Can Stablecoins Reshape Global Finance?

Stablecoin circulation has exceeded $215 billion globally as of Q1 2025, with on-chain transaction volume hitting $5.6 trillion in 2024—equivalent to 40% of Visa’s payments volume. Once confined to crypto markets, stablecoins now power real-economy transactions at scale, from remittances to merchant payments. Their role in cross-border finance is rapidly expanding, especially in emerging markets, while institutional adoption accelerates through initiatives from Visa, Stripe, and BlackRock. As regulatory clarity improves and new entrants challenge incumbents like Tether and Circle, stablecoins are poised to reshape global payment systems. This issue explores the key trends, risks, and opportunities shaping stablecoins' evolution from 2025 to 2030.

Global Stablecoin Market Overview (2025)

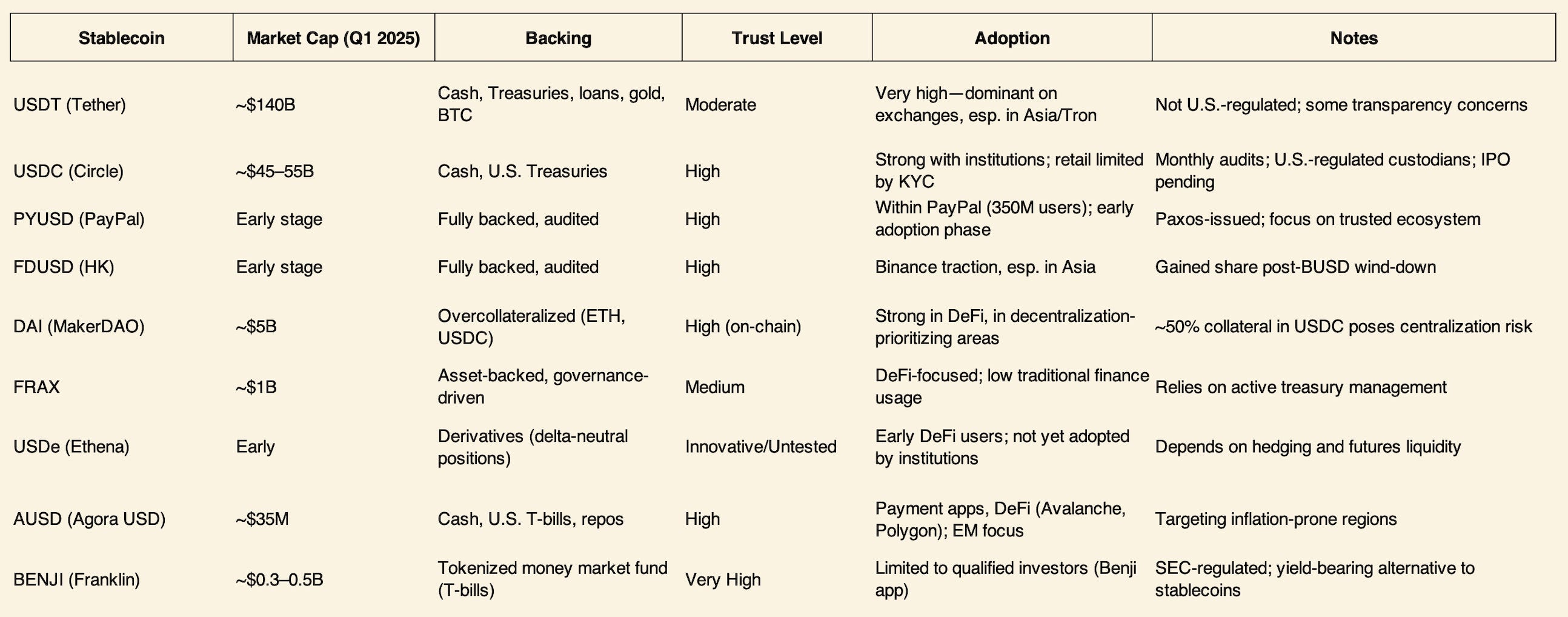

The stablecoin market has expanded dramatically, more than doubling from under $120 billion in early 2023 to over $215 billion in early 2025. This growth underscores that stablecoins have broken out of niche crypto trading circles and become widely used digital cash. Tether (USDT) and USD Coin (USDC) remain the giants – with ~$140B and ~$55B circulating respectively – but their combined ~90% share in 2024 is slowly diluting as new issuers emerge.

Notably, PayPal USD (PYUSD) launched in late 2023, FDUSD (First Digital USD) out of Hong Kong, Agora’s AUSD,Ethena’s USDe, and others like TrueUSD (TUSD) and DAI collectively make up the remaining ~10%. These newer stablecoins aim to differentiate on transparency, regulatory compliance, or yield-sharing, which is gradually chipping away at Tether and Circle’s dominance. We expect the stablecoin universe to diversify further as major banks and fintechs issue their own tokens by late 2025, lowering concentration in any single stablecoin issuer.

Adoption & Usage Metrics

Stablecoins’ growing appeal is evident in both user numbers and on-chain activity. By January 2025, over 32 million unique addresses had transacted with stablecoins—more than double the figure from two years earlier—signaling rising adoption among both retail and institutional users. This includes users in emerging markets seeking digital dollars amid high inflation, as well as crypto-native participants in DeFi and trading. Notably, stablecoin activity extends beyond public blockchains; significant volumes occur off-chain on centralized exchanges and custodial wallets.

Nevertheless, on-chain volumes have surged, with adjusted stablecoin volume reaching $5.6 trillion in 2024, up from $3.8 billion in 2018. This measure, which excludes wash trading and bot activity, highlights real economic use and now represents approximately 40% of Visa’s payment volume. Increasingly, this volume stems from institutional and enterprise usage, including corporate treasuries and fintech apps leveraging stablecoins for cross-border liquidity and instant settlement—beyond exchange-related flows.

Wallet distribution has also diversified. Stablecoins are now held across millions of non-exchange wallets worldwide, including those of merchants and savings platforms. Transaction sizes vary widely—from sub-$100 transfers by individuals to multi-million-dollar institutional transfers. Regional data reflects this diversity: in Nigeria, 85% of crypto transfers are under $1 million, indicating strong use by retail and SMEs, while in Brazil, large transfers (>$1M) are rising as banks and firms adopt stablecoins.

Growth Trajectory (2023–2025)

The post-2020 stablecoin boom began with rapid growth driven by crypto trading, followed by a plateau in 2022 after the TerraUSD collapse. Since 2023, growth has resumed strongly, supported by real-world applications and institutional backing. From 2022 to 2024, venture capital investment in stablecoin-related startups exceeded $2.5 billion, targeting compliance, cross-border payments, and yield-bearing stablecoins.

Major corporate moves underscore market confidence. Circle Internet Financial, issuer of USDC, filed for a U.S. IPO in early 2024, aiming to be the first publicly listed stablecoin issuer, with the listing expected in 2025. This would provide capital to scale operations and further integrate USDC into mainstream finance. In another major development, Stripe acquired Bridge for $1.1 billion in late 2024—one of the largest crypto M&A deals to date. Bridge offers stablecoin and blockchain payment APIs, and Stripe’s acquisition reflects strong belief in stablecoins' future role in payments.

Stablecoin-related M&A in banking has also increased, with BNY Mellon expanding its partnership with Circle to integrate stablecoin settlement. Additionally, high-profile partnerships (e.g., Visa and Mastercard’s stablecoin settlement pilots) indicate industry maturation and growing involvement from traditional financial institutions.

World-Changing Use Cases

Cross-Border Remittances

This is perhaps the clearest real-world impact of stablecoins. International money transfers have long been plagued by high fees (average ~6% for remittances) and slow settlement. Stablecoins change that dynamic by enabling near-instant, low-cost transfers of value over the internet. For example, sending $200 from one African country to another via stablecoin is about 60% cheaper than via traditional remittance services. The speed is measured in minutes (or seconds, on faster chains) instead of days.

Real case studies

Latin America: In 2023, Mexico emerged as a leading recipient of crypto-dollar remittances. According to Banxico, $63.3 billion in stablecoin remittances flowed into the country—approaching its total remittance inflows. Fintech firm Bitso facilitated up to 10% of US-to-Mexico remittances, converting USDC to pesos for recipients. This reduced fees, saved families millions, and enabled same-day payouts, compared to multi-day wire transfers. In Brazil, business use of stablecoins for cross-border payments rose sharply, with >$1M transactions increasing ~29% in late 2023 as firms sought lower-cost forex alternatives.

Sub-Saharan Africa: The region leads in grassroots stablecoin adoption. In Nigeria and Kenya, remittances and B2B payments increasingly use stablecoins (often USDT via mobile apps), bypassing Western Union. Sending $200 through traditional channels can cost 8–12%, while stablecoins plus local exchanges reduce this to below 3%, with instant delivery. Stablecoins also overcome weak banking infrastructure, providing fast, mobile access. As of mid-2024, 43% of Africa’s crypto transaction volume involved stablecoins. In Nigeria, over $59 billion in crypto was received annually, with stablecoins critical amid naira volatility. Even Ethiopia, despite strict capital controls, saw a 180% YoY rise in retail stablecoin transfers after its 2023 currency devaluation, highlighting reliance on USDC/USDT.

Cost & Time Efficiency: Traditional remittances can take 3–5 days and involve multiple intermediaries, inflating costs. Stablecoin transfers incur only network fees—mere cents on Tron or a few dollars on Ethereum—and settle within one block. For example, a Filipino worker in the U.S. can send USDC home, with same-day PHP conversion via local exchanges or ATMs. According to the World Bank, digital remittances, including crypto, are helping drive costs toward the UN’s sub-3% target, with stablecoins playing a key role.

Global Payroll (Remote Work Payments)

Stablecoins are transforming cross-border payments for freelancers and remote workers. Companies can now pay salaries in digital USD without the delays or costs of international wires. A key example is Remote.com’s partnership with Stripe, which launched stablecoin payroll in December 2024 across 69 countries, using USDC on a low-cost blockchain. A U.S.-based company can pay overseas contractors in USDC via Remote’s platform, with funds received almost instantly in a wallet (e.g., Coinbase’s Base network), while the employer is debited in USD. This eliminates intermediary bank fees and long delays—especially vital for workers in countries with weak banking infrastructure.

Freelancer Impact: Freelancers in developing markets often face limited access to global banking, with wire transfers costly or inaccessible. Stablecoins provide immediate access to dollar balances. Workers can hold USDC(valuable amid inflation), spend it directly (where accepted), or convert to local currency via exchanges or P2P platforms. A Nigerian freelancer, for example, may reduce fees from 10% (via banks) to under 2% with USDC. Additionally, payout speed improves dramatically—what once took a week now takes minutes on-chain.

Corporate Efficiency: For employers, stablecoin payroll simplifies treasury management. Companies can pay globally from a single USD stablecoin pool 24/7, without maintaining foreign accounts or navigating wire deadlines. Remote.com ensures compliance (KYC, tax documentation), addressing prior hurdles to crypto payroll. Firms like Stripe expect stablecoin payouts to attract businesses seeking efficient global hiring. Adoption has been strong in tech fields—e.g., open-source contributors, designers, and content creators are opting for USDC. Traditional outsourcing firms may follow, avoiding local currency volatility and delays.

Financial Inclusion: In countries like Argentina or Turkey, stablecoin salaries offer individual-level dollarization and protection against inflation. Workers gain a stable store of value, convertible as needed, and access to a de facto USD account via smartphone—without relying on local banks. This expands global economic participation, enabling skilled workers in underbanked regions to be paid efficiently and securely.

Capital Markets Settlements

Stablecoins are streamlining capital markets by enabling instant, on-chain settlement of securities, eliminating the traditional T+2 day delay and reducing reliance on intermediaries. Governments and institutions now issue tokenized bonds and money market funds, with stablecoins like USDC serving as the payment rail—e.g., Hong Kong’s 2023 green bond pilot and BlackRock’s 2024 USD Digital Liquidity Fund on Ethereum. Equity settlement pilots, including Paxos’s T+0 settlement with Credit Suisse and DTCC’s Project Ion, highlight regulatory acceptance, with Visa’s USDC support reinforcing institutional momentum. Additionally, tokenized U.S. Treasuries and JPM Coin are being used for real-time collateral settlements and 15-minute repo transactions, improving liquidity and reducing systemic risk by unlocking billions in idle capital.

On-Chain Treasury Management

Corporations and institutions with large cash reserves are increasingly using stablecoins for treasury operations and liquidity management. Holding capital in stablecoins—rather than in local banks—enables faster cross-border payments and access to DeFi yield opportunities.

Institutional Treasury Use: In 2024, Tesla disclosed holding a portion of its cash in digital assets, including stablecoins, to expedite global transfers between subsidiaries. Stripe uses USDC for instant cross-border payouts, while firms in volatile economies—such as Latin American exporters—hold stablecoins like USDC to hedge against local currency depreciation before gradual conversion for expenses.

Yield Strategies: Stablecoins allow treasurers to earn 4–5% yields via DeFi protocols like Aave, Compound, or tokenized T-bill funds, often exceeding traditional bank rates. Meta (Facebook) reportedly experimented with allocating part of its $44B cash reserves to short-term DeFi lending via third-party funds. Crypto-native firms, family offices, and hedge funds increasingly invest in “stablecoin funds” that arbitrage DeFi yields. While smart-contract risks exist, solutions with insurance and custodial safeguards are mitigating concerns.

Treasury Integrations: Platforms like Fireblocks and Coinbase Custody offer secure, multi-user workflows for holding and transacting stablecoins, mirroring corporate banking standards. ERP systems are also integrating stablecoin capabilities—SAP’s 2025 update will support USDC transactions via banking APIs, enabling treasurers to convert USD to USDC, deploy it on-chain, or pay suppliers within existing systems, all while maintaining compliance.

Case Study – Stripe Treasury: After acquiring Bridge, Stripe’s treasury unit enables merchants to hold stablecoins instead of converting to fiat. This supports global businesses: they accept payments in multiple currencies, consolidate in stablecoins, earn yield, and pay out globally. Stablecoins are becoming the working capital of the internet economy—programmable, always-on dollars connecting TradFi and DeFi. Adoption is early, but surveys show rising interest among finance executives, especially as regulations mature and rate differentials encourage treasury innovation.

Dollarization & Financial Inclusion

In high-inflation and capital-controlled economies, stablecoins drive grassroots dollarization by offering access to stable value and a medium of exchange. In Argentina, amid 100%+ inflation and a 2023 peso devaluation, stablecoin use surged—USDT became widely accepted as digital cash, while USDC served as a savings tool. Turkey now leads globally in stablecoin volume relative to GDP, with citizens using USDT to hedge against 50%+ inflation and manage FX needs. In Africa, dollar scarcity prompts USDT purchases via P2P markets; in Nigeria, importers use USDC to bypass banking delays, and 33% of Nigerians used stablecoins for payments or savings in 2024. Stablecoins also advance financial inclusion, enabling unbanked individuals, refugees, and SMEs to access mobile, low-fee financial services, including aid and remittances. However, the IMF warns that widespread stablecoin use may undermine monetary policy and tax collection, though their real-world impact, especially in volatile economies, continues to grow.

Regulatory Landscape: March 2025 Update

Regulation of stablecoins has rapidly evolved from talk to action. By March 2025, major jurisdictions have either implemented or proposed comprehensive stablecoin rules. This section reviews key developments in the U.S., Europe, and Asia-Pacific, and examines their implications for the industry.

United States

As of March 2025, the U.S. lacks a federal stablecoin law, but bipartisan bills debated in 2024, including the Clarity for Payment Stablecoins Act (Rep. McHenry) and a proposal by Rep. Waters, show growing consensus. Both require 100% reserve backing in cash or Treasuries, enforce prudential oversight, and propose a two-year moratorium on algorithmic stablecoins. The main divergence lies in regulatory authority: one approach allows banks and licensed non-banks (e.g., Circle) to issue stablecoins under state or federal supervision, while another (Sen. Hagerty’s bill) assigns oversight to the Fed, OCC, or state regulators based on issuer type. Issuers would face mandatory audits, prompt redemption rights, capital requirements, and likely prohibitions on paying interest to avoid shadow banking concerns. While no bill has passed yet, momentum suggests legislation may arrive by late 2025. Meanwhile, the SEC and CFTC have acted under existing laws—e.g., the SEC’s 2023 challenge of Paxos’ BUSD issuance and the CFTC’s commodity classification of USDT—creating legal uncertainty. Regulators remain cautious, but industry-wide clarity is expected soon, potentially unlocking broader institutional adoption.

Europe (EU) – MiCA Implementation

The EU implemented the Markets in Crypto-Assets (MiCA) regulation in 2023, with stablecoin rules effective from June 2024, creating a comprehensive legal framework for so-called “asset-referenced” and “e-money tokens.” Issuers of euro or foreign-pegged stablecoins must be EU-based entities, obtain regulatory approval, and publish detailed disclosures on governance and reserves. MiCA requires full reserve backing, prohibits lending or rehypothecation of reserves, mandates regular audits, and bars passing interest to token holders to avoid classification as securities. Stablecoins reaching €5M daily volume or €500M market cap face enhanced European Banking Authority oversight, and regulators can cap issuance to protect monetary policy. Firms like Circle are pursuing MiCA licenses, and EU banks can issue stablecoins under existing licenses. MiCA’s clarity is expected to drive adoption across fintech and public sectors, positioning Europe as a regulatory benchmark, though issuer profits may compress due to the ban on yield-sharing.

Asia-Pacific

Asia’s stablecoin regulation is rapidly evolving, led by Japan, Hong Kong, and Singapore. Japan eased restrictions in February 2025, now allowing up to 50% of reserves in government bonds or term deposits, enabling safe yield generation for issuers. Foreign stablecoins like USDC are now tradable domestically (e.g., via SBI VC Trade), with strict custody and audit rules ensuring consumer protection. Hong Kong, aiming to be a stablecoin issuance hub, introduced a mandatory licensing regime via the HKMA in late 2024, requiring local reserve custody and governance standards similar to MiCA, with implementation expected in 2025. Singapore’s MAS finalized its stablecoin framework in 2023, mandating 100% low-risk asset backing, prompt redemption, and capital requirements, while allowing both bank and non-bank issuers. Tokens must be MAS-regulated to use the “stablecoin” label, ensuring quality and user confidence. Elsewhere, South Korea and Australia are drafting stablecoin rules, India remains restrictive, and China bans yuan-pegged stablecoins, though Hong Kong provides a workaround for Chinese firms. These developments position APAC as a key region for regulated stablecoin growth.

Compliance Costs & Global Arbitrage

New regulations will significantly increase compliance costs for stablecoin issuers, requiring funding for audits, regulatory capital, and reporting systems. Smaller or opaque issuers may struggle, potentially leading to market consolidation around larger, well-capitalized firms. Issuers may need compliance teams and legal counsel across jurisdictions. However, clearer regulations could broaden adoption, attracting corporates and fintechs that previously avoided stablecoins due to legal uncertainty.

Regulatory arbitrage remains relevant. Issuers often favor lenient jurisdictions—as seen with Tether’s early success in Hong Kong and the Caribbean amid U.S. regulatory gaps. As the U.S., EU, and Asia advance frameworks, fewer havens remain. Differences persist: the EU bans yield to tokenholders, while places like Bermuda or the UAE might permit yield-bearing stablecoins. Issuers may choose flexible bases for such offerings, provided global access remains.

Profitability will depend on regulation. Capital requirements or restrictions on reserve assets (e.g., only short Treasuries or non-interest-bearing Fed cash) would reduce interest income, acting as a tax on margins. Circle and similar firms appear willing to accept lower profits for scale and legitimacy. Tether, currently highly profitable under light oversight, may face pressure if stricter jurisdictions block unlicensed stablecoins—forcing it to either comply (and lower margins) or limit itself to less regulated markets.

Business Models and Revenue Shifts

Early stablecoin models prioritized growth over revenue, but rising interest rates and market maturity have shifted focus to profitability. Issuers now generate income from several sources and face evolving competition over revenue sharing.

Revenue Breakdown for Issuers

Interest on Reserves

In today’s high-rate environment, this is the primary revenue source. When users deposit $1 for 1 stablecoin, issuers invest reserves in short-term U.S. Treasuries, money market funds, or bank deposits. At scale, yields are substantial—e.g., 5% annual yield on $20 billion generates $1 billion/year. In 2024, Tether reportedly earned $13 billion in net profit, largely from interest on reserves, surpassing major banks and even BlackRock. Circle earned ~$770M in H1 2023, with USDC reserves averaging $30B. Issuers retain most interest income to fund operations and profits, unlike banks which pay depositors. However, as competition rises, some yield may be shared with users or partners.

Mint/Burn & Transaction Fees

Blockchain transfers usually incur no issuer fees, but institutions often pay redemption fees (e.g., Tether charges 0.1%, $1,000 minimum). Circle charges no standard USDC fees, though platforms using its APIs may. Retail transaction fees are rare, but enterprise clients may incur charges. Paxos reportedly takes small basis-point fees on transactions for white-label stablecoins like BUSD/PYUSD. Issuers may also earn from custody or treasury services—e.g., Circle Accountfor businesses.

Partnerships and Other Revenue

Issuers form revenue-sharing partnerships with fintechs, exchanges, and banks. In 2023, Coinbase and Circle agreed to split USDC interest income, allowing Coinbase to offer up to 4% APY to USDC holders. Issuers may also pay referral fees or rebates to wallets and payment firms, and share revenue from services like FX conversions (e.g., MoneyGram and Stellar’s USDC). Additional income may come from premium services like merchant APIs (Circle charges for Payments API usage). These partnerships expand stablecoin adoption while sharing revenue.

Impact of On-Chain Money Market Funds and New Entrants

The rise of tokenized money market funds (MMFs) from firms like BlackRock (BUIDL) and Franklin Templeton (BENJI), offering ~5% yield with stable value, is compressing stablecoin profit margins by attracting users seeking returns. These tokenized MMFs integrate into crypto wallets, allowing users to swap USDC for yield-bearing assetswhile maintaining dollar stability. The RWA (real-world asset) boom in DeFi has funneled billions into tokenized T-bills, pressuring stablecoin issuers like Circle (now offering USDC rewards via Coinbase) and Tether (which has yet to share yield) to pass through returns or risk client attrition. Meanwhile, new entrants—such as PayPal’s PYUSD, bank-issued tokens, and Agora’s AUSD—are also offering yield or incentives, intensifying competition. DeFi-native options like Overnight’s USD+, which embed yield, further signal that zero-yield stablecoins must adapt or face obsolescence.

Technological Innovations

Stablecoins now move seamlessly across multiple blockchains. Early stablecoins were limited to single networks, but today, USDC and USDT are natively issued on Ethereum, Tron, Solana, Polygon, Arbitrum, Avalanche, Binance Chain, and others. This allows users to access the same asset (1:1 redeemable for USD) across ecosystems—e.g., USDC on Ethereum for DeFi or on Solana for fast payments. Notably, USDT supply is largest on Tron, popular in Asia for low-cost transfers, while USDC is prominent on Ethereum and L2s.

New protocols support cross-chain swaps without bridges. For example, Circle’s CCTP enables burning USDC on one chain and minting on another atomically, enhancing chain-agnostic usability. Interoperability extends to wallets and platforms—stablecoins are integrated into wallets like MetaMask and Phantom, fintech apps via Stripe’s crypto tools, and even messaging platforms (e.g., Telegram bots for USDT transfers). Traditional finance is also integrating stablecoins—Visa’s Universal Payment Channels and Visa VTAP aim to connect blockchain payments to bank settlements, letting merchants accept stablecoins with fiat conversion.

The result is ubiquity and fungibility: a stablecoin on one network functions identically on others, enabling cross-chain arbitrage and consistent pricing globally.

Programmability – Smart Contracts and Automation

Stablecoins function as programmable money, enabling innovative applications via smart contracts.

DeFi Composability: Stablecoins are central to lending, trading, and yield protocols. Users can deposit USDC to earn interest or borrow assets, with contracts combining functions for yield tokenization and automated returns.

Real-Time Payments: Protocols like Superfluid allow streaming payments, e.g., real-time payroll or per-minute service fees. Some DAOs pay contributors this way, and Visa has piloted auto-payments via Ethereum smart contracts, replicating recurring billing.

Escrow and Conditional Payments: Stablecoins in smart contract escrow can automatically release funds upon verified outcomes, such as freelance delivery confirmation or parametric insurance triggers (e.g., flight delays via oracles).

Complex Instruments: Stablecoins are used as collateral and settlement in derivatives, liquidity provision, and trade finance. Smart contracts can automate payments upon events like IoT-confirmed goods delivery, replacing traditional clearing.

Visa’s VTAP and Institutional Integration

Visa launched its Tokenized Asset Platform (VTAP) in October 2024, offering banks stablecoin-as-a-service with APIs to mint, burn, and manage fiat-backed tokens on blockchain networks, ensuring compliance, secure issuance, and cross-chain interoperability. The first partner, BBVA, will pilot issuing euro and dollar tokens via Ethereum in 2025. VTAP allows banks to integrate tokenized payments into existing systems without blockchain expertise, enabling cross-border transactions (e.g., SGD to USD stablecoins) with seamless FX. Leveraging Visa’s 80M+ merchant network, stablecoins can be used at scale, with Visa handling settlement in fiat or stablecoins. Building on its USDC trials since 2021, VTAP also supports programmable finance—including automated loan disbursements and instant settlement of tokenized assets—positioning Visa as a neutral infrastructure layer connecting stablecoins to mainstream finance.

Security Improvements

Security enhancements are vital as stablecoins scale. Measures such as smart contract audits, formal verification, and multisig minting controls are expanding to reduce risks. For example, Circle’s “Circuit Breaker” on USDC can halt suspicious large transfers to prevent hacks. Projects are also developing insurance and custody solutions, including Nexus Mutual for custodial risk and Fireblocks' MPC custody for institutions.

Scalability has improved through Layer-2 networks like Arbitrum and Optimism, enabling faster, low-cost stablecoin transactions. Additionally, cross-chain bridge security is advancing; CCTP, for instance, eliminates locked bridge contracts, reducing vulnerability to attacks.

Risks and Challenges

The stablecoin market remains highly concentrated, with Tether (USDT) comprising ~two-thirds of supply and Tether + Circle controlling over 90%, creating a systemic single point of failure. A loss of confidence in USDT could trigger market-wide disruption, potentially worse than TerraUSD’s $40B collapse in 2022. Stablecoins depend on off-chain reserves (e.g., banks), exposing users to counterparty risk, as seen when USDC fell to $0.88 during SVB’s collapse in 2023. Redemption halts (e.g., Tether post-FTX) and blacklisting powers highlight centralization risks. Peg stability is fragile, with USDC/USDT briefly trading near $0.90 in volatile periods. Smart contract vulnerabilities (e.g., Acala’s $1.2B mint error) and bridge hacks (e.g., Wormhole’s $300M loss) add technical risk. Regulatory uncertainty further complicates growth, as actions like Paxos halting BUSD demonstrate. To mitigate, regulators are pushing reserve audits, redemption safeguards, and shutdown mechanisms, aiming to ensure financial stability as stablecoins evolve into systemically significant assets.

Future Outlook (2025–2030)

Between 2025 and 2030, stablecoins are expected to either integrate deeply into global finance or face challenges from strict regulation and CBDCs. Annual on-chain volume already reached $5.6T in 2024, with projections exceeding $20T by 2030, potentially surpassing card networks in areas like cross-border payments. Most likely, stablecoins will complement traditional rails, powering settlements for banks and platforms such as Visa and Stripe. While the IMFand BIS caution against risks and advocate for CBDC alternatives, they foresee coexistence under tighter oversight. Market concentration remains a concern—USDT holds ~66% share—and a failure could trigger systemic risks similar to TerraUSD’s $40B collapse. Still, institutions like BlackRock anticipate trillions in tokenized assets, with McKinseyreporting $120B tokenized by 2024. Market cap projections range from $300B (regulatory squeeze) to $2–3T (bull case), with upside in emerging market dollarization. Stablecoins’ role will depend on CBDC design: wholesale CBDCs could support stablecoin reserves, while retail CBDCs may compete. By 2030, tokenized deposits and bank-issued stablecoins may underpin financial settlement infrastructure, while stablecoins facilitate aid disbursement, remittances, and new monetary tools in high-inflation regions.

Conclusion

By 2030, stablecoins are expected to be integral to global finance, especially in cross-border payments, B2B transactions, and digital asset settlement. Market cap could range from hundreds of billions to a few trillion, with tight regulatory frameworks ensuring stability. Though less “wild,” stablecoins will enable broader innovation, marking a shift toward a more efficient and inclusive monetary system. The next five years will be pivotal as stablecoins evolve from niche tools to systemic infrastructure.

Sources

Highly recommended by us:

The State of Stablecoins 2025: Supply, Adoption & Market Trends

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer's views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.