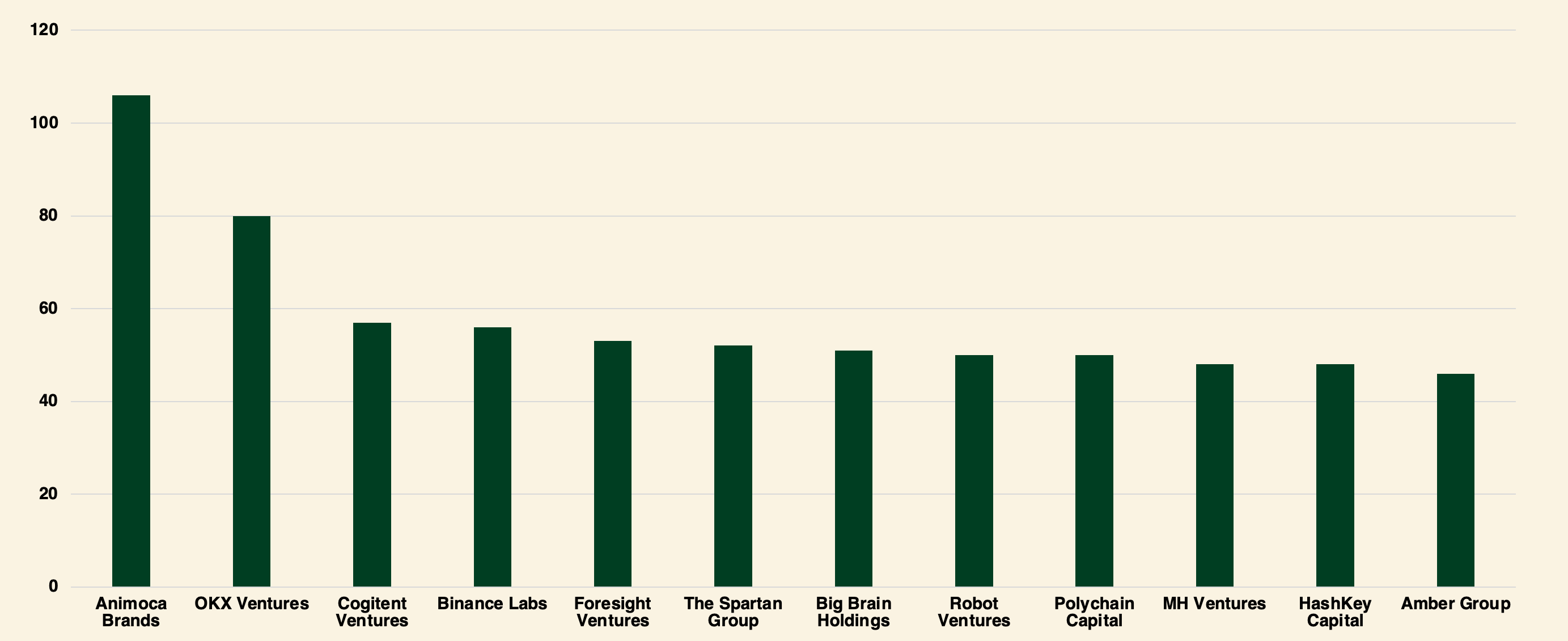

Most Active Investors

In 2024, Animoca Brands led venture capital activity with over 100 funding rounds, followed by OKX Ventures with more than 80. Cogitent Ventures, Binance Labs, and Foresight Ventures completed around 60 rounds each, while The Spartan Group, Big Brain Holdings, and Robot Ventures executed over 50. Key players like Polychain Capital and Amber Group maintained steady activity with 40+ rounds.

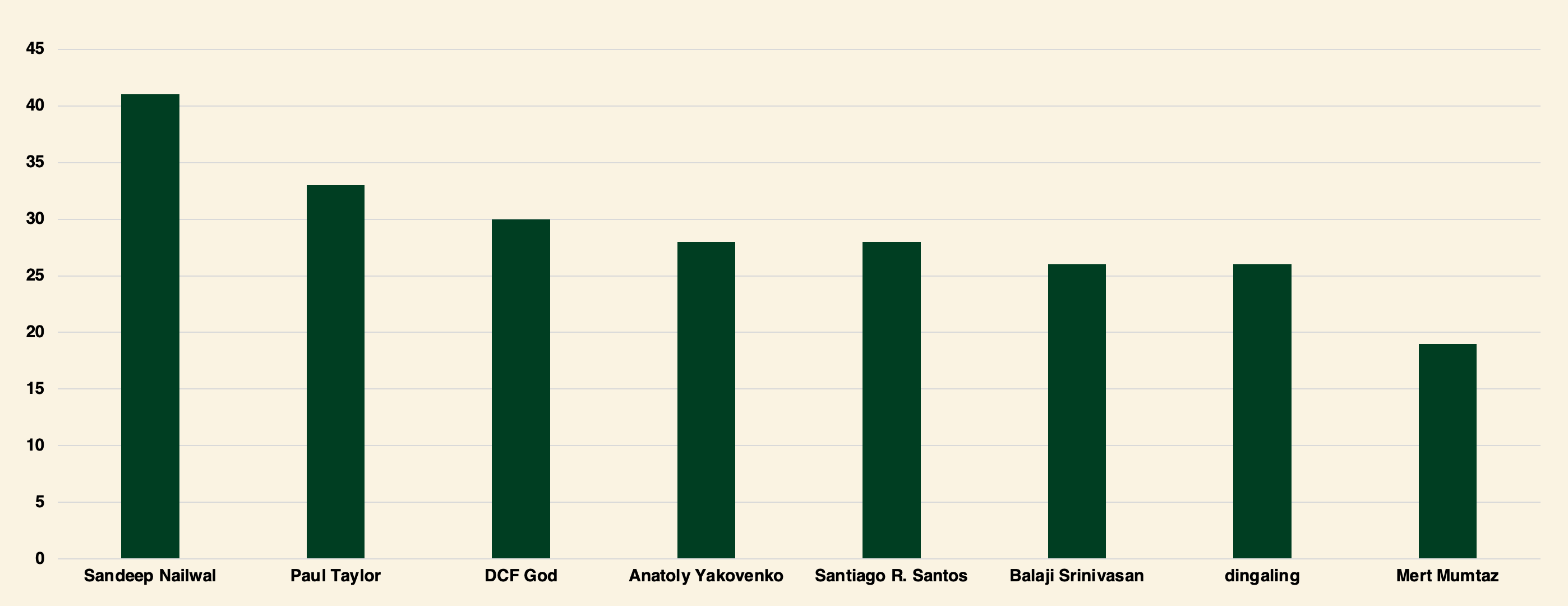

Among angel investors, Sandeep Nailwal (Polygon Founder) participated in over 40 rounds, making him the most active, followed by Paul Taylor and DCF God with 30+ each. Anatoly Yakovenko (Solana Founder), Santiago R. Santos, and Balaji Srinivasan were also significant contributors, completing over 25 rounds, with Mert Mumtaz slightly trailing but remaining active.

Crypto Venture Fundraising

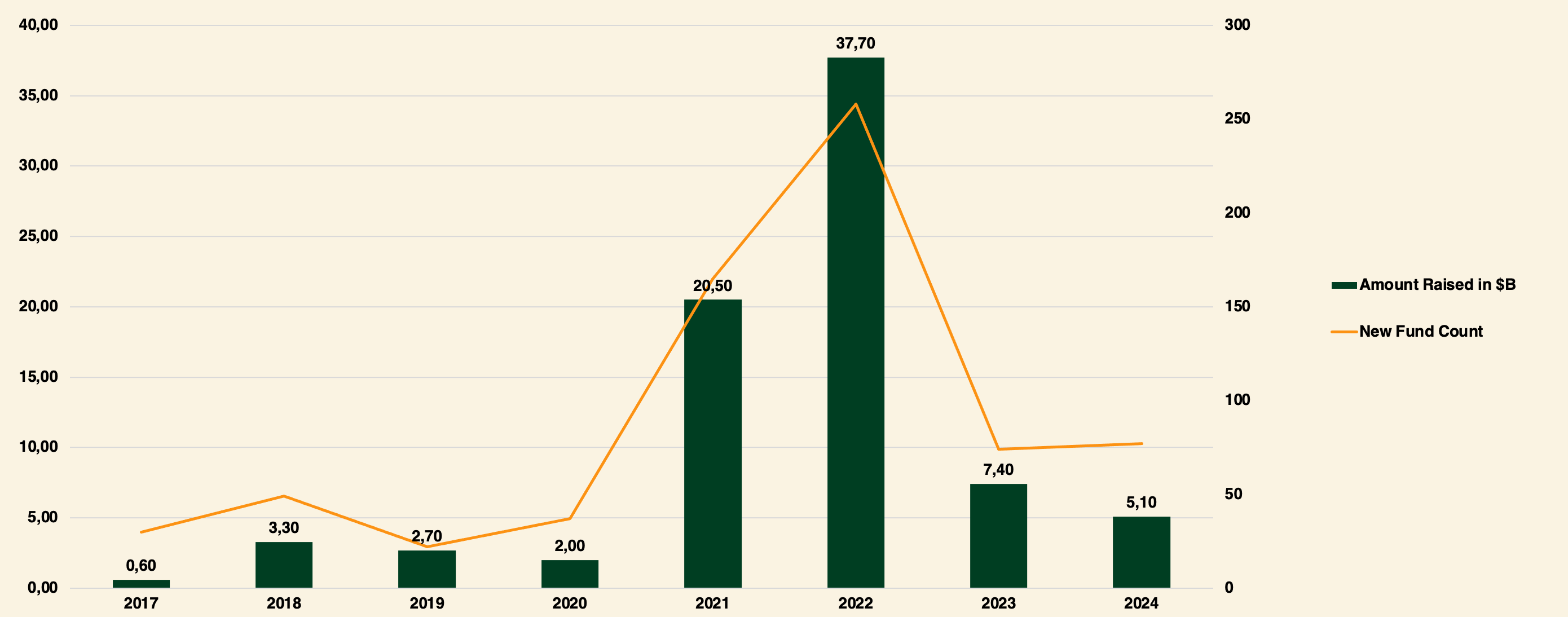

Venture capital fundraising in 2024 dropped to its lowest level in six years, with 865 funds raising a total of $104.7 billion—a significant 18% decline from $128 billion raised by 1,029 funds in 2023, according to Venture Capital Journal. Both the amount raised and the number of funds declined by 16% year-over-year.

Crypto venture fundraising remained under pressure, driven by macroeconomic headwinds and lingering market volatility from 2022-2023. Allocators reduced commitments to crypto VC funds, reflecting a shift from the bullish sentiment seen in 2021 and early 2022. Despite expectations of rate cuts in 2024, meaningful reductions materialized only in the latter half of the year, with venture fund capital allocations continuing to decline quarter-over-quarter since Q3 2023.

Capital raising by crypto venture capital funds in 2024 was notably weak, with only 79 new funds securing $5.1 billion—representing the lowest annual total since 2020. While the number of new funds showed a slight year-over-year increase, diminished interest from allocators led to a significant reduction in fund sizes. Both the median and average fund sizes in 2024 reached their lowest levels since 2017, highlighting the increasingly challenging fundraising landscape.

Shift Towards Midsized Funds

Historically, smaller funds (under $100 million) dominated crypto VC fundraising, reflecting the industry's early stage. Since 2018, however, there has been a noticeable shift toward midsized funds ($100–$500 million).

While megafunds ($1 billion or more) saw rapid growth from 2019 to 2022, they have been absent in 2023 and 2024 due to challenges such as:

Deployment Difficulties: A limited number of startups require significant capital.

Valuation Risks: Large investments drive up valuations, increasing risk.

Nevertheless, prominent funds like Pantera Capital and Standard Crypto ($500 million) remain active, broadening their mandates to include areas beyond crypto, such as artificial intelligence. Notably, Pantera Fund V, a successor to Pantera Blockchain Fund IV, is set for its first close on July 1, 2025, with a $1 billion target.

Below is a table summarizing the 10 funds that raised over $100 million in 2024. The largest closed fund in 2024 was Fund III, managed by Paradigm.

Notable Funding Rounds in 2024

Monad: an EVM-compatible Layer 1 blockchain, achieves exceptional throughput of up to 10,000 transactions per second, with 1-second block times and single-slot finality. Its parallel transaction execution architecture ensures efficiency, making it a top choice for developers seeking speed and scalability.

Farcaster: enables social networks where users control their data. Its “sufficiently decentralized” design allows interactions without network-wide approval, using a non-custodial social graph secured by Ethereum. Warpcast, a flagship app, highlights its potential to redefine social media.

Berachain's Proof-of-Liquidity (PoL) consensus ties network security to liquidity provision, allowing validators to stake liquidity assets to enhance security while earning rewards. EVM compatibility simplifies DeFi application deployment, cementing Berachain's role in the decentralized finance ecosystem.

Story Protocol: transforms intellectual property management with on-chain registration, automated licensing, and monetization via ERC-6551-enabled token-bound accounts. Leveraging both Ethereum Virtual Machine and Cosmos SDK, it offers creators unparalleled control and fosters innovation.

0G Labs: combines blockchain scalability with AI-driven processes, featuring a robust data availability layer and a decentralized AI operating system (dAIOS). Leading 2024’s funding rounds with $250M raised, it surpassed Monad, solidifying its dominance in the AI-blockchain intersection.

Polymarket: a decentralized prediction market, gained significant traction during the 2024 U.S. presidential election, showcasing Web3’s potential for rapid adoption despite post-event metric declines.

Blockchain Infrastructure

EigenLayer: Introduces a restaking marketplace to maximize Ethereum’s staked assets, improving security and validator revenue.

Babylon: Integrates Bitcoin’s proof-of-work with proof-of-stake blockchains, offering tamper-proof security and cross-chain interoperability.

Blockchain Services

Sentient: Enables decentralized AI applications by utilizing blockchain’s distributed networks for scalable and private AI computations.

Zama: Implements homomorphic encryption for secure data processing on blockchain, ensuring privacy without sacrificing functionality.

Key Trends for 2024 and Beyond

AI integration, DeFi on Bitcoin, and specialized blockchains dominate the blockchain landscape. Projects like 0G Labs and Sentient lead in AI, while Babylon strengthens Bitcoin’s role in DeFi. In the near future, Monad, Berachain, and Story Protocol are expected to launch their mainnets.

Conclusion

The crypto venture capital landscape in 2024 exhibits cautious optimism, marked by a rebound in fundraising activities and growing institutional interest. The shift towards midsized funds and the continued dominance of emerging managers signal a maturing industry adapting to evolving market dynamics. Despite short-term declines in VC investments and extended fundraising cycles, the sustained focus on early-stage ventures and emerging trends like AI integration underscore a resilient ecosystem poised for future growth. Overall, the sector demonstrates underlying strength, suggesting that renewed momentum may be on the horizon.

Sources

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer's views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.