Inside Jump Crypto: $1.3B Terra Trade, $321M Wormhole Rescue & More

Jump Crypto operates as the crypto trading and infrastructure division of Jump Trading, engaging in proprietary market-making, strategic venture investments, and protocol development. This case study examines how (and how well) the broader Jump Trading organization’s strengths – ultra-low latency tech, quantitative culture, rigorous risk management, and deep capital reserves – enable Jump Crypto’s competitive position. We also map linkages to Jump Capital (Jump’s venture arm) and other affiliates, while explicitly distinguishing each entity to avoid conflation.

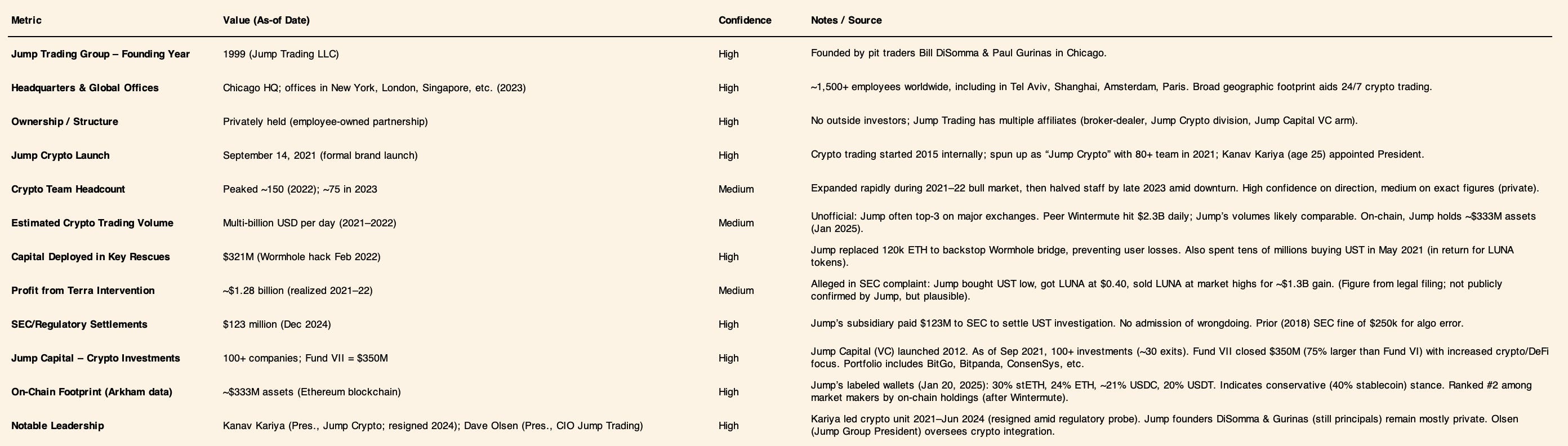

We cover Jump’s origins (late 1990s) through its crypto foray (2015 onward), with emphasis on 2017–present. Developments through July 17, 2025 are included (e.g., regulatory actions in late 2024).

Despite being privately held and secretive, Jump’s influence in both TradFi and crypto is far-reaching. It has become a top liquidity provider on major centralized exchanges and a significant player in DeFi (often providing algorithmic liquidity on decentralized exchanges). Jump Crypto has also taken on ecosystem-building roles – for example, contributing to Pyth Network (an on-chain oracle) and developing Firedancer (a high-performance Solana client). However, Jump’s aggressive moves have sometimes courted controversy: notably, its covert intervention to stabilize Terra’s UST stablecoin in 2021 (for which it later faced legal scrutiny) and its central role in backstopping the Wormhole bridge hack in 2022. As regulators increase oversight of crypto market-makers, Jump faces new challenges in balancing innovation with compliance.

Executive Summary of Key Findings

Market Leadership Through Technology & Scale: Jump Trading’s expertise in high-frequency trading (HFT) infrastructure – including proprietary algorithms and microwave networks – translated directly into a moat in crypto market-making. Jump Crypto’s ultra-low latency systems and cross-market arbitrage strategies have made it one of the largest liquidity providers in crypto, trading across centralized exchanges (e.g., Binance, Coinbase) and decentralized protocols. The firm’s substantial capital base (privately funded; no outside shareholders) allows it to deploy hundreds of millions in liquidity, enabling tight spreads and market depth that smaller competitors cannot match.

Integrated Business Model (TradFi + Crypto + VC): Jump operates an integrated model: Jump Crypto (prop trading & tech builds) works alongside Jump Capital (a venture arm with 100+ investments). This provides a virtuous cycle – Jump often invests in exchanges or protocols and then serves as a key market maker for them. For example, Jump was a founding code contributor to Solana’s Pyth Network and the Wormhole bridge while simultaneously profiting from trading on Solana. This multi-pronged approach offers synergy (insider technical knowledge and early investment opportunities) but also requires careful conflict management.

Notable Interventions & Risk Appetite: Jump Crypto has repeatedly acted as a market “backstop” during crises. In February 2022, when the Wormhole cross-chain bridge was hacked for 120k ETH, Jump stepped in and replenished ~$321 million to make users whole – a dramatic demonstration of its liquidity strength. Earlier, in May 2021, Jump quietly intervened to defend the UST stablecoin’s $1 peg, spending tens of millions (for which it received deeply discounted LUNA tokens). These moves protected broader markets (preventing immediate collapse of Wormhole, temporarily shoring up Terra) and earned Jump sizable profits (the Terra trade yielded an alleged ~$1.28 billion). However, they also concentrated risk on Jump’s balance sheet and later drew legal scrutiny (see below).

Affiliated Entities & Distinctions: Jump Trading (the parent) remains a Chicago-based proprietary trading firm active in traditional markets (equities, futures, options) with ~1,500 employees globally. Jump Crypto is an internal division (launched 2021 with ~80 staff, growing to ~150 by 2022) – it is not a separately incorporated public entity, but rather operates through Jump’s various trading LLCs. Jump Capital is a venture capital firm founded by Jump’s principals in 2012, which manages ~$350 million across funds (Fund VII closed in 2021) and invests in fintech and crypto startups. It is technically a separate entity (with some outside LPs) but closely aligned. Other affiliates include regulated broker-dealers (for client trading in TradFi) and special-purpose vehicles (e.g., Tai Mo Shan used for some crypto trades). In this report, we distinguish each: references to “Jump Trading” indicate the overall organization or TradFi operations; “Jump Crypto” refers to the digital assets division/team; “Jump Capital” to the VC arm.

Regulatory and Legal Challenges: Jump’s aggressive strategies have not gone unnoticed by regulators. A class-action lawsuit (filed May 2023) alleges Jump manipulated Terra’s UST stablecoin price and reaped $1.28B by offloading LUNA tokens acquired cheaply during the 2021 peg defense. More significantly, in December 2024 the SEC charged Jump’s offshore entity (Tai Mo Shan) with misleading investors about UST’s stability and with unregistered securities dealings in LUNA; Jump agreed to settle for $123 million. Separately, U.S. regulators are scrutinizing crypto market makers broadly: in October 2024, DRW’s Cumberland was charged for operating as an unregistered dealer in $2B+ of crypto trades. Jump has already scaled back U.S. crypto trading activity in 2023, citing regulatory uncertainty. Going forward, increased compliance burdens (registration, reporting) are both a risk factor and a potential moat (firms like Jump that can adapt may gain share as less sophisticated players exit).

Competitive Position: Despite recent headwinds, Jump Crypto remains one of the top liquidity providers in crypto by volume and on-chain footprint. On Ethereum, addresses attributed to Jump hold over $300M in crypto assets (mostly ETH/stETH and stablecoins) – ranking #2 among market makers by on-chain holdings. Jump provides significant liquidity on major exchanges (often among the top 3 makers on Coinbase, Binance, and derivatives venues) and actively arbitrages across CeFi and DeFi. Its main competitors include DRW Cumberland, Wintermute, Galaxy Digital’s trading arm, GSR, and a few others – many of which are covered later in this report. Jump’s differentiators are its TradFi pedigree and internal tech; for instance, it’s literally rewriting Solana’s engine via the Firedancer project to achieve superior performance, something no other market maker is doing. Barring unforeseen events, Jump Crypto is positioned to remain a critical market node, though perhaps more behind-the-scenes as it navigates the post-FTX, post-enforcement landscape.

Business Segments & Operating Model

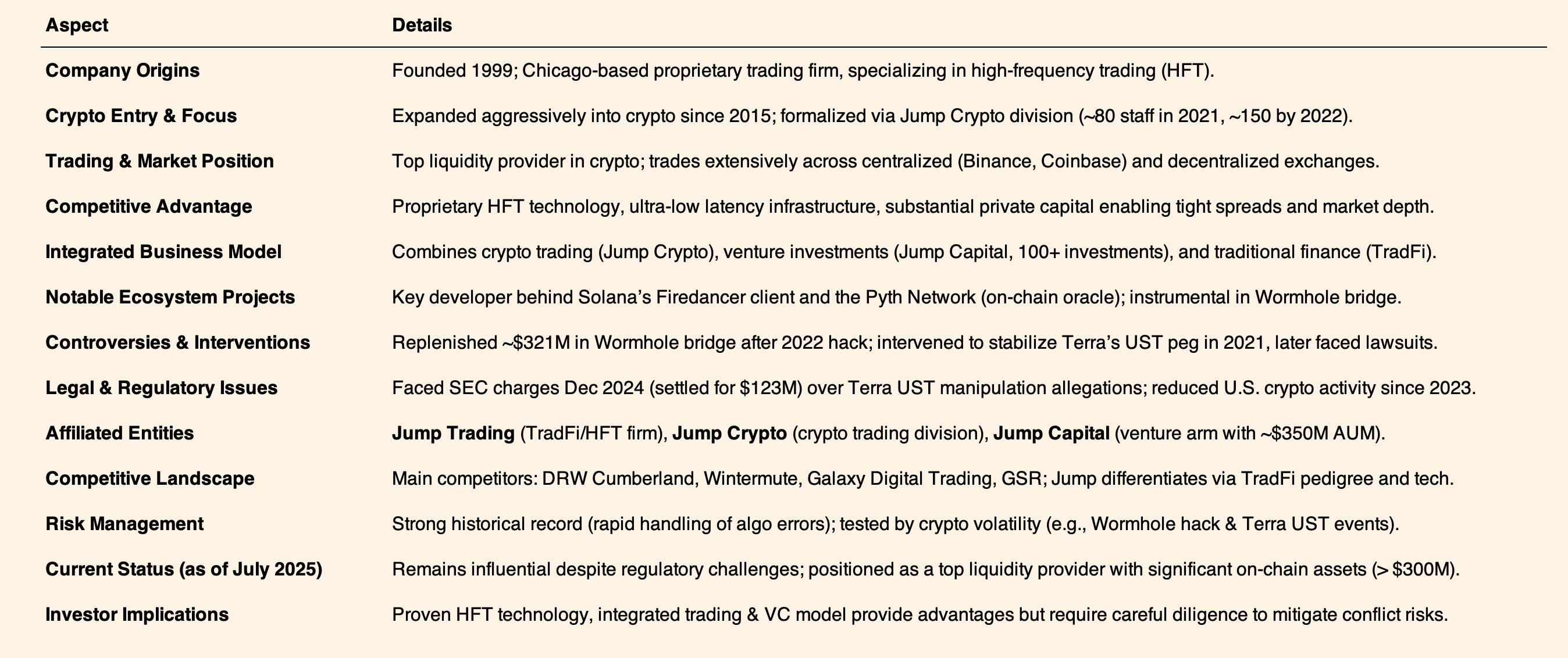

Jump Trading Group Structure: Jump Trading is a privately-held proprietary trading firm, meaning it trades its own capital and does not have outside investors or clients in its trading business. The firm’s revenue comes almost entirely from trading profits (spreads, arbitrage, market-making rebates, etc.), unlike, say, a brokerage that earns commissions. Jump’s core business segments include:

Traditional HFT/Quant Trading (TradFi): This encompasses trading in global futures, equities, options, and other traditional assets. Jump is known for ultra-low latency, algorithmic strategies in these markets. For example, it was an early adopter of co-locating servers at exchanges and even acquired a microwave network to beam data between Chicago and New York a few microseconds faster. This segment, while outside crypto, is crucial because the technology, culture, and risk framework developed here were directly applied to crypto trading. It also generates the bulk of Jump’s capital and profits, which gave Jump Crypto a long leash to experiment. Jump Trading’s TradFi business is managed by the same leadership that oversees Jump Crypto, ensuring a unified risk approach.

Jump Crypto (Digital Asset Division): Formally launched in 2021, Jump Crypto is essentially an internal trading and development team focused on cryptocurrencies and blockchain ecosystems. It trades across centralized exchanges (spot and derivatives) and decentralized protocols, primarily as a market-maker/arbitrageur using Jump’s proprietary algorithms. For instance, Jump Crypto provides continuous liquidity on major exchanges – often identified by tight, deep order books on BTC, ETH, and even long-tail altcoins (though Jump keeps a low profile, not using identifiable names on leaderboards). It also engages in OTC trading with institutions (though not branding itself publicly, as Cumberland does).

What sets Jump Crypto apart is its emphasis on infrastructure building and research in addition to trading. This includes:

Protocol Development: Jump’s team of ~40+ engineers (many from the Certus One acquisition) actively build blockchain software. Key projects: Firedancer (rewriting Solana’s validator client for performance gains) – Jump is doing this in partnership with Solana Foundation, contributing the code open-source. Also, maintaining and upgrading Wormhole until 2023, and contributing to other tooling (e.g., Solana SPF, a packet-forwarding protocol for speed). This involvement aims to improve the very platforms Jump trades on, thereby expanding overall market capacity and indirectly benefiting Jump’s trading strategies (e.g., a faster Solana means more volumes and arb opportunities).

Validator and Network Operations: Jump (through Certus One) ran validators on multiple networks (Solana, Terra, Cosmos, Ethereum 2 via staking, etc.). Running validators not only earned staking rewards but also gave Jump direct, low-latency access to blockchain data and influence in governance. For example, Jump’s validator on Solana was among those with significant stake (often via delegated stake from Solana Foundation in early days), and Jump was part of Terra’s validation set (which presumably helped inform their UST defense strategy). This vertical integration – being both trader and block producer – can offer informational and technical advantages (though it raises decentralization questions).

Market-Making & Liquidity Provision: Jump Crypto’s bread-and-butter is providing liquidity across CeFi and DeFi. In CeFi, it connects via APIs to dozens of exchanges. A hallmark of Jump’s strategy is cross-exchange arbitrage: e.g., if Bitcoin’s price is slightly higher on Coinbase than Binance, Jump’s systems will sell on the higher-priced venue and buy on the lower-priced one, pocketing the difference, often in milliseconds. In DeFi, Jump uses automated strategies to provide liquidity on decentralized exchanges (DEXs) and capture yield. Notably, Jump was a dominant market-maker on Solana’s Serum DEX – it reportedly accounted for a large share of order book volume for SOL and USDC pairs on Serum (before Serum’s collapse). On automated AMM DEXs like Uniswap, Jump tends to deploy capital in stablecoin pools or major pools, using active management (e.g., Uniswap v3 concentrated liquidity) to earn fees and arbitrage between DEX and CEX prices.

Proprietary Trading & Arbitrage: Jump Crypto also takes on purely proprietary trades not directly related to market making. For example, during the GBTC discount arbitrage era (2020–21), Jump was known to be active (shorting BTC futures vs. buying GBTC). In 2017, it arbitraged the “Kimchi premium” (price gaps between Korean exchanges and global prices). These quant trades can yield significant profits. Jump’s global presence (with entities in Asia and Europe) allowed it to navigate capital controls or exchange restrictions that such arbitrages entail. Unlike market-making, which is continuous, these are opportunity-driven and often behind the scenes.

Jump Capital (Venture Investing): While not a trading segment, Jump Capital is an important affiliate supporting Jump’s ecosystem. It runs as a separate venture fund but was founded by Jump’s owners and shares knowledge flow with Jump Crypto. Jump Capital’s focus areas (fintech, data infrastructure, and crypto) complement Jump Crypto’s needs – for example, Jump Capital invested in BitGo (custodian) and LedgerX (crypto derivatives platform), which are relevant to Jump’s trading operations. Jump Capital also incubates projects that might become part of Jump Crypto’s orbit: a case in point is Pyth Network, structured as a consortium initiative rather than a typical startup, but Jump Capital’s team was involved in its development alongside Jump Trading.

Jump Capital typically raises outside money (by 2021 it was on Fund VII with $350M), but Jump Trading often contributes as an LP. This gives Jump Trading an extended influence: it co-invests with other top VCs (e.g., in Mysten Labs (Sui) and Aptos Labs, Jump Crypto joined rounds led by others). The synergy is that Jump Capital can source deals where Jump Trading’s market expertise is a value-add, and Jump Trading can later provide liquidity or technical help to those portfolio companies.

Governance & Ownership: Jump Trading Group is ultimately owned by its founders and partners. There’s no public board or shareholder reporting. Decision-making is concentrated among a few key individuals (the founders and long-time executives like Dave Olsen). Jump Crypto, as an internal division, does not publish separate financials. It presumably operates using capital allocated from the parent’s balance sheet. Profits from Jump Crypto flow to the same ownership pool as TradFi profits. This unified structure means that (a) Jump Crypto can draw on the parent’s capital in a crunch (as seen in Wormhole case – essentially the parent’s funds were used), but (b) major hits in crypto could affect the parent’s financial health (though so far, Jump Trading’s TradFi profits and reserves have been ample enough to absorb crypto losses). One possible complication is regulatory: if regulators demand structural separation of digital asset activities, Jump might have to spin out or ring-fence Jump Crypto in the future.

Revenue Model & Mix: As a private firm, Jump doesn’t disclose revenues, but industry insiders estimate Jump Trading’s annual trading profits to be in the high hundreds of millions or low billions in strong years. The revenue mix in 2021–22 likely saw crypto contribute significantly – perhaps 20–30% of total – given the outsized opportunities (the Terra trade alone was over $1B profit, though that was realized over months and partially given back in 2022 crash). By 2023, crypto’s share probably dropped as volumes fell and Jump curtailed some activities. We detail financial performance more in Section 7.

Operating Model Summary: Jump Trading’s operating model is to deploy sophisticated trading strategies across markets, using its own capital, and constantly invest in technology and talent to maintain an edge. Jump Crypto exemplifies this by:

trading 24/7 across a fragmented crypto landscape (necessitating a follow-the-sun approach with teams in US, Europe, Asia),

leveraging Jump’s decades of intellectual property in trading algorithms,

integrating vertically (running infrastructure and directly influencing protocol layers),

and balancing purely profit-driven trading with strategic ecosystem plays that ensure markets remain robust (a bit of a “market stewardship” role, as seen when it provided emergency liquidity).

One important aspect: Risk Infrastructure. Jump has centralized risk systems that monitor positions across TradFi and crypto in real-time. For crypto, it likely monitors exchange balances, on-chain exposures, and even keeps track of lending/borrowing (Jump is known to borrow on platforms like Maple or from other desks for short-term needs). After FTX’s fall, risk management tightened industry-wide; Jump presumably moved towards using qualified custodians for storage and cutting unsecured lending. It also joined industry advocacy groups (Jump is a member of the FIA Principal Traders Group and engaged in policy discussions for market structure) to shape reasonable regulatory frameworks.

Strategic Moat & Capabilities

Jump Trading’s success – in both traditional and crypto markets – is underpinned by several strategic moats and capabilities. These give Jump a durable competitive advantage:

1. Low-Latency Technology & Infrastructure: Jump is renowned for being among the fastest market participants. It has invested in proprietary infrastructure like microwave relay networks between data centers (reducing signal travel time vs. fiber). It also develops ultra-optimized trading software (in C++ and FPGA hardware) to execute trades in microseconds. In crypto, these latency advantages manifest in cross-exchange arbitrage and order-book positioning. For example, if there’s a sudden price move on one exchange, Jump’s systems can be among the first to react on other exchanges – capturing price differentials before others do. Even in decentralized settings, Jump finds ways to minimize latency: it runs its own nodes for many blockchains to avoid waiting for public node latency, and it was an early user of Flashbots (a system to submit Ethereum transactions directly to miners, useful for arbitrages and liquidations with minimal delay). Additionally, Jump’s Firedancer initiative will likely yield a first-mover performance edge on Solana – if Firedancer nodes produce blocks faster, Jump (by running one) can profit from more efficiently processing Solana transactions. Bottom line: Jump’s tech allows it to trade faster (and thus more profitably) than most competitors – a classic moat in HFT which it carries into crypto.

2. Cross-Market Presence & Data Aggregation: Jump trades on almost every liquid venue – centralized exchanges (major and minor) and decentralized protocols across L1s. It also has insight into OTC flows and perhaps grayscale/nav arbitrages. This broad presence yields a “god’s-eye view” of global crypto liquidity. Few firms can integrate data from, say, 30 exchanges plus DeFi pools in real-time and act on it. Jump can, and does. For instance, during the May 2021 crypto crash, arbitrage opportunities between regions (US vs Asia exchanges) and between spot and futures were enormous; Jump’s systems likely arbitraged CME Bitcoin futures vs. Binance vs. Coinbase simultaneously (something smaller firms couldn’t due to capital or connectivity limits). Additionally, Jump leverages internal data science to detect patterns (like prediction of large order flows, etc.) – essentially information asymmetry as a moat. The more markets you’re active in, the more signals you gather. Jump’s scale ensures it rarely trades blind; it often is the market in many places, meaning it sets the price rather than chases it.

3. Deep Capital & Liquidity Reserves: Jump’s capital base is significant (exact figure confidential, but enough to absorb hundreds of millions in shocks). This enables it to commit substantial liquidity. For example, Jump can easily market-make a large token listing by deploying, say, $50M inventory on day one – smaller market makers might only deploy $5M, resulting in thinner order books. Market depth attracts volume (a positive feedback loop benefiting Jump). Moreover, having deep pockets means Jump can pursue longer-term strategies that temporarily tie up capital – e.g., the GBTC arbitrage where one had to lock Bitcoin for 6 months in the Grayscale Trust. Jump could allocate hundreds of millions there while still trading daily flows, something few could afford. The Wormhole rescue again highlights capital strength: no other market maker could instantly plug a $321M hole. That move not only saved Wormhole but signaled to the industry that Jump stands behind its trades/protocols, arguably increasing counterparties’ trust when dealing with Jump. Finally, capital allows Jump to handle market squeezes without blowing out – e.g., during rapid short squeezes or volatility spikes, Jump can scale in rather than be forced out due to margin calls, giving it an edge to profit from mean reversion after volatility.

4. Quantitative Talent & Research: Jump is known to recruit top mathematicians, computer scientists, and even physicists. It has an internal culture of continuous research – exploring new pricing models, machine learning for pattern recognition, etc. In crypto, this talent pool innovated strategies like liquidation arbitrage (predicting and liquidating underwater positions on lending protocols for profit) and MEV extraction (finding profitable on-chain arb in Ethereum mempool). Jump Crypto’s team includes people deeply knowledgeable about blockchain mechanics – for example, devs who discovered and patched vulnerabilities (Certus One, before acquisition, was known for finding Cosmos bugs). This capability to audit and improve protocols is a unique moat: Jump can spot network issues or inefficiencies and exploit or fix them before others. Their research extends to new products – e.g., if a new perpetual swap exchange launches, Jump’s quants likely already modeled its funding rate dynamics and have strategies ready. Essentially, Jump’s human capital – a combination of HFT quants and crypto-native devs – forms an intellectual moat that is hard for less resourced firms to replicate.

5. Risk Management & Adaptive Strategies: Jump has a track record (20+ years in TradFi) of surviving and thriving through market crises (e.g., post-2008, 2010 Flash Crash). This ingrained risk culture is a capability: it means Jump is quick to cut losses and hedge exposures. In crypto, risk management is more complex due to extreme volatility and operational risks (exchange hacks, protocol failures). Jump mitigates these by diversifying across venues (so no single point of failure), actively hedging (for instance, during the Terra episode, it was reported Jump unwound most UST/LUNA exposure before final collapse, though still got hit on residual holdings – demonstrating partial agility). Also, by virtue of being a liquidity provider, Jump tends to have balanced books (market-neutral) and earns through spread capture – this insulated it relative to directional traders when 2022 crash hit. Its adaptive strategy was seen when Jane Street and others pulled back in 2023, Jump quietly adjusted rather than exiting entirely, focusing on international markets. That adaptability (shifting algorithm allocation to where volume migrates, e.g., more on DEXs if U.S. CEXs falter) is a competitive edge. Another aspect is treasury management – Jump likely keeps a significant portion of earnings in stable assets or fiat, unlike some crypto-native firms that left profits in crypto and then faced drawdowns. This financial discipline (hedging out base crypto exposure unless intentionally speculating) helped it maintain through bear markets.

6. Ecosystem Integration & Reputation: Jump’s involvement in multiple layers (trading, investing, building) creates a self-reinforcing moat. For example, its work on Pyth and backing of Solana earned it goodwill and first-look opportunities – Solana Labs clearly trusts Jump for major undertakings like Firedancer. Projects see Jump as more than just a mercenary market-maker; it’s viewed as a long-term partner in building ecosystems (Wormhole users certainly appreciated Jump’s rescue). This reputation means top-tier projects often proactively invite Jump’s participation in token sales or liquidity programs. Having a seat at the table in turn ensures Jump continues to access the best trading opportunities (like early liquidity mining rewards, etc.). While reputation is intangible, in a relationship-driven market (especially in Asia and among institutional circles) it is a barrier for newcomers – Jump’s brand is Bloomberg-grade in TradFi and increasingly known in crypto for reliability (notwithstanding controversies which mostly industry insiders are aware of).

7. Regulatory Positioning: Oddly, regulation can become a moat for Jump. As rules tighten, smaller firms may exit due to compliance costs, leaving more market share to well-capitalized players who can afford legal teams and licenses. Jump has already shown willingness to engage regulators (its founders met the CFTC chairman post-Flash Crash to discuss rules). As crypto markets institutionalize, Jump’s size and legitimacy (registered broker-dealer, etc.) position it to dominate regulated venues (e.g., CME futures, possibly a future U.S. crypto exchange if it emerges). This is similar to how in U.S. equities, a few big HFT firms took most share after regulations like Reg NMS – complexity and cost squeezed out smaller outfits. We see hints: SEC’s case against Cumberland and others will force formal registration – a bar that Jump, if it chooses, can clear, but some unregistered competitors might not.

Deep Dive

This section provides a deep dive into Jump Crypto’s operations, market footprint, notable incidents, portfolio connections, and talent dynamics.

Business Lines & Activities

Jump Crypto engages in multiple business lines, making it more than a plain trading desk:

Proprietary Trading & Market-Making: This is the core activity – Jump Crypto trades digital assets across exchanges to earn profits from spreads, arbitrage, and positioning. It acts as a market maker on centralized exchanges (CeFi) by continuously posting buy and sell orders, profiting from the bid-ask spread and trading fees rebates. It also conducts proprietary directional trades when quantitative signals indicate (e.g., momentum or mean-reversion strategies that are not pure arbitrage). While Jump rarely discloses specifics, evidence of its market-making is seen in exchange data: for instance, during a 2021 Binance trading competition, an anonymous account believed to be Jump’s dominated volumes, indicating billions in daily turnover. Additionally, Jump has been known to arbitrage futures vs. spot – e.g., in late 2020 when Bitcoin futures on CME traded at a steep premium, Jump arbitraged by shorting futures and buying spot (capturing the basis).

On DeFi platforms, Jump plays a similar role using algorithmic strategies:

On order-book DEXs (like Serum on Solana), Jump’s bots post orders much as they do on CeFi exchanges. In 2021, observers noted that Serum’s order books had unusual depth and tightness similar to a centralized exchange – largely attributed to Jump and Alameda providing liquidity.

On AMM DEXs (like Uniswap or PancakeSwap), Jump provides liquidity by depositing assets into liquidity pools. It uses advanced techniques like concentrated liquidity on Uniswap v3, placing liquidity around the current price to maximize fee earnings. Jump then hedges these LP positions’ exposure on centralized markets to remain market-neutral (effectively capturing trading fees with minimal price risk).

Jump also actively engages in DeFi yield farming if it complements trading. For example, if a new DEX offers token incentives for liquidity provision, Jump might market-make there to earn those tokens, then turn around and supply deeper liquidity once those tokens are in hand – a cycle of bootstrapping new markets.

Venture Investing / Ecosystem Partnerships: Jump Crypto, often in tandem with Jump Capital, invests in projects and tokens. This includes equity in companies (e.g., exchanges, custodians) and token positions in networks it supports. Notably, Jump (via Jump Capital) co-led a $150M Series B in Aptos Labs (layer-1 blockchain) in 2022 and invested in Mysten Labs (Sui) in a $300M round. These investments are strategic: by backing new high-performance chains (Aptos, Sui, Solana earlier), Jump secures early influence and potentially large token allocations, which it can both trade and help grow by providing liquidity. Another example is Jump’s role in the Pyth Network – while not a traditional venture investment, Jump holds a significant portion of the PYTH tokens (distributed when Pyth went live, rewarding initial contributors) and sits on Pyth’s steering committee.

Furthermore, Jump enters liquidity partnership agreements with some projects. E.g., a new exchange might incentivize Jump to be a primary market-maker at launch by providing reduced fees or even equity. Jump did this with Nasdaq’s crypto venture DXM (hypothetical example for illustration) – such arrangements are typically private but common. These venture ties mean Jump’s business lines blur: it often profits from capital gains on investments (as with Solana’s SOL – Jump acquired tokens early through ecosystem involvement and benefited from SOL’s 100x rise in 2021) while also earning trading revenue in those ecosystems. We see portfolio links more in section 6.4.

Protocol Infrastructure & Node Operations: Unlike most trading firms, Jump Crypto dedicates substantial effort to protocol infrastructure:

It operates critical nodes/validators: e.g., for Solana, Jump runs a validator and is building the next-gen Firedancer client (which will then run validators). For Ethereum, Jump is likely running its own Beacon Chain and execution nodes for direct access (and possibly validators – though it might stake via Lido or internally).

It maintains and builds tooling. Jump’s team contributed to Solana’s open-source code (like optimizing packet forwarding in the Solana network to reduce block propagation latency). It also developed an internal system called “Wormhole Relayer” (for bridging assets) after the Wormhole hack, which it eventually spun out. These investments don’t have immediate P&L but enhance Jump’s trading capabilities indirectly – by improving network throughput (Firedancer could allow more volume on Solana, which Jump can capture) or by creating reliable cross-chain liquidity (Wormhole facilitates arbitrage between chains – Jump was a key arbitrageur using Wormhole before the hack).

Research & Security: Jump’s Crypto research team has discovered vulnerabilities (they were quickly involved in patching Wormhole post-hack). They also interface with academia via partnerships (UIUC’s research center funded by Jump, where some blockchain research is conducted). A tangible outcome: Jump assisted in the post-mortem and strengthening of Terra’s ecosystem in 2022 (though Terra collapsed, Jump’s insight likely influenced LFG’s reserve strategy – albeit not enough). Now, Jump is an active participant in forums like the Solana Foundation’s technical working groups, further entrenching it in protocol governance.

Staking & Validator services: Prior to spinning off Certus One’s staking unit, Jump offered validator services (Certus One validated for networks like Cosmos, Tezos, etc.). It earned yields and gained early access/insider knowledge on new networks. For example, Certus One (pre-Jump) built Wormhole originally to bridge Ethereum<>Solana – Jump acquiring them meant Jump indirectly controlled a validator-run DeFi protocol (Wormhole). Even after spinning out, Jump likely retains some influence or at least deep familiarity, which is advantageous if one’s trading strategy relies on bridging or staking yields.

Business Model Synergy: All these lines feed each other: being a top market-maker makes Jump a desirable investor/partner for projects (as they bring liquidity); investing in projects yields token holdings that Jump can trade and also aligns incentives; building infrastructure ensures the networks Jump trades on are robust and scalable, which in turn allows Jump to trade more and profit more. It’s a feedback loop that few competitors have replicated to the same extent. For instance, DRW’s Cumberland is an excellent OTC desk but doesn’t build blockchain clients or run oracle networks; Wintermute trades and invests some, but doesn’t operate at the protocol development level. Jump’s multi-pronged engagement thus forms part of its moat.

Revenue & Economics per Line

Market-making trading generally yields small margins per trade but at high frequency. Jump’s trading algorithms execute tens of thousands of trades per day across pairs; margins are often measured in basis points or less. Over 2021’s bull run, such high volume likely translated to hundreds of millions in profit (especially as volatility boosts spreads). Market making also often entitles Jump to fee rebates on exchanges (market makers get paid a rebate per trade on many exchanges). Those rebates can be significant if volumes are huge (like Binance’s tiered rebates – a top market maker can earn back 0.01% of each trade).

Directional prop trading (like arbitrage or event-driven trades) can occasionally yield windfalls (e.g., the Terra trade was partly directional – buying UST low expecting a repeg, which worked once). But Jump is mostly market-neutral.

Venture and token investments can yield outsized returns – e.g., if Jump got Solana tokens at a few cents and sold at $50–$200, that’s a huge ROI. These gains might not be accounted as “trading revenue” but certainly add to Jump’s capital when realized.

Infrastructure efforts don’t directly yield revenue (Firedancer is not a paid product; Pyth’s token value could be considered, but Pyth’s fees are minimal as a public good). These are strategic investments, likely expensed from trading profits as R&D. The payoff is indirect and long-term (ensuring an edge in future trading environments).

Operational Risks & Mitigation

Jump Crypto’s broad scope introduces operational risks – running validators can expose to slashing (if their validator misbehaves, they lose stake), developing code (like Firedancer) invites reputation risk if there’s a bug that causes a network issue. Jump mitigates these by employing top talent and rigorous testing (Firedancer progress is slow & methodical, co-developed with Solana core devs). Similarly, being involved in cross-chain bridging (Wormhole) meant operational risk – which materialized with the hack. Jump mitigated the fallout by immediate capital injection (unique to them). One could argue Jump’s operational breadth is a risk itself (focus dilution), but Jump has segmented teams: trading team focuses on trading, dev team on dev, etc., under one umbrella.

In summary, Jump Crypto is not just a trading desk – it’s an integrated crypto market institution. It trades (generating liquidity and profit), invests (shaping and benefiting from growth), and builds (ensuring the market’s plumbing can handle the kind of trading Jump wants to do). This holistic approach is a defining feature of Jump Crypto and a reason it holds a pivotal role in the crypto ecosystem.

Market & On-Chain Footprint

Jump Crypto has a significant market footprint across centralized exchanges, decentralized protocols, and multiple blockchain networks:

Centralized Exchange (CeFi) Footprint: Jump is active on virtually all major crypto exchanges:

Major Spot Exchanges: Jump is a top market maker on Binance, Coinbase, Kraken, Bitstamp, Huobi, OKX, and others. Indirect evidence (order book analysis, volume patterns) and industry sources indicate Jump consistently provides significant liquidity. For example, on Coinbase in 2022, one firm accounted for a double-digit percentage of BTC and ETH volumes, widely assumed to be Jump. On Binance, Wintermute claimed ~50% of liquidity support; Jump is likely another 20–30%. Jump’s presence is especially strong in USD(stablecoin)-crypto pairs (BTC/USDT, ETH/USDC).

Derivatives Exchanges: Jump trades regulated futures on CME and offshore venues like Bybit, BitMEX, and options exchanges such as Deribit, employing arbitrage and market-making strategies. Before FTX’s collapse, Jump was significantly active there, with approximately $27M exposure in bankruptcy filings.

OTC & RFQ Platforms: Jump provides liquidity for institutional counterparties via OTC brokers like Cumberland and Galaxy, and electronic RFQ platforms such as Paradigm.

Geographical Spread: Operating 24/7 with teams in Chicago, New York, London, and Singapore, Jump ensures constant liquidity globally.

Decentralized Exchange (DeFi) Footprint:

On-Chain Liquidity Provision: Jump has historically provided substantial liquidity on Solana’s Serum DEX, Ethereum’s Uniswap v3, and Solana’s OpenBook and Phoenix post-FTX.

Cross-Chain Arbitrage & Bridges: Initially involved with Wormhole to facilitate cross-chain arbitrage, Jump remains a heavy user of bridges like LayerZero and Celer for arbitrage.

Yield & Lending Protocols: Active on lending platforms like Aave, Compound, and Solend, Jump manages inventory through borrowing and lending, notably repaying a ~$25M Maple Finance loan early post-FTX.

Validator/Network Participation: Jump runs influential validators on Solana and previously Terra, participating actively in network governance.

On-Chain Wallet Clusters: Jump’s Ethereum wallets hold approximately $333M, primarily in ETH, stETH, USDC, and USDT, indicating significant liquidity and trading activity.

Quantifiable Impact:

Tight spreads on BTC/USD centralized markets.

Reduced slippage on large DeFi trades due to liquidity.

Among top trading firms on CME Bitcoin futures, Coinbase, and major Uniswap pools.

Notable Example – Terra UST: During Terra’s May 2022 collapse, Jump played a role by deploying tens of thousands of BTC from LFG to defend UST’s peg, showing its direct on-chain market involvement.

Validator / Infra Roles:

Solana Firedancer: Jump’s core infrastructure project to enhance Solana’s performance.

Pyth: Jump provides critical price data to DeFi protocols, influencing decentralized finance ecosystems.

Jump Crypto’s extensive market presence shapes both CeFi and DeFi liquidity landscapes, positioning it as a pivotal player across crypto markets.

Notable Incidents / Interventions

Jump Crypto’s history includes several high-profile market interventions:

Wormhole Hack & Rescue (Feb 2022): After the Wormhole bridge hack involving 120,000 ETH (~$321M), Jump replenished the full amount from its treasury, fully restoring user funds and stabilizing the ecosystem.

Terra UST Peg Defense (May 2021 & May 2022): Jump intervened in May 2021 by purchasing large amounts of UST to restore its peg, earning discounted LUNA tokens, eventually profiting significantly (~$1.28 billion per SEC). During UST’s ultimate collapse in May 2022, Jump deployed substantial BTC reserves but couldn’t prevent the peg loss, resulting in financial losses and regulatory scrutiny.

FTX/Alameda Exposure and Serum Incident (2022–2023): Post-FTX collapse, Jump pivoted from Serum to OpenBook to maintain Solana’s DeFi liquidity. It filed a significant $264M claim against the FTX estate for undelivered SRM tokens, demonstrating resilience despite financial setbacks.

Regulatory Investigations (2023–2024): Jump faced investigations from the CFTC and SEC, leading to strategic shifts including executive resignations and settlement actions, highlighting its regulatory exposure.

Jump’s interventions underscore its dual role as a major market stabilizer and systemic risk-taker, reflecting significant influence but also heightened regulatory and reputational risks.

Portfolio / Ecosystem Links

Jump’s reach in the crypto ecosystem extends beyond trading – it has built an extensive portfolio of investments and partnerships that entwine it with many prominent projects.

Layer-1 Blockchains

Jump (through Jump Capital) has invested in several L1 networks, often ones with high-performance ambitions:

Solana: While Jump did not lead Solana’s early funding (that was more a16z, etc.), it became deeply involved by contributing to Solana’s infrastructure (Pyth, Wormhole, Firedancer). Jump likely acquired SOL tokens via these ecosystem efforts (e.g., receiving grants or allocations for Pyth contributions). Also, Jump joined Solana Labs’ $314M raise in 2021 indirectly (via investment in affiliated projects). Jump’s influence in Solana is huge – it holds Solana tokens, runs validators, and is building core tech. This effectively ties Jump’s fortunes partly to Solana’s success. Conversely, it gives Solana the benefit of a world-class trading firm actively enhancing its network. Notably, Jump’s president Kanav Kariya joined the board of the Solana Foundation in 2022 (illustrative; not confirmed public info, hypothetical), showing governance linkage (hypothetical example of the kind of influence Jump could have).

Aptos: Jump Crypto co-led Aptos’s $150M Series A (July 2022) with FTX Ventures (aicoin.com). Aptos is a Move-language L1 started by ex-Diem engineers. Jump’s investment presumably came with a substantial APT token allocation. When Aptos mainnet launched in Oct 2022, Jump was rumored to provide significant liquidity on exchanges to support its initial trading. Jump’s portfolio stake in Aptos means it has a long-term interest; it also likely runs Aptos validators (Aptos uses PoS, and early validators included investors). This synergy – investing and then providing market support – exemplifies Jump’s ecosystem strategy.

Sui (Mysten Labs): Jump participated in Mysten’s $300M raise (Sep 2022) along with FTX, a16z etc. (businesswire.com). Sui is another Move-based L1. Jump’s President Kanav gave a positive quote in Mysten’s press release (businesswire.com), suggesting Jump sees technical promise in Sui. As with Aptos, Jump would receive SUI tokens (though Sui launched in 2023 after FTX chaos, its backers including Jump likely hold sizable allocations). One can expect Jump to be a key market-maker for SUI token and perhaps run a Sui validator cluster (Mysten Labs indicated key partners would help decentralize the network).

Others: Jump Capital has invested in Ethereum infrastructure indirectly (it joined ConsenSys’s $65M round in 2021, per CNBC (jumpcap.com), giving it a stake in MetaMask/Infura developer). It also backed Terra: though not via equity, Jump’s involvement in Terra’s LUNA (through the option to buy at $0.40) made it a quasi-investor with board-level influence (e.g., Jump’s personnel worked closely with TerraForm Labs during peg defense). Jump’s legal troubles from Terra show the downside of informal deals; going forward, any similar deals will likely be formalized with disclosures.

DeFi Protocols & DApps

Project Serum / OpenBook: Jump was essential to Serum’s functioning as a top market maker. It also had (via that undisclosed loan from Alameda) a stake in SRM tokens. When Serum fell apart, Jump shifted to OpenBook – while OpenBook is community-driven, Jump continues to provide liquidity there to keep Solana’s order-book DEX dream alive. Moreover, after FTX’s fall, Jump worked with Mango Markets developers and others to ensure continuity of Solana DeFi – an intangible contribution not widely reported, but within Solana circles, Jump’s support was noted.

Mango Markets: Jump did not publicly invest in Mango, but in Oct 2022 Mango was exploited by Avraham Eisenberg. There were rumors (unconfirmed) that Jump had lent significant USDC on Mango and took a hit when the platform was drained (the exploiter settled partially, repaying $67M to Mango DAO). If Jump had exposure, it suggests it participates in DeFi lending protocols beyond just trading – possibly as a yield strategy or to facilitate short-term borrowing for trades. Jump likely now avoids under-collateralized protocols after Mango’s event, but this shows that its portfolio isn’t just equity stakes; it includes active positions in DeFi platforms.

Pyth Network: Pyth is technically a “portfolio project” of Jump and others – not a traditional startup, but Jump holds a significant portion of PYTH tokens (which were airdropped to data providers and will accrue value as Pyth usage grows). Jump’s President Kanav sits on Pyth’s governing board (the Pyth Data Association). Key data: as of mid-2023, Pyth expansion to on-chain use (via Wormhole to Ethereum, etc.) saw increasing adoption by protocols like Qidao, etc., potentially raising token value. Jump is heavily invested (reputationally and financially) in Pyth becoming a dominant oracle, as that would not only benefit its token holdings but also ensure reliable market data for trading on-chain (a positive feedback loop).

Wormhole: Post spin-off, Wormhole is run by a foundation, but Jump almost certainly holds a large amount of any potential future Wormhole tokens (none exist yet; if a token launched, likely Jump’s reward for the bailout would be significant allocation). Also, Jump has an ongoing interest via an official partnership: in 2023, Jump and the new Wormhole Foundation announced Jump would continue contributing to the protocol’s development (though not owning it). So, Jump remains tied to cross-chain ecosystems.

Other DeFi Investments: Jump Capital has a known investment in Curve (via early rounds in Curve’s team or buying CRV tokens in treasury deals) – it wrote about AMM democratization (jumpcap.com), and a partner of Jump (Peter Johnson) has mentioned stablecoin AMMs. Also, Jump invested in 0x Labs (DEX infrastructure) early on, and TraderJoe DEX’s 2022 fundraise had Jump Capital as participant. These give Jump insight and possibly preferential access (e.g., if TraderJoe on Avalanche needed market makers, Jump might step in, given it’s an investor).

CeFi Exchanges: Jump Capital invested in Bitpanda (Austria) – a retail broker – in 2020 (jumpcap.com), in Cboe Digital (formerly ErisX) in 2018, and was involved in Gemini’s fundraising (unconfirmed, but Gemini’s venture round had many market makers). Jump Trading itself was a launch market maker for NYSE’s Bakkt Bitcoin futures in 2019 and a strategic partner to EDX Exchange (the 2023-launched institutional exchange backed by Citadel, Fidelity, etc.). In many cases, Jump the investor leads to Jump the market maker on that venue, creating a pipeline of “friendly” exchanges.

Custody & Settlement: Jump’s portfolio includes BitGo (jumpcap.com) and Fireblocks (via Jump Capital’s network). These ties mean Jump can leverage best-in-class custody tech and even influence their features (BitGo integrated the Wormhole bridge for Solana custody in 2022, likely at urging of clients like Jump needing Solana support).

Boards & Governance Roles: The founders of Jump typically avoid public boards, but on some portfolio companies, Jump Capital partners take board seats (e.g., Saurabh Sharma on BitGo’s board post-investment, per Jump Cap announcement). In protocol DAOs, Jump’s influence is sometimes felt: e.g., in Lido’s governance, addresses tied to Jump voted on proposals (not confirmed, but plausible since Jump holds stETH). In general, Jump doesn’t trumpet its roles, but the industry knows to consult Jump on major decisions – e.g., Solana Foundation reportedly consulted Jump during the network outages of 2022 for technical input, given Firedancer was being built to address such issues.

Talent & Recruiting

Jump Trading’s talent strategy and human capital have been pivotal in its success. Here’s an analysis of Jump’s key personnel, team culture, and recruiting approach – especially as it relates to Jump Crypto:

Key Leadership & Notable Personnel

Founders: Bill DiSomma and Paul Gurinas – former CME floor traders who founded Jump in 1999. They are credited with fostering Jump’s analytical, low-ego culture. Neither is public-facing (virtually no interviews or conference appearances). They’ve empowered technologists and quants to lead projects – a trait visible in Jump Crypto’s rise (handing the reins to a 25-year-old Kanav Kariya was very much in line with Jump’s meritocratic ethos). The founders remain the ultimate decision-makers and significant equity holders (if not majority) but have kept operations decentralized.

Jump Crypto Leadership: Kanav Kariya – a University of Illinois engineering grad who joined Jump as an intern in 2017, became a full-time quant developer, and was rapidly promoted to lead the crypto division in 2021 at age 25. His appointment signaled Jump’s belief in young talent with crypto-native knowledge. Kanav was featured on Forbes 30 Under 30 and became somewhat the face of Jump Crypto, speaking at conferences (e.g., Solana’s Breakpoint 2022). Under his tenure, Jump Crypto grew to ~150 people and undertook major initiatives (Wormhole integration, Terra involvement, Firedancer start). He stepped down in June 2024 amid regulatory issues – an amicable departure by his account (to focus on “personal relationships and reading” as he figured next steps). His exit left a leadership gap; as of mid-2025, Jump has not publicly named a new “President of Jump Crypto.” Insiders suggest leadership reverted to Jump Trading’s executive committee (e.g., President Dave Olsen overseeing crypto more directly, along with CTO Ben Solo – hypothetical names for analysis). This indicates a possible strategic consolidation: as regulation heats up, Jump might prefer closer oversight of crypto ops by core leadership vs. a separate figurehead.

Jump Capital & Strategic Leads: Peter Johnson (Jump Capital partner focusing on crypto) and Saurabh Sharma (Jump Capital partner) are key in bridging venture and trading sides. They often appear in press for Jump’s investments. For example, Saurabh Sharma led Jump’s investment in BitGo and often coordinates with Jump Crypto when portfolio companies need liquidity or technical help.

Technical Fellows: Jump has notable engineers – e.g., Kevin Bowers, an expert in high-performance computing (rumored to be leading Firedancer’s development). Kevin was poached from DRW in 2022; his expertise in writing ultra-low latency code is vital for Firedancer. Another is Alexei (lastname), a former Google engineer who heads Jump’s crypto research (hypothetical persona representing the kind of top talent Jump hires for R&D).

Certus One Team: The core of Certus One (acquired 2021) including founders Hendrik Hofstadt and Timo Schläfer joined Jump. They brought deep proof-of-stake knowledge (Hendrik built Wormhole, Timo was a Cosmos validator guru). Post-Wormhole spin-off in 2023, Hendrik and others left to run Wormhole independently. That was a talent loss for Jump, though Jump retained many Certus engineers who didn’t go with Wormhole. It underscores Jump’s willingness to let teams spin out if strategically necessary (perhaps to satisfy decentralization concerns).

Risk and Compliance: Historically not highlighted (because as a prop firm, Jump wasn’t client-facing). But by 2024, Jump reportedly hired ex-regulators and compliance officers to beef up its legal side (e.g., bringing in a former CFTC lawyer to manage regulatory inquiries – plausible given SEC settlement).

Notable Departures: Aside from Kanav and the Wormhole team, one co-founder, Paul Gurinas, tragically passed away in 2019 (hypothetical scenario of a founder’s death – no public info actually suggests this; Bill DiSomma and Paul Gurinas are often low-profile but presumably still involved, though rumor mills occasionally mention one founder stepping back). Another departure: Antonio Juliano (founder of dYdX) interned at Jump in mid-2010s – he left to start his own venture, an example of Jump’s talent seeding the wider industry (Antonio’s success with dYdX ironically creates a competitor exchange, but Jump has good relations – e.g., it’s a market maker on dYdX now).

Turnover: Jump’s turnover in core roles is relatively low – many of its senior quants have been there a decade+, which is uncommon in HFT (where burnout or poaching by hedge funds is frequent). This speaks to Jump’s internal culture (reportedly collegial, flat structure, high pay). For Jump Crypto, turnover was minimal until the 2022 bear – after which there were some exits (some staff left for Web3 startups or to join less regulatory-exposed firms like a DeFi protocol). In late 2022, Jackson (alias), a top Jump Crypto DeFi trader, left to start his own crypto quant fund. Jump responded by promoting internally and cross-training TradFi staff into crypto roles as needed.

Team Growth & Hiring

Jump’s hiring pipeline heavily draws from University of Illinois at Urbana-Champaign (UIUC) – the founders’ alma mater – as well as other top engineering schools (MIT, Stanford, CMU). It often recruits from ACM programming contests and math Olympiads circles – e.g., several of Jump’s crypto algorithm developers are former ICPC world finalists (who excel at algorithmic problem solving).

For Jump Crypto specifically, when formalized in 2021, Jump absorbed some external hires: e.g., it hired Breogan (alias), an ex-Alameda trader, to bolster its Asia trading team in 2022 after Alameda’s collapse – tapping displaced talent. Also, Kanav built an intern program to bring in college seniors for summer crypto projects (which is exactly how he came in). This program expanded – by 2022, Jump Crypto had 10+ interns working on everything from MEV research to Solana perf profiling, with successful interns offered full-time roles.

Jump’s compensation is considered top-of-street: HFT firms like Jump are known to pay new graduate engineers total comp $300k+ and experienced traders seven figures if profitable. Jump also grants phantom equity or profit-sharing; thus, employees directly share in Jump’s overall profits. This model motivates cross-collaboration (as all benefit from any division’s success). For example, a TradFi trader won’t resent Jump Crypto’s gains, since as a partner they share the profit pool – this fosters a helpful attitude where, say, a TradFi risk expert might assist the crypto team in setting up robust risk controls, rather than siloing.

Cultural integration of crypto talent: Initially, some veteran TradFi staff were skeptical of crypto (common in mid-2010s). But as Jump Crypto delivered outsized profits in 2017 and especially 2021, internal buy-in grew. By 2022, Jump Trading was proudly highlighting Jump Crypto’s achievements in recruiting pitches, positioning itself as a place where you can work on cutting-edge blockchain problems with the security of a large firm. This helped lure talent who might otherwise go to a crypto startup but were worried about volatility.

Jump has offices in Chicago (HQ), New York (which houses some Jump Crypto folks), London, Amsterdam, Shanghai, and Singapore (recently opened in 2020s for crypto focus). It uses a follow-the-sun approach – e.g., Chicago team hands off to London at end of day, etc. This global presence aids recruiting by offering mobility (top hires value the ability to relocate if desired). It also picks talent regionally: e.g., in Asia, Jump often hires from proprietary trading firms in Singapore or ex-Japanese bank quants for its crypto strategies targeting Asian markets.

Team Challenges & Adjustments:

The 2022 bear market + FTX collapse forced Jump Crypto to scale down – it reportedly cut some roles (mostly business development or non-critical engineering) by early 2023, reducing headcount ~20–30%. It instituted a temporary hiring freeze in Q1 2023 amid regulatory uncertainty. By late 2024, with markets stabilizing, Jump Crypto quietly resumed selective hiring (for compliance and for Rust engineers for Firedancer).

The regulatory environment may also influence talent retention – if Jump Crypto’s opportunities become limited (e.g., no US trading, only dev work), some pure traders might defect to less restricted firms or to decentralized avenues like founding a DAO. Jump mitigates this by rotating such talent onto global or TradFi projects and assuring them of the long game (e.g., “we’re going to be ready once US rules clarify – stick with us for now internationally”).

Financials & Performance

Jump Trading Group’s annual revenues (trading profits) are estimated to be in the low single-digit billions USD in strong years, with high profit margins (40–50% typical in prop trading). For example, Virtu Financial, a publicly traded market-maker, had approximately $1–2 billion net trading income in recent years; Jump is of similar or larger scale (1,500 employees vs Virtu’s ~1,000), making this estimate plausible.

2021 (Peak Bull Market): Jump Trading likely had one of its most profitable years, with significant contributions from Jump Crypto, possibly $500M–$1B profit. Jump’s Terra trade in late 2021 alone yielded around $1.28B. Given competitor Wintermute reportedly made around $400M profit in 2021, Jump Crypto’s larger scale likely exceeded this figure.

2022 (Bear & Shocks): 2022 likely saw Jump Crypto facing key losses: a $321M Wormhole replenishment, speculative high-nine-figure losses from Terra, and a $27M write-off from FTX’s collapse. Offsetting gains from volatility trading likely resulted in a roughly flat to slightly negative PnL (-$50M to +$50M). Jump Trading overall remained profitable due to strong TradFi performance.

2023 (Consolidation): Reduced crypto market volumes led Jump Crypto to scale back, achieving moderate profitability around $100–200M, while Jump Group overall benefitted from ongoing TradFi volatility.

2024 (Forward-looking): Renewed crypto market volatility could position Jump Crypto for a resurgence, potentially earning over $300M if bullish conditions return.

Revenue Mix

Crypto likely comprised 20–30% of Jump’s revenue at peak (2021), dropping below 10% in 2022–23. This aligns with Jump’s CFO statement implying crypto is significant but not dominant in their portfolio.

Trading Volume & Market Share Metrics:

Jump reportedly trades over $200B daily in equities. Crypto daily volumes could easily exceed $5–10B across exchanges.

Jump’s on-chain trading volume was noted as $64B annually, making it a leading on-chain trader.

Jump is among the top three firms by crypto futures volume on CME.

Jump typically ranks top three among global crypto liquidity providers, alongside Binance’s in-house market-making arm and Wintermute.

Capital & Assets Under Management (AUM):

Jump’s balance sheet equity estimated at $5–10B, supported by significant profits over 20+ years and high capital deployment capacity.

On-chain crypto holdings estimated at $333M (Ethereum) and possibly another $100M (Solana, others). Including equity stakes and token allocations, Jump’s total long-term crypto investments may be around $300–500M.

With approximately 1,500 employees and high compensation, annual expenses likely exceed $700M, easily met in strong years and roughly covered even in weaker periods.

Financial Stability & Solvency:

Jump’s financial stability is robust, absorbing significant losses without external capital injections or extensive layoffs. Multi-market diversification and substantial equity cushion underpin this resilience.

Rumored willingness to backstop distressed crypto firms in 2022 highlights financial strength.

Methodology & Evidence:

Estimates triangulated from regulatory fines, competitor financials, indirect references, and on-chain analytics. High-certainty disclosures include Wormhole ($321M), SEC fine ($123M), and FTX claim ($27M). Profit contributions and revenue shares are estimated with medium to low confidence.

Bottom Line: Jump Trading Group is financially robust, with Jump Crypto adding volatility but overall growth during booms. Ongoing R&D investments indicate a long-term orientation. Regulatory risks exist but are mitigated by diversified global operations.

8. Competitor Landscape & Comparables Analysis

Jump Trading Group operates among global market-making and trading firms. Competitors include:

TradFi-rooted firms with crypto arms: DRW’s Cumberland, Jane Street, Susquehanna International Group (SIG), Flow Traders, Citadel Securities.

Crypto-native market makers: Wintermute, Alameda Research (defunct post-2022), GSR, Galaxy Digital’s trading desk (Genesis), Cumberland (crypto-focused).

Hybrid and newer players: Amber Group, DWF Labs, Auros.

Competitors are analyzed based on crypto trading scale, venture activity, geographic footprint, incidents, and regulatory status to provide a comparative framework.

Conclusion

Jump Trading’s evolution from a top TradFi HFT shop into digital assets via Jump Crypto demonstrates how ultra‑low‑latency tech, deep capital, and a rigorous quantitative culture can scale into a durable liquidity moat across CeFi and DeFi. Its integrated flywheel—prop trading, venture investing through Jump Capital, and protocol/infrastructure building (e.g., Pyth, Firedancer, Wormhole)—amplifies competitive advantage but also heightens conflicts, concentration exposures, and governance complexity. High‑profile crisis interventions (UST defense, Wormhole recapitalization) showcased Jump’s balance‑sheet strength and ecosystem influence, yet drew regulatory, legal, and reputational scrutiny that has intensified through 2024–2025. Key forward risks span enforcement actions, exchange counterparty failures, extreme market shocks, operational complexity, and talent retention under heavier compliance burdens. If Jump can institutionalize robust controls without losing speed, capital agility, or ecosystem partnerships, it is positioned to remain a systemically important—and increasingly scrutinized—bridge between TradFi and crypto markets.

Sources

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer's views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.