Inversion Capital: Private Equity On-Chain

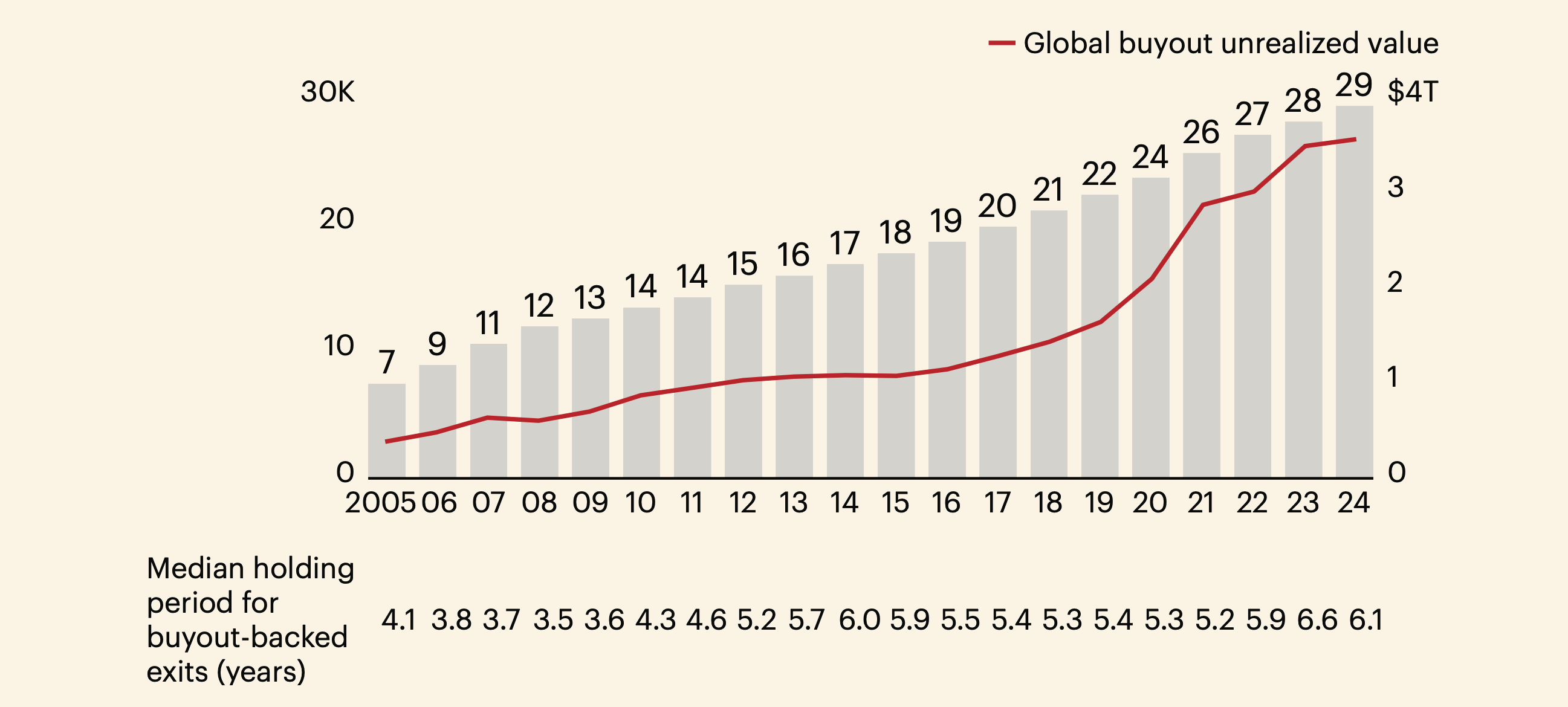

Global buyout funds are sitting on roughly $3.6 trillion in unrealized value across about 29,000 portfolio companies – a “towering” overhang that leveled off in 2024 but remains near all-time highs. Exit activity showed a tentative rebound in 2024 (global exit value jumped 34% year-on-year to $468 billion, with exit count up 22% to 1,470), yet distributions to limited partners (LPs) sank to just 11% of net asset value, the lowest in a decade. This mismatch – assets doubling since 2019 while exit values stagnate – has left general partners (GPs) under pressure to monetize aging holdings and left LPs increasingly cash-constrained and selective on new commitments.

In 2024, global buyout value rose 37% to $602B, reversing a two-year slide. Average deal size reached $849M, with $1B+ deals accounting for 77% of value.

Regional mix:

North America: value +34%, deal count +9%.

Europe: value +54%, deal count +9%.

Asia-Pacific: value +11%; China’s share of APAC value fell from 50% in 2020 to just over 25% in 2024.

Funds hold about $3T of unrealized NAV worldwide (about $2T in the US). Much of this sits in younger portfolios: ~25% from funds under 3 years and ~50% under 5, still maturing. Older funds (5+ years) are generating solid liquidity, sometimes above historical norms. The recent slowdown also follows a period of unusually strong distributions.

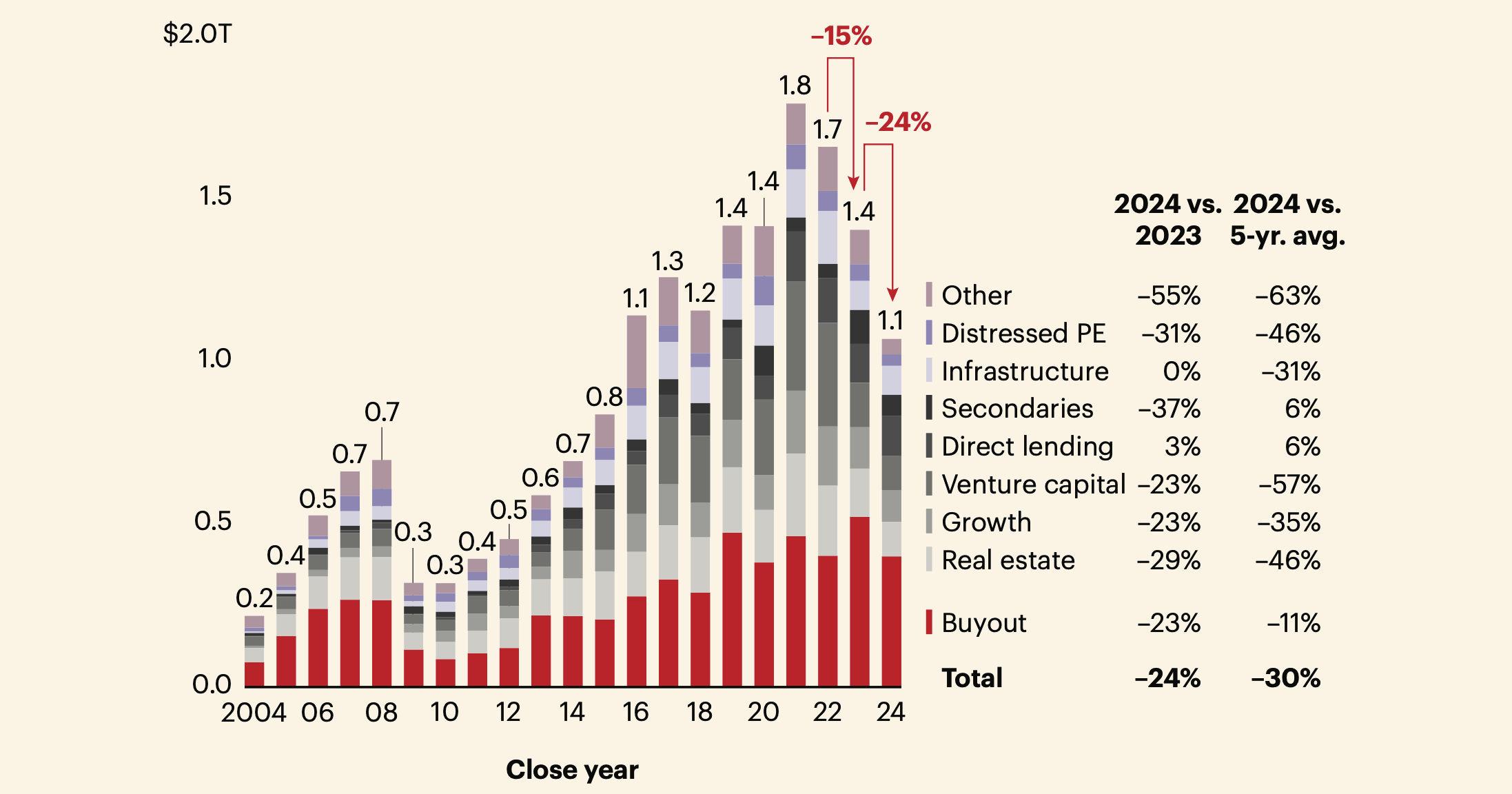

Fundraising indeed slumped for the third straight year: global private capital raised fell roughly 24% in 2024 (to about $1.1 trillion), and the number of fund closings dropped by 28% to ~3,000 – roughly half the pre-pandemic average. Investors are concentrating capital in brand-name managers, while many mid-sized funds spend 20+ months on the road to hit their targets.

Note: This post may read like a sponsored piece, but it is not. insights4vc has no financial relationship with Inversion; we simply share several of the founder’s theses. We recognize that a paradigm-shifting model comes with trade-offs and execution risk, and we’ll evaluate outcomes critically.

Inversion Capital’s Crypto-Native Buyout Strategy

Enter Inversion Capital, a newly launched firm that exemplifies this next-generation approach to private equity. Founded by crypto investor Santiago Roel Santos in 2025, Inversion raised a $26.5 million seed round on September 8, 2025 to fund its vision of “crypto-native private equity”. Previously, Santiago was a Partner at ParaFi Capital, an institutional blockchain investor managing over $1 billion. He also held investment roles at Sageview Capital, a $2 billion growth equity firm focused on software and tech-enabled businesses, and at JP Morgan’s Investment Banking Financial Sponsors Group.

The round was led by Dragonfly Capital and drew an eclectic investor base of 24 participants – including 19 venture firms and even a traditional asset manager, VanEck. Notable backers alongside Dragonfly and VanEck included HashKey Capital, ParaFi, Mirana Ventures, Wintermute, and other leading Web3 investors. This strong syndicate reflects confidence in Inversion’s thesis: that blockchain technology can fundamentally improve the businesses it acquires and accelerate mainstream adoption of crypto in the process.

Inversion operates a dual-entity model comprising Inversion Labs and Inversion Capital. The $26.5 million seed funding is earmarked for Inversion Labs – the firm’s technology development arm – to build and “bootstrap” a core blockchain platform that will be deployed across portfolio companies. In parallel, the team is raising a separate private equity fund (under the Inversion Capital banner) to acquire target businesses and execute on its deal pipeline. This structure ensures that Inversion’s blockchain engineering is well-resourced and purpose-built for operational integration, while its buyout fund will supply the acquisition capital.

September 9: Santiago R Santos replied on X that “Echo is planned,” implying Cobie’s Echo platform - https://echo.xyz/ will likely include a future round for retail investors. Timing and details were not provided.

The firm’s leadership blends deep crypto and Wall Street experience: Santos is joined by a team of eight including COO Suzanne Dannheim. Prior to joining Inversion in 2025, Suzanne led US & EMEA crypto product development, strategy, and distribution within the Firmwide Digital Assets team at Goldman Sachs, informed in part by her early foray into the crypto industry as a passion project in 2016. Suzanne started her career in the Emerging Markets FX and Rates trading desk at Goldman Sachs.This combination of traditional finance know-how and Web3 expertise underpins Inversion’s ability to navigate both worlds.

At the heart of Inversion’s model is making blockchain invisible to end-users while harnessing its benefits under the hood. “Our North Star is to make crypto invisible to our users. They won’t see how the technology works, but they’ll feel the impact. It’s going to be faster, better and cheaper,” Santos explains. Inversion is not buying companies with crypto, nor focused on crypto-native businesses themselves. Rather, “we are a traditional buyout firm targeting low-tech, low-margin businesses where we see a clear path to growing EBITDA by leveraging blockchain as a better operating system,” as Dannheim puts it.

The firm specifically targets industries burdened by outdated, inefficient processes – for example, telecommunications, banking, or other utility-like sectors with large customer bases and thin margins. These are businesses where incremental efficiency gains can translate into significant profit improvement. Inversion’s thesis is that blockchain can serve as a new operating layer to cut costs, increase speed, and enable new revenue streams in such companies.

Technology Choice – Avalanche

To implement this, Inversion is building a custom blockchain network using the Avalanche protocol. Avalanche was chosen for its high performance and flexibility – it allows Inversion to launch a dedicated permissioned subnet with tailored parameters (privacy, fees, governance) while still remaining interoperable with the broader Avalanche ecosystem.

“Building the largest and most efficient customer acquisition channel for crypto requires a highly performant and customizable infrastructure… Avalanche became an obvious choice,” — said Inversion’s founder, Santiago R. Santos

By running its own Avalanche-based chain, Inversion can ensure its portfolio companies get the benefits of blockchain (fast transaction throughput, smart contracts, asset tokenization capabilities) without the unpredictability or congestion of a general public chain. In effect, Inversion gains full control over a blockchain environment that all its businesses can use – a private-yet-public network that connects to mainstream crypto rails when needed. This approach provides a unified tech stack across the portfolio, akin to an in-house operating system.

Why VanEck invested in Inversion (By Wyatt Lonergan, Juan Lopez)

Thesis: Inversion applies a private-equity style acquisition model to crypto. It buys real businesses with existing users, then embeds blockchain rails to create immediate, revenue-backed on-chain activity.

Founder quality: Strong conviction in Santiago Roel Santos for his crypto depth, commercial instincts, and clear vision to refactor finance on open rails.

Distribution first: Rather than competing for developers, Inversion acquires companies that already have customers. This treats blockspace as a commodity and prioritizes user bases where embedded finance can win.

Revenue over speculation: Focus on cash-generating businesses that contribute to “on-chain GDP,” not headline TVL. This supports differentiated, durable network activity from day one.

Crypto as infrastructure: End users do not need to see blockchain. They get faster, cheaper payments and financial services with better UX.

Secular tailwind: Inversion sits at the center of stablecoin adoption as payment volumes migrate to crypto rails. The strategy targets the highest ROI front-ends to accelerate that shift.

Structural upside: Potential to build an evergreen, on-chain conglomerate that captures value at the chain level, a Berkshire-like model for crypto.

Blockchain-Driven Value Creation vs. Traditional PE

Inversion’s operational playbook flips the script on traditional private equity value creation. Rather than relying on financial engineering, cost-cutting, or purely managerial improvements, Inversion’s primary lever is technology engineering. Upon acquiring a company, Inversion plans to “replace inefficient infrastructure and systems with crypto rails,” deploying blockchain-based solutions for core processes like payments, identity management, data sharing, supply chain tracking, and record-keeping. By using smart contracts and decentralized protocols in place of legacy IT systems, the goal is to make businesses run markedly “faster, better, and cheaper” – improving transaction speeds, enhancing transparency, and eliminating middleman fees. These efficiencies should flow through to higher margins and more scalable operations.

Ultimately, Inversion aims to turn solid but under-optimized companies into “leaders in their industry with best-in-class margins” through blockchain-enabled productivity gains. Crucially, this strategy is not about launching new tokens or speculative crypto projects. “The strategy is not token speculation. It is operational modernization that uses on-chain rails for payments, identity, data integrity, and programmable workflows,” Inversion emphasizes. In other words, blockchain is a means to an end – a tool to drive real-world business performance – rather than an end in itself.

This tech-centric value creation comes at an opportune time. As discussed, high interest rates have made debt-driven LBO tricks far less effective, increasing the premium on genuine operating improvements. Inversion’s model addresses that head-on. By introducing blockchain and automation, the firm expects to boost EBITDA organically – a form of alpha generation well-suited to a climate where multiple expansion is hard to come by.

LBO Revolution of the 1980s

Inversion explicitly draws parallels to the leveraged buyout revolution of the 1980s, which used financial innovation (junk bond financing) to redefine private equity’s scope. Santos argues that a similar inflection point is here, with “crypto engineering” poised to reinvent how deals are financed and how value is created, much as junk debt once did. Inversion even earns the moniker of a “Berkshire Hathaway on-chain” – reflecting its plan to acquire a diversified portfolio of traditional businesses and improve them via blockchain, just as Berkshire buys companies and optimizes them (albeit with Web3 tech rather than managerial prowess alone).

In the 1980s, pioneers like KKR (Kohlberg Kravis Roberts) revolutionized private equity by aggressively using high-yield debt to acquire companies – the era memorably chronicled in “Barbarians at the Gate.” This LBO boom showed how financial innovation (junk bond financing) could dramatically expand the scale and scope of private equity. Firms could do larger deals and take public conglomerates private, unlocking value through restructuring and eventual resale. The LBO innovation was controversial but ultimately became a mainstream tool, underpinning the growth of the multi-trillion-dollar PE industry.

Fast forward to today: blockchain and crypto integration could be a similar inflection point. While the analogy isn’t perfect, the “crypto engineering” that Inversion Capital touts draws explicit inspiration from the LBO revolution.

“Just like KKR revolutionized private equity buyouts with financial engineering in the 1980s, Inversion is aiming to do the same with crypto engineering,” says Inversion’s founder - Santiago R. Santos.

The idea is that a new set of techniques – tokenization, decentralized finance, smart contracts – can reinvent how deals are financed, how ownership is structured, and how value is created in businesses (much as junk bonds and aggressive takeovers did in the ’80s).

Some specific parallels and contrasts:

Democratization vs. Consolidation: LBOs were a tool for big players and concentrated ownership (few investors could buy junk bonds). In contrast, blockchain tends toward democratization (many investors can hold tokens). Crypto integration could open private equity to a wider investor base, flipping the 1980s script of exclusivity on its head.

Regulatory Scrutiny: Both waves attract regulators’ eyes. The 1980s LBO frenzy led to concerns about debt levels and corporate raiding, eventually resulting in some regulations and market corrections. Crypto in private markets similarly raises questions (investor protection, systemic risks) that regulators are now grappling with. Each innovation forced regulatory evolution.

Technology-Driven Speed: Junk bond deals still relied on traditional financial plumbing (manual processes, physical certificates for bonds, etc.). Blockchain operates at internet-speed – value can be transferred globally in seconds on-chain. This could make the pace of transactions and transformations even faster than the 1980s, albeit tempered by smart contract code and network constraints.

Public Perception: Both LBOs and crypto had image problems initially – LBO firms as “barbarians,” crypto as the Wild West of finance. Over time, LBOs gained acceptance as their success stories (and returns) spoke for themselves. Crypto integration may follow a similar trajectory: skepticism giving way to acceptance as tangible benefits are demonstrated (e.g., a successful tokenized fund with high liquidity, or a blockchain-run business outperforming peers).

Beyond private equity, it’s instructive to consider the broader technological adoption curves of related innovations:

E-commerce in the 1990s-2020s: The early days of e-commerce witnessed a speculative bubble—the dot-com boom—that burst in 2000. However, the underlying trend of online retail growth was genuine. Over the subsequent decades, e-commerce expanded from virtually non-existent to a significant portion of global retail sales. In 2023, e-commerce accounted for 19.4% of total retail sales worldwide, and this figure is projected to reach 22.6% by 2027. Companies like Amazon emerged stronger than ever post-bubble. Cryptocurrencies have experienced similar hype cycles (e.g., the ICO boom and bust in 2017-2018), yet each cycle leaves behind greater infrastructure and adoption. Today, major retailers and payment processors accept or use cryptocurrencies, akin to how brick-and-mortar stores gradually embraced online channels.

Software-as-a-Service (SaaS) in the 2000s-2010s: When SaaS first emerged, many large enterprises were hesitant to host critical software in the cloud due to concerns about security, reliability, and control—much like apprehensions today about placing financial assets on public blockchains. Over time, SaaS proved its worth by offering more frequent updates, lower IT overhead, and scalability, becoming the default model for software delivery. Similarly, banks and institutions are gradually overcoming their reservations as blockchain solutions demonstrate security and efficiency. Just as SaaS gained trust and a clear regulatory framework (for data security, etc.), blockchain-based finance is progressively establishing standardized practices and receiving regulatory guidance.

Internet Adoption S-Curve: Globally, cryptocurrency adoption appears to be tracking an S-curve similar to the internet's early days. Analysts have noted that the number of cryptocurrency users worldwide is expected to reach 861 million by 2025, with a user penetration rate of 11.02%. Each new wave—from early Bitcoin enthusiasts to retail speculators, institutions, and now possibly nation-states or large enterprises—brings a broader base of adoption. As with any technology, adoption is not linear; it accelerates as the technology matures and becomes easier to use.

In essence, crypto and blockchain are on a trajectory that mirrors past tech transformations. The integration of crypto into private equity and institutional finance might seem niche today – just as only a few deals in the 1980s used LBO techniques, or only a few retailers sold online in 1995. But those small beginnings can herald sweeping changes. The combination of market forces (need for liquidity and efficiency) and technological momentum (blockchain maturation) suggests that we could be in the early stages of a major financial innovation cycle. The eventual impact might be as profound for the structure of asset ownership and capital markets as LBOs were, or as SaaS was for software delivery.

A Crypto-Enabled Buyout Model and its Go-To-Market Edge

Beyond efficiency gains, Inversion’s strategy offers a novel solution to crypto’s perennial go-to-market challenge. One of the biggest hurdles for blockchain adoption has been getting mainstream users on board; people are often wary of new wallets, tokens, or technical complexity. Inversion’s answer is elegantly simple: don’t ask users to adopt crypto – instead, embed crypto into services they already use. By acquiring companies with large, loyal customer bases (say a mobile carrier, a bank, or an internet service provider) and quietly integrating blockchain features, Inversion onboards potentially millions of users into Web3 passively. For example, if Inversion buys a telecom operator, that business could start offering its customers a built-in digital wallet with stablecoins for faster remittances, or tokenized loyalty points, or verifiable on-chain records for service contracts.

Customers would enjoy faster and cheaper services (e.g. instant bill settlements, improved rewards tracking, better data security) without needing to understand that blockchain is under the hood. The crypto infrastructure remains invisible to them, but its benefits drive a superior user experience. In the financial services context, an acquired bank could use blockchain for more efficient compliance and settlement, passing the savings or speed on to customers. Inversion is essentially turning its portfolio companies into crypto adoption vectors – bringing the mountain to Mohammed by infusing blockchain into established businesses and piggybacking on their existing customer trust and distribution. This approach differs from traditional PE in that it doesn’t just seek operational improvement, but also has a technology adoption dimension: the PE firm itself becomes a catalyst for bringing Web3 into the mainstream consumer realm.

Venture capital and private equity are not separate worlds

They sit on a single spectrum defined by three variables: the degree of operating control, the concentration of exposure in a few businesses, and the share of value captured per business. The most interesting opportunity today sits between the two ends of that spectrum. In this middle zone, companies mix software with ownership or deep operational influence. The goal is simple: apply a proven operating playbook through code, then keep more of the upside than pure software allows while scaling faster than classic buyouts usually can.

Push factors from VC include crowded B2B SaaS, tougher customer acquisition, and AI compressing moats; pull factors toward hybrids include embedded monetization in payments, marketing, and lending, plus AI that makes interventions cheaper and more repeatable. Practically this shows up as three models: a crown jewel acquisition that becomes the captive first customer for a proprietary stack, a venture roll up that standardizes many similar operators with shared systems and data driven underwriting, and a business in a box that launches new operators with a software and services bundle.

The result is a shift from financial engineering to technology led operating improvement, higher value capture by participating in variable economics and equity, and stronger distribution through control of businesses that already have customers. It works best in fragmented markets with repeatable workflows and in verticals where embedded payments or financing can materially move unit economics, but it carries integration, channel conflict, regulatory, and financing risks that require tight governance in a higher rate world. The scorecard should combine software KPIs like net revenue retention and attach rate with operating KPIs like post playbook EBITDA uplift and integration cycle time, plus capital health metrics such as leverage and interest coverage.

Inversion fits this middle zone by combining crown jewel and roll up tactics with blockchain as an operating system for payments, identity, data integrity, and programmable workflows, aiming for measurable EBITDA gains through operational modernization rather than token speculation.

Conclusion

Inversion’s early moves bear watching. With fresh capital in Inversion Labs and a fundraise underway for acquisitions, the firm is reportedly scouting targets in sectors like telecom and finance where legacy infrastructure creates obvious pain points. Executing this strategy will not be without risks – seamless blockchain integration is a new endeavor, and not every business will benefit equally from “crypto rails.” Execution and tech adoption risk will have to be managed on top of normal business risks.

However, if Inversion succeeds, it could pioneer a new class of blockchain-driven buyouts that address many of the industry’s current challenges. By unlocking liquidity (through potential asset tokenization down the line), driving true operational alpha, and accelerating crypto’s real-world foothold, Inversion’s model offers a bold vision for private equity’s future. It marries the discipline of traditional PE with the dynamism of Web3 technology. In a period when the private equity industry is forced to evolve – facing high-rate headwinds, a glut of unexited assets, and LPs clamoring for innovation – Inversion Capital’s experiment in blockchain-driven buyouts may well signal how the next generation of value creation will be achieved. The coming years will reveal whether this “Berkshire on-chain” can deliver on its promise of faster, better, cheaper companies and, in the process, blaze a trail for crypto-integrated private equity.

Inversion Capital:

Sources

Cover Artwork

Piazza San Marco

Canaletto (Giovanni Antonio Canal), c. 1720s

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer's views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.

Making crypto invisible to end users is the only credible route to mainstream adoption

Great post!!