Circle’s IPO: USDC’s Next Chapter

Circle Internet Financial was founded in October 2013 by Jeremy Allaire (a serial internet entrepreneur) and Sean Neville. Allaire’s vision was to harness cryptocurrency technology to revolutionize online payments.

In early interviews, he described Bitcoin and digital currency as a “once-in-a-lifetime opportunity to shape the future of the Internet and global commerce,” aiming to make payments “easier, more secure and less costly for consumers and businesses.”

Circle’s initial mission was essentially to create a “universal system of plumbing for money” on the internet, analogous to how HTTP enables information exchange (a phrase Allaire often used to illustrate the company’s long-term goal).

Early Products and Pivots

In its first few years, Circle launched consumer-facing services to simplify using crypto for payments. It obtained the first-ever New York BitLicense in 2015 to operate a digital currency service, reflecting an early focus on regulatory compliance. Circle’s business model evolved significantly over time:

2013–2016: Built a Bitcoin-based payment app (Circle Pay) to let users send and receive money with digital currency. The company raised over $135 million in venture capital during this period, including a $50 million round led by Goldman Sachs in 2015, highlighting strong early backing from financial institutions.

2018: Pivoted toward crypto trading services. Circle acquired Poloniex, a major cryptocurrency exchange, in early 2018, seeking to expand into the trading market. However, this move proved ill-fated – Circle sold Poloniex just a year later (2019) at a reported $156 million loss. Around the same time, Circle also sold off other non-core products (e.g. a mobile investing app waager Digital in 2020) to refocus the business.

2018–2019: Launch of USDC: Circle’s true “killer app” emerged with USD Coin (USDC). In October 2018, Circle and Coinbase jointly formed the CENTRE Consortium and launched USDC, a U.S. dollar-pegged stablecoin. USDC is fully backed 1:1 by U.S. dollar assets and was introduced as a regulated, transparent alternative to other stablecoins. This marked a pivotal shift from consumer app development to becoming a stablecoin issuer and crypto-financial infrastructure provider.

2020–2021: Having shed its exchange operations, Circle doubled down on growing USDC’s ecosystem. By early 2020, USDC’s circulating supply was modest (~$500 million, versus ~$4.2 billion for market-leader Tether’s USDT). But Circle’s focus on transparency and compliance drove rapid growth. During the 2020–2021 crypto boom, USDC’s circulation ballooned into the tens of billions, validating Circle’s pivot. Notably, Circle secured a $110 million Series E round in 2018 to support the USDC launch, and later announced a SPAC merger in 2021 as USDC adoption took off.

Strategic Partnerships

Throughout its evolution, Circle has forged major partnerships to bring stablecoins into mainstream finance:

Coinbase – USDC Consortium: As a co-founder of the CENTRE Consortium, Coinbase launched USDC on its platform from day one and took a minority stake in Circle in 2023. This move dissolved the consortium, making Circle the sole issuer of USDC, while Coinbase now shares 50% of the reserve interest income. Coinbase has been central to USDC’s distribution across both retail and institutional channels, reinforcing a joint commitment to regulated stablecoin adoption.

Visa – Global Payments: Circle joined Visa’s Fintech Fast Track in 2020, leading to a 2021 pilot using USDC for Ethereum-based settlements. In 2023, Visa scaled this initiative, settling millions in USDC across Ethereum and Solana with partners like Worldpay and Nuvei. Circle’s CEO noted this collaboration showcases how stablecoins can modernize global payments.

BlackRock – Asset Management: In 2022, Circle raised $400M from BlackRock, Fidelity, and others. BlackRock also became a key manager of USDC reserves, leading to the launch of the Circle Reserve Fund, a regulated government money market fund now holding most of USDC’s cash. The partnership brought institutional trust and improved Circle’s reserve management.

Institutional Alliances: Circle built further alliances with Stripe, MoneyGram, Mastercard (crypto cards), and major banks like JPMorgan and BNY Mellon. As a founding member of the Blockchain Association, Circle continues to engage proactively with regulators. These relationships helped position Circle as a core bridge between traditional finance and the crypto ecosystem.

USDC’s Role in Global Markets

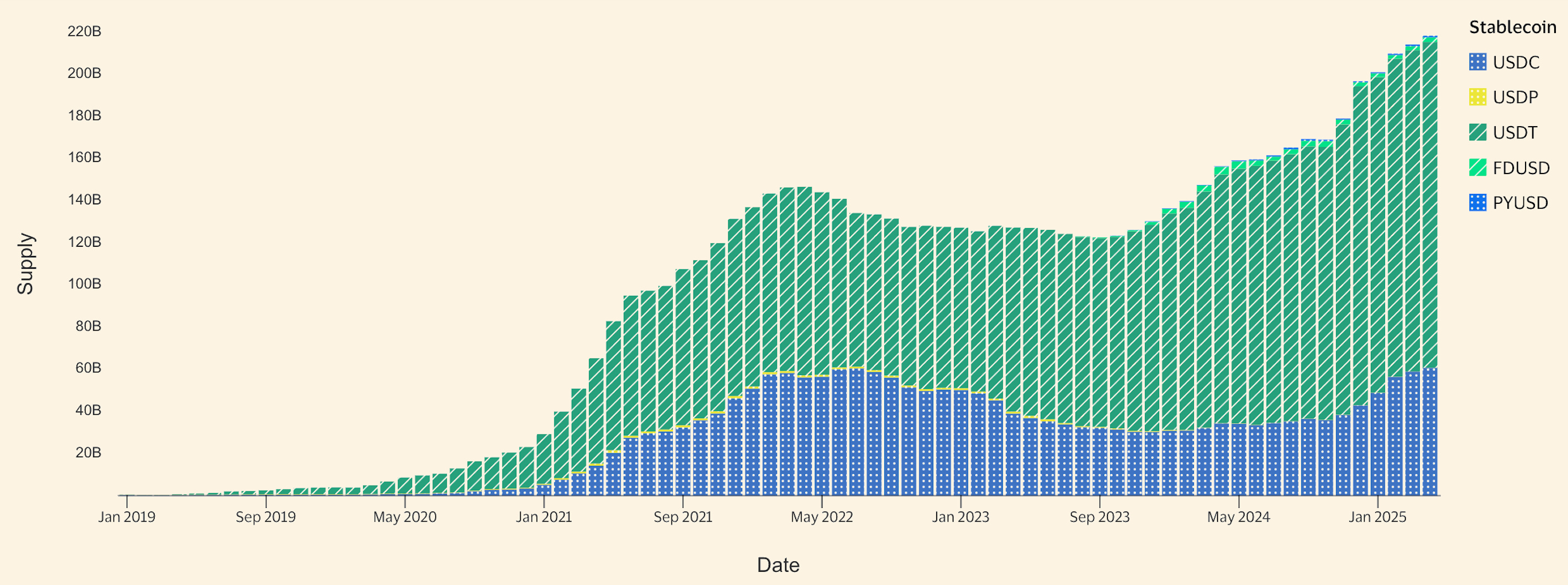

USDC (USD Coin) is currently the second-largest stablecoin globally (behind only Tether’s USDT) and plays a pivotal role in crypto markets. Its market capitalization has at times rivaled USDT’s, though each has seen shifts in dominance. In early 2022, USDC was on a trajectory to possibly overtake USDT – after Terra’s collapse in May 2022, USDC grew from ~$49 billion to $55 billion in circulation as investors fled riskier stablecoins, while USDT’s market cap fell from ~$83 billion down to ~$66 billion. USDC’s rise at Tether’s expense during that period was widely attributed to Circle’s greater transparency and regulatory standing (Tether faced criticism for opaque reserves and had been reducing its risky commercial paper holdings).

However, market share dynamics reversed in 2023 amid U.S. banking turmoil and regulatory pressures. USDT pulled ahead strongly as the dominant stablecoin, especially after a U.S. banking crisis in March 2023 temporarily shook confidence in USDC. When Silicon Valley Bank failed in March 2023, Circle revealed $3.3 billion of USDC’s cash reserves were stuck at the bank. USDC briefly “broke the buck,” de-pegging to about $0.88, before recovering once U.S. regulators backstopped SVB deposits. In the week of that crisis, investors redeemed a net $6 billion out of USDC. USDT, which had no direct exposure to U.S. banks, gained relative ground. By early 2024, Tether’s USDT commanded roughly 70%+ of stablecoin market cap (around $97 billion of $137 billion total in Feb 2024), while USDC’s share had fallen to about 20% (circa $28 billion).

Stablecoin market share has oscillated with market conditions. In 2023, USDT’s dominance grew to ~63%, while USDC’s share dipped but rebounded by early 2025 to ~25% amid renewed confidence. The collapse of algorithmic stablecoin UST in 2022 led investors toward asset-backed stablecoins like USDC.

Current Status

As of Q1 2025, USDC is again on a growth trajectory. Circle reports ~$60 billion USDC in circulation (March 2025), reflecting a 78% year-over-year increase in circulation. This resurgence (from a low of ~$24 billion in late 2023) suggests recovering market confidence and new use cases driving demand. USDC now constitutes approximately one-quarter of the total stablecoin market by value, vs. about two-thirds for USDT. USDC and USDT together dominate over 90% of the stablecoin space by supply, with smaller players like BUSD (Binance USD) and DAI occupying the remainder. Notably, algorithmic stablecoins (which attempt to maintain pegs via algorithms rather than full reserves) have largely fallen out of favor after high-profile failures. TerraUSD’s collapse to zero in May 2022 underscored the systemic risks of unbacked stablecoins, leaving USDC and USDT (both fully reserve-backed) as the trusted options. Circle’s USDC benefited from this flight to safety – regulators and users alike began to view fully collateralized stablecoins as the prudent model.

Adoption in DeFi

USDC is deeply integrated into the decentralized finance (DeFi) ecosystem. It is often the stablecoin of choice on DeFi platforms due to its transparency and reliability. Many decentralized protocols rely on USDC for liquidity and as a stable unit of account:

On lending platforms (like Aave and Compound), USDC is one of the top borrowed and supplied assets, used for gaining yield or leverage. Its predictable value makes it ideal collateral for crypto-backed loans.

On decentralized exchanges (DEXs), USDC pairs facilitate trading between crypto and stable dollar value. For example, pools like USDC/ETH on Uniswap are among the highest-volume pairs, providing crucial liquidity with lower volatility.

Stablecoin swap pools (Curve Finance, etc.) heavily feature USDC. Users swap between USDC, USDT, DAI and others with minimal slippage. USDC’s presence in these pools rose after 2022 as it was seen as lower risk than Tether or algorithmic coins.

MakerDAO’s DAI stablecoin is partially collateralized by USDC (via its Peg Stability Module), meaning Maker holds billions of USDC to backstop DAI’s peg. This “centralized collateral” in a decentralized stablecoin sparked debate, but it underscores USDC’s role as a reserve asset in DeFi.

In summary, USDC has become de facto digital dollar infrastructure in DeFi. Its usage goes beyond crypto trading – it underpins DAO treasuries, NFT marketplaces, and on-chain FX markets. Circle has fostered this by expanding USDC to 19+ blockchains (including Ethereum, Solana, Avalanche, Tron, and many new chains in 2023–24), making USDC ubiquitously available across ecosystems.

Enterprise and Real-World Adoption

Beyond the crypto-native realm, USDC is increasingly used in traditional contexts for payments and settlements:

Cross-Border Payments: Businesses in emerging markets are adopting USDC for cheaper and faster cross-border transactions. For instance, a manufacturer in Brazil can pay a supplier in Nigeria using USDC, avoiding the slow SWIFT system and multiple correspondent banks. Stablecoins eliminate conversion fees and delays, delivering near-instant settlement. In 2024, startups facilitating B2B remittances in Africa and Latin America (e.g. Yellow Card, Conduit) saw transaction volumes double as companies embraced USDC for trade payments. The cost savings are significant – sending $200 from the U.S. to Colombia via stablecoin costs pennies (<$0.01) versus ~$12 using legacy remittance channels.

Treasury Management: Even large corporates have begun experimenting with stablecoins. In 2024, SpaceX (Elon Musk’s rocket company) reportedly turned to stablecoins by partnering with a startup to accept customer payments in various currencies that are instantly converted to USDC for treasury management. This kind of use case shows stablecoins being used as working capital tools, not just trading instruments. USDC’s stability and liquidity (instant convertibility to cash) make it attractive for corporate treasury operations, especially in markets with less reliable banking.

Fintech Integrations: Major fintech and payment processors have integrated USDC. Stripe, for example, enabled payouts in USDC for freelancers and sellers in certain countries where traditional payouts are slow or costly. MoneyGram launched a service allowing cash funding and payout of USDC in various countries, bridging physical cash and digital dollars. Circle’s APIs also power neobank apps that offer accounts denominated in USDC as an alternative to local currency in high-inflation economies.

Visa & Mastercard Pilots: As noted, Visa is settling transactions in USDC with merchants. Mastercard has run pilots with Circle (like cards that let users pay via USDC balances). These initiatives blur the line between credit card networks and blockchain networks, hinting at a future where stablecoins might circulate as freely as fiat for commerce.

Global Reach: In inflationary emerging markets (Latin America, Africa, Middle East), stablecoins serve as a dollar substitute for many individuals. Both USDT and USDC have seen organic adoption as a hedge against local currency devaluation. Circle has capitalized on this by promoting “global digital dollar access” use cases – enabling anyone with a phone to hold a stable USD asset. In Argentina and Turkey, for example, citizens use USDC via exchanges or P2P markets to store savings in dollars amid 50%+ inflation locally. While Tether (USDT) has historically been more widely used by individuals in some regions (due to its longer history and sometimes easier accessibility), USDC’s credibility has begun attracting more emerging market users and fintechs seeking a fully-reserved, compliant dollar token.

Regulatory Positioning

Circle has deliberately positioned USDC as the trusted, compliant stablecoin, engaging proactively with regulators in the U.S. and abroad:

In the U.S., Circle is a licensed money transmitter and has consistently emphasized compliance with laws (e.g. KYC/AML). Circle was an early recipient of New York’s BitLicense in 2015, demonstrating regulatory bona fides when many crypto companies avoided stringent licensing. Circle’s Chief Strategy Officer Dante Disparte and CEO Jeremy Allaire have frequently engaged with policymakers. Allaire testified to the U.S. Senate in 2021, advocating for reasonable stablecoin oversight to integrate them into the financial system. Circle has supported the push for federal stablecoin legislation, arguing that clear rules would cement the U.S.’s role in crypto innovation while protecting consumers.

Interactions with U.S. Regulators: Circle’s attempt to go public via SPAC in 2021–2022 meant filing extensive disclosures to the SEC, which forced a high level of transparency (Circle had to provide audited financials and reserve data to regulators). While the SEC did not ultimately approve the SPAC merger (more on that later), Circle emerged with a reputation for being an open book relative to other crypto firms. Circle also has cooperated with law enforcement – famously, in August 2022, after the U.S. Treasury sanctioned a crypto mixer (Tornado Cash) for illicit use, Circle froze about $75,000 of USDC in sanctioned addresses, showing it will enforce U.S. sanctions on its network. This move drew some criticism from decentralization advocates, but it underscored Circle’s compliance-first stance.

Regulatory Challenges: Despite Circle’s posture, the U.S. regulatory environment was uncertain through 2023. Stablecoins exist in a gray area – not classified as securities by default, but lacking a comprehensive regulatory framework. U.S. bank regulators in early 2023 warned banks about crypto-related liquidity risks (mentioning stablecoin reserves runs). The lack of a federal stablecoin law meant Circle had to navigate state-by-state regimes and the risk that regulators (or Congress) could introduce new requirements. This uncertainty likely contributed to the SEC’s hesitation on Circle’s SPAC. By late 2023, however, progress was being made: a proposed Clarity for Payment Stablecoins Act advanced in Congress with bipartisan support. By 2025, the political climate shifted – the incoming administration in 2025 signaled a more crypto-friendly approach, with a new SEC Chair nominee pledging a “rational” regulatory stance. This more supportive tone at the federal level bodes well for USDC, as it reduces regulatory tail-risk.

Global Regulators: Circle actively engages outside the U.S. as well. It pursued licenses in key jurisdictions – for example, Circle Singapore obtained a Major Payment Institution license in 2023, allowing it to offer digital payment token services under the Monetary Authority of Singapore’s oversight. In Europe, Circle became the first stablecoin issuer approved under the EU’s MiCA regulation in 2024. MiCA (Markets in Crypto-Assets) provides a pan-European framework for stablecoins, and Circle preemptively met its standards (including capital, liquidity, and disclosure requirements). Circle also secured registration in France as a Digital Asset Service Provider (DASP) in 2023 to prep for euro-denominated stablecoin expansion. These steps mean USDC will be one of the few fully compliant stablecoins in both the U.S. and EU, easing adoption by traditional institutions. Circle is effectively setting the benchmark for regulatory compliance among stablecoin issuers, which could become a competitive moat.

International Collaboration: Circle has aligned with bodies like the Financial Stability Board (FSB) and engaged with central banks on how stablecoins can coexist with future central bank digital currencies (CBDCs). While some governments (e.g. China) ban private stablecoins, others are embracing regulated ones – e.g. Japan’s new stablecoin law or the UK’s proposals to treat stablecoins as a form of e-money. Circle’s transparency likely makes USDC one of the few private stablecoins regulators are comfortable with. Notably, in late 2022 Circle announced plans to seek a federal bank charter to become a digital currency national bank, though it has put that on hold pending clearer legislation. The company’s long-stated aim is to be a fully regulated, full-reserve banking entity for the digital age, which reflects its strategy of working within regulatory frameworks rather than against them.

Financial and Capital Markets Profile

Circle has raised substantial private capital over its lifespan, evolving from a venture-backed startup to a multibillion-dollar enterprise. Key funding milestones include:

2013–2016: Raised ~$135 million across Series A through D, including notable investors like Accel, General Catalyst, and Goldman Sachs. Goldman’s involvement in 2015 was seen as validating Circle’s approach to Bitcoin.

May 2018: $110 million Series E led by Bitmain (the Chinese crypto mining giant) at a nearly $3 billion valuation. This round was explicitly aimed at building out USDC and the CENTRE stablecoin framework.

Late 2019: Circle sold its Crowdfunding division and raised some strategic funds (e.g. $25 million from Digital Currency Group, which also involved a partnership to launch Circle’s yield product).

July 2021: Announced a planned merger with Concord Acquisition Corp, a SPAC, which initially valued Circle at $4.5 billion. In February 2022, as USDC’s growth far outpaced projections, the deal was amended to value Circle at $9 billion. This implied a dramatic increase in enterprise value thanks to USDC’s success in 2021.

April 2022: $400 million funding round (private raise concurrent with the SPAC process) with investors including BlackRock and Fidelity. This round (which closed by Q2 2022) reinforced the $9 billion valuation and brought in strategic capital and partnerships (BlackRock, as noted, became an asset manager for reserves).

Late 2022: The SPAC deal failed to close (terminated in Dec 2022), leaving Circle private. Despite that setback, Circle by then had a war chest from the recent raise and continued operating strongly. By end of 2022, some reports pegged Circle’s implied valuation in secondary markets around $8–9 billion, though the public market conditions were unfavorable.

2023: No major public funding rounds were announced; however, a significant ownership restructuring occurred in August 2023 when Coinbase acquired an equity stake in Circle as part of dissolving the Centre Consortium. The size of Coinbase’s stake wasn’t disclosed, but it’s described as a minority position. This deal likely involved little or no cash but rather a revenue-sharing arrangement (Coinbase getting 50% of USDC reserve revenue) in exchange for equity. It suggests an implicit valuation for Circle, but specific numbers remain confidential. Notably, Circle’s latest SEC filing listed Accel, General Catalyst, Breyer Capital, IDG, and Oak Investment as owners of >5% pre-IPO, indicating those early VC backers still hold significant equity.

As Circle now prepares for an IPO in 2025, reports indicate it is aiming for a valuation in the $4–5 billion range. This is roughly half the peak $9 billion SPAC figure, reflecting the more subdued crypto market in 2022–2023 and a reset of expectations. However, it’s still a hefty valuation for a fintech company with essentially one primary product (USDC). Circle has hired major banks (J.P. Morgan and Citi) as lead underwriters for the IPO, signaling confidence that institutional investors will support the offering.

USDC Reserve Composition

USDC’s strength is its high-quality, transparent reserves, critical to Circle’s financial standing. Each USDC token is backed by equivalent USD reserves held by Circle. As of April 2025, these reserves are conservative and highly liquid:

Approximately 80% or more are in the Circle Reserve Fund (USDXX), an SEC-registered government money market fund managed by BlackRock. This fund invests primarily in short-term U.S. Treasury bills, overnight Treasury-backed repurchase agreements, and cash, totaling over $53.5 billion, closely matching USDC circulation. Daily disclosures by BlackRock ensure market-leading transparency, unlike competitors like Tether, which provide only quarterly summaries.

About 20% or less is held in cash deposits across multiple banking partners (e.g., BNY Mellon, Customers Bank, Cross River Bank), minimizing risk exposure. Post-SVB, Circle began weekly disclosures of bank holdings, enhancing liquidity and security with automated minting/redemption through Cross River Bank and Bank of New York Mellon.

Circle further enhances credibility with weekly reserve updates and monthly third-party attestations by Deloitte, confirming reserves consistently meet or exceed circulating USDC. This rigorous reporting distinguishes Circle, ensuring its reserves are essentially risk-free assets (short-term U.S. government debt and cash), minimizing credit and interest-rate risks.

Circle Yield Product

Circle briefly offered Circle Yield, an institutional USDC lending program launched in 2020 with Genesis Global Capital facilitating over-collateralized loans. During the 2022 crypto credit crisis, Genesis halted withdrawals (affected by Three Arrows and FTX), prompting Circle to quickly wind down Yield. At the time, Circle’s exposure to Genesis was minimal—only $2.6 million in over-collateralized loans—and it proactively reduced Yield rates to 0% before Genesis' collapse. By early 2023, Circle Yield ended without material losses, unlike programs such as Gemini Earn. Since then, Circle emphasizes that USDC reserves remain liquid and primarily in government bonds, reflecting its cautious approach. Circle now generates revenue mainly from low-risk interest income rather than credit activities.

Revenue Model

Circle's revenue now primarily comes from interest earned on USDC reserves. It holds billions in short-term U.S. Treasuries and bank deposits backing USDC, generating significant interest income—$1.68 billion in 2024, up from $1.45 billion in 2023. With around $40 billion at 4% yield, interest alone could reach ~$1.6 billion yearly. Coinbase receives 50% of this interest income per a 2023 agreement, meaning Circle's reported revenue factors this sharing arrangement.

Transaction and API fees (from USDC issuance, institutional services, and payment APIs) are minor but provide diversification and potential growth. Past revenues from trading and subsidiaries (Poloniex, SeedInvest) are now discontinued, narrowing Circle’s focus to a wholesale banking model reliant on interest income.

Circle recently turned profitable, reporting net income of $268 million in 2023 and $156 million in 2024, with the profit drop reflecting higher operational costs and Coinbase's revenue split. This underscores Circle’s dependence on interest rates—higher rates generate substantial profits, but a return to low rates could significantly impact financial performance, a crucial factor for investors.

Recent Financial Performance

Circle’s financials for the last two years (which it disclosed in its IPO filing) are quite robust:

2023: Revenue $1.45B, Net income $268M due to first full year of significant interest earnings and fewer revenue-sharing costs with Coinbase (new deal began in Q4). Possible one-time gains or lower expenses.

2024: Revenue grew to $1.68B, but net income dropped to $156M due to higher costs—investments for growth, public company preparations, compliance, ecosystem rewards, and possibly interest payouts to USDC holders. Still, profitability validates stablecoin business model viability.

Balance Sheet: By end-2024, significant cash reserves and shareholder equity over $1B. Liabilities linked to USDC reserves (invested, not traditional debt), akin to money market fund management.

IPO Details (2025):

Expected raise of ~$750M at ~$5B valuation (~15% public ownership).

Funds to support corporate growth, geographic expansion, R&D (e.g., EURC stablecoin), acquisitions, and meet potential regulatory capital requirements.

Underwriters: J.P. Morgan, Citigroup; expected NYSE ticker "CRCL," IPO anticipated Q2/Q3 2025.

Valuation & Comparables:

At $5B, Circle valued at ~30x earnings, ~3x revenue—reasonable for fintech growth, less volatile than Coinbase (valued ~$50-60B, but less predictable revenue). Comparable fintechs like PayPal trade at ~4x sales and under 20x earnings; banks/money fund managers typically lower multiples.

Market Sentiment:

Circle’s IPO tests investor appetite for crypto infrastructure post-2022 bear market. Sentiment cautiously optimistic due to crypto market recovery, stablecoin growth, and Circle’s profitability.

Risks: regulatory uncertainty, competition, reliance on interest rates.

Positive: disciplined approach (traditional IPO vs. SPAC), two years audited financials, transparency emphasized by CEO Jeremy Allaire.

Governance & Executive Leadership

Circle is led by co-founder and CEO Jeremy Allaire, an experienced entrepreneur known for founding Allaire Corp (ColdFusion platform) and Brightcove (IPO 2012). He positions Circle as essential "internet money" infrastructure, emphasizing regulatory dialogue, compliance, and transparency. Co-founder Sean Neville, former President and co-CEO, stepped back from operations around 2019 but remains an independent director and significant shareholder.

The broader executive team includes seasoned professionals from both fintech and traditional finance:

Jeremy Fox-Geen – Chief Financial Officer (CFO): Joined Circle in 2021 from the fintech sector. He has overseen Circle’s financial strategy through the rapid growth of USDC and prepared the company for public-readiness. He often spoke about Circle’s path to going public and financial resilience.

Dante Disparte – Chief Strategy Officer & Head of Global Policy: Disparte leads Circle’s engagement with governments and regulators worldwide. A respected voice in DC policy circles, he has been pivotal in shaping Circle’s global strategy (e.g., navigating EU’s MiCA, obtaining licenses abroad). He frequently articulates Circle’s views on risk management.

Mandeep Walia – Chief Compliance Officer (CCO): Circle’s compliance head (hired from PayPal) has ensured Circle’s licensing in numerous jurisdictions and spearheaded programs like sanctions compliance.

Product and Engineering Heads: Circle’s growth in product lines (like Circle Accounts, APIs, and cross-chain protocol) has been led by VP of Product Joao Reginatto and CTO Li Fan (a former tech lead at Tencent and Google). They oversee technological integration of USDC across blockchains and new product R&D (including a potential Circle-issued digital euro, EURC).

Board Composition

Circle’s board combines founders, investors, and independents:

Jeremy Allaire (Chairman) – founder and management voice.

Sean Neville – co-founder, continuity.

Investors (>5%) represented by:

Jim Breyer – Breyer Capital CEO, early Facebook investor; led Series A, deep tech expertise.

David Orfao – General Catalyst partner, operational experience, board since 2013.

Likely board presence from IDG Capital (early Asia expansion) and Oak HC/FT (fintech experience, invested 2020).

Coinbase notably declined a board seat despite its 2023 stake, leaving control with management and traditional investors. Post-IPO, expect additional independent directors (regulatory/banking veterans) for governance standards.

Governance Practices

Circle says going public will enhance its governance. It already operates like a public firm, with monthly attestations and past SEC filings. As a listed company, Circle will adopt an independent audit committee, formal SEC reporting (10-Ks, 10-Qs), and Sarbanes-Oxley controls to strengthen transparency. Allaire described the IPO as an extension of Circle’s transparency ethos—highlighting governance as a priority.

A critical area is risk management. Circle oversees tens of billions in assets, so its risk committee (at board or management level) is key. Ensuring liquidity for USDC redemptions is the top focus. Policies like cash buffers and diversified banking partners proved effective during the SVB crisis. As a potential systemic stablecoin issuer, Circle’s governance includes coordination with regulators, particularly if it seeks a banking license or adapts to stablecoin regulation.

Ownership (Pre- and Post-IPO):

Pre-IPO: Ownership is concentrated among early VCs and management. Firms holding ≥5% include Accel, General Catalyst, Breyer Capital, IDG, Oak HC/FT. Allaire likely owns ~5–10%, with similar range for Sean Neville. Coinbase’s stake is “small” (~5% or less), likely tied to future revenue sharing. BlackRock and Fidelity didn’t make the 5%+ list—suggesting they hold ~2–3%, possibly via convertible notes or post-money dilution.

Assuming a ~$4–5 B valuation, a $750 M raise would dilute pre-IPO holders by ~15%. Cap table estimates: Accel and General Catalyst ~15% each, Allaire ~7%, Breyer, IDG, Oak ~5% each, Coinbase ~4%, others ~24%, new public holders ~15%. Circle also likely reserves ~10–15% for employee equity incentives, aiding fintech/banking talent retention.

Post-IPO: Public investors will own ~15%, though this could rise if insiders sell secondary shares. Long-time VCs might take this chance to realize gains, though lock-up agreements will delay sales. No dual-class shares are planned—Circle will have a single class (1 share = 1 vote). Initially, insiders + VCs will still control ~80–85%, but over time, that will dilute. VCs may distribute shares to LPs post-lockup, growing public float.

Strategic stakes (e.g., from banks or networks) haven’t been announced but could emerge. Board governance remains VC-heavy for now, with Breyer and Orfao expected to stay on through the IPO. Coinbase will likely coordinate closely with Circle but not influence governance via board seats.

Challenges, Setbacks, and Regulatory Tensions

Terminated SPAC Deal (2021–2022)

Circle planned to go public via a SPAC merger with Concord Acquisition Corp at a $4.5B valuation (later $9B due to USDC growth). The deal collapsed in Dec 2022 amid crypto market turmoil (Terra, Celsius, FTX) and SEC delays. CEO Allaire cited regulatory timing, not fundamentals, and noted Circle’s strong capital position after a $400M raise.

IPO Delays and Market Conditions

Following the SPAC fallout, Circle pursued a traditional IPO cautiously in a tough 2023 market. USDC’s market cap fell from $50B to low $30Bs, and Fed rate hikes plus regulatory pressure post-FTX added headwinds. With conditions improving in 2024, Circle filed its S-1 in April 2025—nearly two years late. Still, it sustained operations, morale, and key partnerships, including with Coinbase.

Regulatory Tensions

Circle’s role as a stablecoin issuer brings complex oversight:

SEC Scrutiny: USDC is labeled a payment token, not a security, but lack of clarity delayed SPAC approval. 2025 legislation may shift oversight to the Fed or OCC.

Banking Concerns: The SVB crisis in March 2023 exposed regulatory worries over stablecoin banking. Circle responded by diversifying partners and seeking a national banking charter.

Global Moves: After NY regulators shut down Paxos’s BUSD, Circle dissolved the Centre consortium, taking full control of USDC for simpler governance.

Market Rivalry: Circle promotes USDC’s transparency versus Tether, maintaining real-time reserve reporting and risk controls.

Transparency and Audits

Circle shifted to weekly reserve updates and engaged Deloitte for full audits ahead of IPO. Its real-time reporting during the SVB crisis helped build trust. Quarterly disclosures post-IPO are expected to boost transparency further.

Crypto Market Turmoil (2023–24)

Circle faced major stress events:

Terra Collapse (May 2022): Highlighted USDC’s fully-reserved model.

FTX Implosion (Nov 2022): Just $2.6M exposure via Genesis.

SVB Crisis (Mar 2023): Managed $3.3B exposure swiftly, maintaining USDC peg after $6B redemptions.

Slower Markets: Despite lower trading volumes, rising interest income and cost control kept revenue stable—no layoffs.

Reputational & Competitive Pressures

Binance Shift: Binance’s move to BUSD in 2022 hit USDC’s market share, though regulatory pressure on BUSD in 2023 eased the impact.

Tech & Compliance: Circle maintains strong smart contract security and compliance standards, despite challenges scaling across blockchains and criticism from privacy advocates.

Key Metrics & Market Signals to Watch

As Circle transitions to public markets, investors should monitor several key metrics to assess USDC’s adoption, stability, and Circle’s financial health. Tracking the total supply (market capitalization) and monthly net issuance or redemption of USDC provides insights into adoption trends or declining user confidence. Investors should compare USDC’s growth against the broader stablecoin market.

Monitoring on-chain transaction velocity and volume reveals how actively USDC is utilized, with higher velocity indicating frequent usage. Comparing USDC’s velocity with competitors like USDT can highlight its commercial appeal.

Investors should closely examine the reserve composition between cash and Treasuries, as it significantly impacts Circle’s interest income. Observing the 7-day yield (USDXX) provided by BlackRock and monitoring interest income per $1 billion of USDC, currently around $50 million annually at a 5% yield, is essential. Additionally, reserve durations should remain short-term to minimize risk. Circle’s potential revenue from management fees via the Circle Reserve Fund is another area to watch.

Transparency metrics, such as monthly attestation reports detailing backing ratios, reserve composition, banking partners, and auditor statements, are crucial indicators of financial stability. Expanding adoption can be measured through unique addresses holding USDC, enterprise integrations, and significant off-chain use cases.

The competitive landscape, including market share shifts against major stablecoins like Tether (USDT) and new entrants such as PayPal’s PYUSD, provides important context for Circle’s positioning.

Finally, Circle’s quarterly financial reports will shed light on revenue growth, diversification, cost management (operating expenses relative to revenue), profitability margins, and cash reserves. Post-IPO, valuation metrics compared to peers like Coinbase, PayPal, and traditional fintech companies will become significant benchmarks.

Conclusion

Circle enters 2025 on the cusp of achieving what it set out to do over a decade ago – integrate the crypto-dollar (USDC) into the fabric of the global financial system, under the scrutiny of public-market investors. The company’s foundational choices (full reserve backing, regulatory engagement, partnership model) have thus far proven wise, yielding widespread adoption of USDC and a sustainable revenue engine. Yet, the journey ahead will require navigating competitive pressures, regulatory evolution, and market fluctuations with the same prudence Circle showed in overcoming past setbacks. By monitoring the key metrics and signals outlined above, institutional investors can stay informed on Circle’s health and progress. Circle’s IPO will not just be a liquidity event; it will be a barometer for the broader crypto industry’s maturation, offering a window into how a crypto-native company can perform when held to the standards of traditional finance. With USDC at its core, Circle’s story in 2025 is one of convergence between fintech and crypto – and its successful public debut could mark a significant step in stablecoins moving from the periphery of finance firmly into the mainstream.

Sources

https://visaonchainanalytics.com/transactions#adjusted-transaction-methodology

https://www.sec.gov/Archives/edgar/data/1876042/000119312525070481/d737521ds1.htm

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer's views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.