Private Equity On-Chain (Inversion Capital)

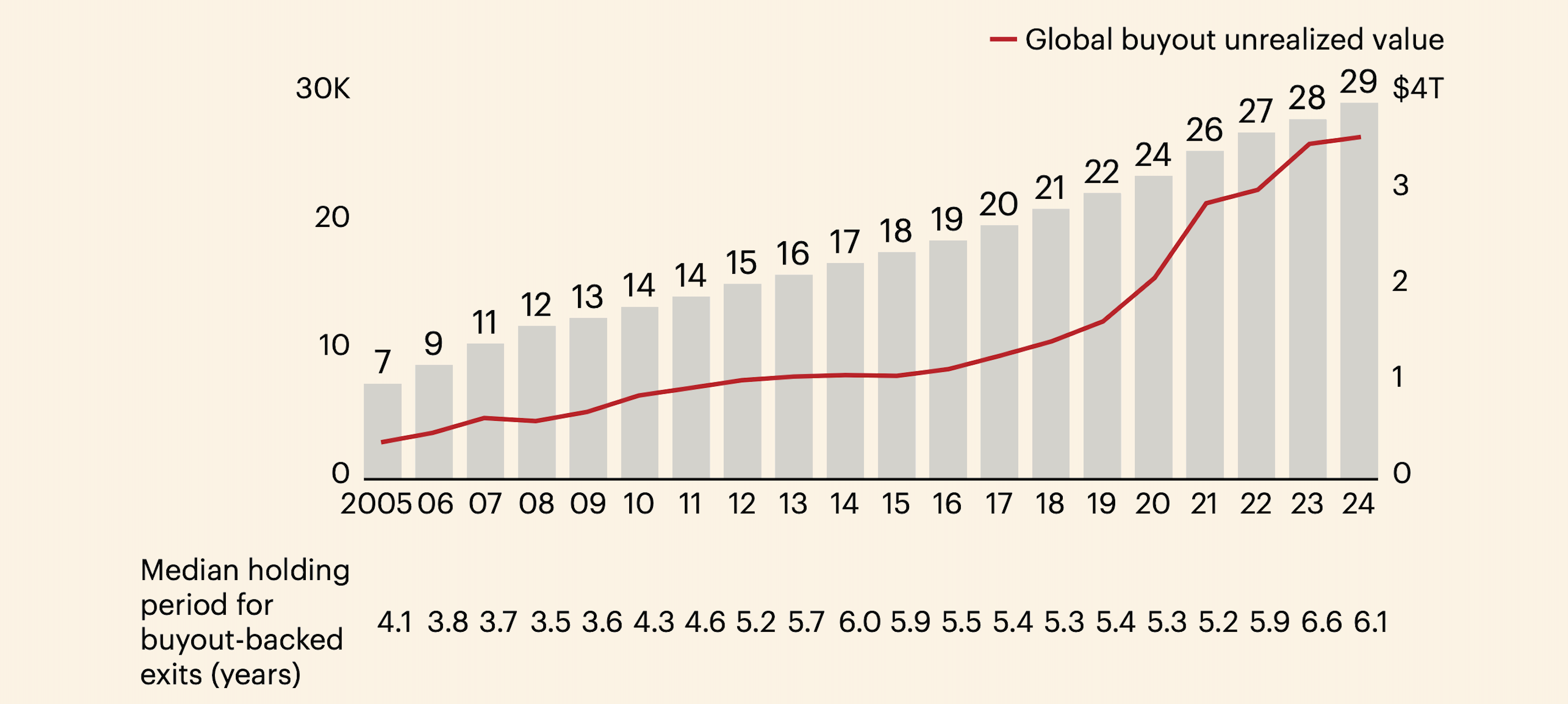

In 2025, with ~$3.6 trillion in unrealized value across 29,000 companies, Private Equity (PE) firms are navigating a complex market landscape. This report examines how financial institutions, particularly PE firms, are leveraging blockchain technology to address these challenges. Future publications will continue to explore this evolving topic, and importantly, none of the institutions mentioned have sponsored this analysis.

Private equity firms are increasingly turning to blockchain, notably through asset tokenization, to broaden investor access and enhance liquidity. A notable example is KKR, a $491 billion asset manager, which in 2022 tokenized a portion of its Health Care Strategic Growth Fund II (HCSG II) on the Avalanche blockchain. Partnering with digital asset platform Securitize, KKR enabled qualified investors to access tokens representing shares of the $4 billion PE fund.

According to KKR, this on-chain tokenization “lowers investment minimums, improves digital investor onboarding and compliance protocols, and increases potential for liquidity through a regulated alternative trading system”.

KKR's move to democratize access to a traditionally illiquid fund—offering smaller minimum investments and automating compliance via smart contracts—is more than just a technical upgrade. It’s a “significant breakthrough” that signals a broader trend: top PE firms are exploring Web3 to modernize fundraising and investor relations.

Other private market giants are following suit. Since March 2022, Hamilton Lane has been at the forefront of tokenization, striking key partnerships with ADDX, Securitize, and Allfunds Blockchain to open private markets to a wider investor base. In January 2025, a new collaboration with Republic brought tokenized funds within reach of U.S. retail investors, underscoring the firm's commitment to transparency, liquidity, and operational efficiency as it manages $947 billion in assets.

These initiatives aren’t about chasing speculative crypto gains. Instead, PE managers are leveraging blockchain as a new infrastructure for fund ownership—boosting liquidity in an asset class notorious for long lock-ups. By enabling fractional ownership and transferability, blockchain is rewriting the rules of private equity investment.

But the impact of blockchain on private equity extends beyond tokenization. Leading firms are exploring blockchain's potential to streamline operations in portfolio companies—from supply chain tracking and payments to data management. As buyout giants invest in crypto startups and experiment with blockchain in back-office processes, the institutional mindset is shifting. Blockchain is no longer just about cryptocurrencies; it's a powerful toolset for both assets and operations.

$3.6 Trillion in Unrealized Assets and Efficiency Imperatives

The private equity market in early 2025 faces a challenging environment marked by a substantial overhang of unrealized assets. Rising interest rates, a slowdown in exits, and a backlog of portfolio holdings have intensified the pressure on firms to generate liquidity and enhance returns. As of 2025, buyout firms are managing approximately 29,000 companies with a staggering $3.6 trillion in unrealized value. This accumulation of unsold assets surpasses levels observed during the 2008–09 financial crisis.

In 2024, global buyout investment value increased by 37% year-over-year to $602 billion, reversing a two-year decline. The average deal size rose to $849 million, with 77% of total deal value attributed to transactions of $1 billion or more. Regional performance varied significantly:

North America: Deal value grew by 34%, with a 9% increase in deal count.

Europe: The highest growth at 54%, also with a 9% increase in transactions.

Asia-Pacific: A modest 11% growth in deal value, with China's share of regional deal value dropping from 50% in 2020 to just over 25% in 2024.

Exit Activity and Liquidity Challenges

The exit environment showed some recovery, with global exit value rising by 34% to $468 billion and the number of exits increasing by 22% to 1,470. Key exit channels included:

Sponsor-to-Sponsor Deals: Up 141%, contributing $181 billion in value.

Strategic Deals: Flat at $261 billion, highlighted by significant sales like SRS Distribution to Home Depot for $18 billion.

Initial Public Offerings (IPOs): Continued to underperform, representing only 6% of exit value.

Despite these gains, exit volumes remain below the five-year average, highlighting persistent liquidity pressures. Distributions to investors dropped to a historic low of 11% of net assets, and the extended holding periods of portfolio companies—over 50% held for more than four years—reflect the slow pace of asset turnover.

Fundraising Trends and Capital Flows

Fundraising declined for the third consecutive year, with global private capital raised falling by 24% to $1.1 trillion in 2024. The number of funds closed also dropped by 28% to 3,000, half the pre-pandemic average. Notably, North America experienced a 34% drop in buyout funds raised, while Europe remained stable and Asia-Pacific saw a 13% increase.

Investors favored top-tier funds, with the top 10 funds capturing 36% of all buyout capital raised. Despite 85% of funds reaching their fund-raising targets, the average time to close remained high at 20 months, with 38% of funds taking two years or more to close.

Rising Interest Rates

The end of the low-interest-rate era has significantly increased borrowing costs, challenging a core driver of past PE returns: multiple expansion through leverage. With central bank benchmark rates in major economies such as the U.S. and the Eurozone hovering around 5.5% and 4.5%, respectively, debt can no longer mask mediocre performance. Instead, operational efficiency and value creation are now critical to driving returns.

Future buyout returns will increasingly rely on growth in revenue and EBITDA rather than financial engineering. Managers who can enhance portfolio company operations are likely to perform better in this high-rate environment.

Blockchain as a Potential Solution

The current market dynamics create an opportunity for blockchain integration as a strategic tool for private equity firms:

Liquidity through Tokenization: Tokenizing PE holdings, as demonstrated by KKR, could provide interim liquidity for general partners (GPs) and limited partners (LPs), enabling partial exits and unlocking capital from the $3.6 trillion in unrealized assets.

Operational Efficiency: Blockchain technology can streamline operations such as payments, compliance, and data sharing, potentially improving margins and enhancing portfolio company performance.

Access to New Capital Pools: On-chain assets could attract non-traditional investors, including retail and foreign investors, through appropriate regulatory frameworks, broadening the capital base.

Strategic Differentiation: Firms leveraging blockchain for earlier liquidity or enhanced performance can differentiate themselves in a competitive market, attracting investment from LPs.

While the private equity market showed signs of recovery in 2024, the overhang of unrealized assets and the challenges of a high-interest-rate environment necessitate strategic agility and innovation. Emphasizing operational improvements and exploring technologies like blockchain could provide a path to liquidity and sustained performance. However, success will require careful navigation of regulatory, market, and operational risks to capitalize on emerging opportunities effectively.

Inversion Capital: Bringing Private Equity On-Chain

Inversion Capital, founded by Santiago Roel Santos, exemplifies a novel approach to institutional blockchain adoption through its "crypto-native private equity" strategy. This model distinguishes itself by not only utilizing blockchain for fund tokenization but also by integrating blockchain technology into the core operations of acquired businesses. Inversion Capital employs the Avalanche blockchain to enhance operational efficiencies within its portfolio companies. This approach represents an evolution in private equity, leveraging Web3 technologies to create value. A comparative analysis of Inversion's strategy—highlighting its use of the Avalanche blockchain, unique acquisition model, and focus on operational improvements—contrasts with traditional private equity methodologies.

Use of Avalanche Blockchain

Inversion is launching its own custom Layer-1 blockchain built on Avalanche, tailored to support its portfolio companies. Avalanche was chosen for its high performance and flexibility – allowing Inversion to customize the network’s parameters (permissioning, privacy, fees) while still being interoperable with the broader Avalanche ecosystem.

“Building the largest and most efficient customer acquisition channel for crypto requires a highly performant and customizable infrastructure… Avalanche became an obvious choice,” — said Inversion’s founder, Santiago R. Santos

By operating a dedicated Avalanche subnet, Inversion can ensure its businesses benefit from blockchain tech (such as fast transactions and smart contracts) without the scalability limits or unpredictability of using a general public chain. This private-yet-public blockchain approach provides Inversion both control and connectivity – a foundation to bring real-world companies on-chain.

Acquisition Model (“Berkshire On-Chain”)

Inversion’s strategy is often described as “Berkshire Hathaway on-chain”, reflecting its plan to acquire traditional businesses and anchor them on its blockchain. Unlike classic PE firms that might rely mostly on financial restructuring, Inversion targets businesses with large, loyal customer bases (e.g. in sectors like mobile services, banking, or internet connectivity) and then integrates crypto infrastructure into their products and operations. The premise is that many mainstream users can be brought into Web3 not by speculative crypto trading, but by using essential services enhanced with blockchain features. For example, an Inversion-acquired telecom or bank could offer its customers blockchain-based benefits like stablecoin wallets, loyalty tokens, or supply chain transparency – all without the user needing to understand crypto (the crypto infrastructure is “invisible” to them). This “go-to-market” innovation means Inversion doesn’t wait for businesses to adopt crypto; it buys them outright and onboards their users to blockchain-enabled services by default.

Operational Improvements through Crypto

The core thesis of Inversion is that blockchain can make businesses run “faster, better, and cheaper.” After acquiring a company, Inversion plans to “replace inefficient infrastructure and systems with crypto rails”, thereby improving speed, transparency, and cost-efficiency in operations. By using smart contracts and decentralized protocols (for payments, data, identity, etc.), businesses can streamline processes that were previously slow or costly. The end goal is to create “leaders in their industry with best-in-class margins” by virtue of these crypto-powered efficiencies. Inversion also intends to leverage decentralized finance (DeFi) and decentralized physical infrastructure networks (DePIN) within its businesses, potentially reducing reliance on traditional financing or intermediaries. For instance, a portfolio company could use DeFi liquidity pools for funding or stablecoins for cross-border transactions, cutting out layers of fees. This contrasts with traditional PE’s playbook, which often focuses on cutting costs through layoffs or optimizing supply chains without fundamentally altering the IT backbone.

Inversion’s crypto-centric improvements are a new way to boost EBITDA – one particularly suited for a world where tech-driven productivity is key.

Comparative Perspective: Compared to traditional private equity, Inversion Capital’s approach is distinct on several fronts:

Value Creation Lever: Classic PE relies heavily on financial engineering (debt leverage, refinancing) and conventional operational tweaks. Inversion relies on technology engineering – introducing blockchain to create value. This is especially relevant as rising interest rates today make debt-fueled strategies less attractive, increasing the need for true operational gains.

Investment Horizon and Liquidity: Traditional PE funds have ~5-7 year horizons per investment and face illiquidity until exit. Inversion’s on-chain approach could, in theory, allow continuous value realization – if portfolio companies or their assets are tokenized, stakeholders might trade exposure even before formal exits. It’s a hybrid of operating company and investment platform, potentially offering more flexibility.

Scalability of Adoption: Inversion directly brings potentially millions of existing customers (of acquired firms) into contact with blockchain-based services. Traditional PE doesn’t typically impact technology adoption among consumers; here, the PE firm becomes a crypto adoption vector. This addresses crypto’s “go-to-market problem” by piggybacking on established businesses.

Risk Profile: Inversion is pushing into uncharted territory by betting that blockchain integration will yield the promised efficiencies. Execution risk is significant – not all businesses may seamlessly benefit from crypto rails. Traditional PE might view this as adding tech integration risk on top of normal business risks. However, if successful, it could unlock unprecedented margins and network effects.

Helium Mobile Network

One of the first transactions for Inversion Capital involves the integration of Helium's decentralized wireless network into a newly acquired MVNO (Mobile Virtual Network Operator). By offloading mobile data to Helium's network, Inversion Capital aims to reduce telecom operational costs by up to 50%, significantly enhancing profitability. The investment strategy includes staking 100,000 HNT tokens to become a Service Provider on the Helium Mobile Network, targeting international markets and aiming to drive substantial demand for data credits and HNT burn. Rapid scaling is planned through strategic partnerships, such as collaborating with convenience stores to quickly deploy Helium hotspots, with an emphasis on international expansion, particularly in Latin America.

Inversion Capital’s strategy thus represents a bold convergence of private equity and blockchain. It’s essentially operational alpha via Web3. Time will tell if this “Berkshire onchain” can replicate the success of 1980s buyout barons using a very different toolkit. Nonetheless, its emergence highlights the creativity now blossoming at the intersection of traditional finance and crypto.

LBO Revolution of the 1980s

Financial history offers a useful parallel in the leveraged buyout (LBO) wave of the 1980s, which transformed private equity. The question is whether crypto integration could play a similar game-changing role in the coming decades.

In the 1980s, pioneers like KKR (Kohlberg Kravis Roberts) revolutionized private equity by aggressively using high-yield debt to acquire companies – the era memorably chronicled in “Barbarians at the Gate.” This LBO boom showed how financial innovation (junk bond financing) could dramatically expand the scale and scope of private equity. Firms could do larger deals and take public conglomerates private, unlocking value through restructuring and eventual resale. The LBO innovation was controversial but ultimately became a mainstream tool, underpinning the growth of the multi-trillion-dollar PE industry.

Fast forward to today: blockchain and crypto integration could be a similar inflection point. While the analogy isn’t perfect, the “crypto engineering” that Inversion Capital touts draws explicit inspiration from the LBO revolution.

“Just like KKR revolutionized private equity buyouts with financial engineering in the 1980s, Inversion is aiming to do the same with crypto engineering,” says Inversion’s founder - Santiago R. Santos.

The idea is that a new set of techniques – tokenization, decentralized finance, smart contracts – can reinvent how deals are financed, how ownership is structured, and how value is created in businesses (much as junk bonds and aggressive takeovers did in the ’80s).

Some specific parallels and contrasts:

Democratization vs. Consolidation: LBOs were a tool for big players and concentrated ownership (few investors could buy junk bonds). In contrast, blockchain tends toward democratization (many investors can hold tokens). Crypto integration could open private equity to a wider investor base, flipping the 1980s script of exclusivity on its head.

Regulatory Scrutiny: Both waves attract regulators’ eyes. The 1980s LBO frenzy led to concerns about debt levels and corporate raiding, eventually resulting in some regulations and market corrections. Crypto in private markets similarly raises questions (investor protection, systemic risks) that regulators are now grappling with. Each innovation forced regulatory evolution.

Technology-Driven Speed: Junk bond deals still relied on traditional financial plumbing (manual processes, physical certificates for bonds, etc.). Blockchain operates at internet-speed – value can be transferred globally in seconds on-chain. This could make the pace of transactions and transformations even faster than the 1980s, albeit tempered by smart contract code and network constraints.

Public Perception: Both LBOs and crypto had image problems initially – LBO firms as “barbarians,” crypto as the Wild West of finance. Over time, LBOs gained acceptance as their success stories (and returns) spoke for themselves. Crypto integration may follow a similar trajectory: skepticism giving way to acceptance as tangible benefits are demonstrated (e.g., a successful tokenized fund with high liquidity, or a blockchain-run business outperforming peers).

Beyond private equity, it’s instructive to consider the broader technological adoption curves of related innovations:

E-commerce in the 1990s-2020s: The early days of e-commerce witnessed a speculative bubble—the dot-com boom—that burst in 2000. However, the underlying trend of online retail growth was genuine. Over the subsequent decades, e-commerce expanded from virtually non-existent to a significant portion of global retail sales. In 2023, e-commerce accounted for 19.4% of total retail sales worldwide, and this figure is projected to reach 22.6% by 2027. Companies like Amazon emerged stronger than ever post-bubble. Cryptocurrencies have experienced similar hype cycles (e.g., the ICO boom and bust in 2017-2018), yet each cycle leaves behind greater infrastructure and adoption. Today, major retailers and payment processors accept or use cryptocurrencies, akin to how brick-and-mortar stores gradually embraced online channels.

Software-as-a-Service (SaaS) in the 2000s-2010s: When SaaS first emerged, many large enterprises were hesitant to host critical software in the cloud due to concerns about security, reliability, and control—much like apprehensions today about placing financial assets on public blockchains. Over time, SaaS proved its worth by offering more frequent updates, lower IT overhead, and scalability, becoming the default model for software delivery. Similarly, banks and institutions are gradually overcoming their reservations as blockchain solutions demonstrate security and efficiency. Just as SaaS gained trust and a clear regulatory framework (for data security, etc.), blockchain-based finance is progressively establishing standardized practices and receiving regulatory guidance.

Internet Adoption S-Curve: Globally, cryptocurrency adoption appears to be tracking an S-curve similar to the internet's early days. Analysts have noted that the number of cryptocurrency users worldwide is expected to reach 861 million by 2025, with a user penetration rate of 11.02%. Each new wave—from early Bitcoin enthusiasts to retail speculators, institutions, and now possibly nation-states or large enterprises—brings a broader base of adoption. As with any technology, adoption is not linear; it accelerates as the technology matures and becomes easier to use.

In essence, crypto and blockchain are on a trajectory that mirrors past tech transformations. The integration of crypto into private equity and institutional finance might seem niche today – just as only a few deals in the 1980s used LBO techniques, or only a few retailers sold online in 1995. But those small beginnings can herald sweeping changes. The combination of market forces (need for liquidity and efficiency) and technological momentum (blockchain maturation) suggests that we could be in the early stages of a major financial innovation cycle. The eventual impact might be as profound for the structure of asset ownership and capital markets as LBOs were, or as SaaS was for software delivery.

Hedge Funds and Banks

Renowned for their opportunistic and innovative investment strategies, hedge funds have emerged as some of the earliest institutional adopters of digital assets. Many funds actively trade cryptocurrencies, invest in blockchain-focused startups, and harness distributed ledger technology to enhance transactional efficiency.

As of March 2025, the crypto investment landscape among hedge funds has significantly expanded:

AUM in Dedicated Crypto Hedge Funds: The total assets under management are expected to exceed $75 billionby year-end.

Traditional Hedge Funds Investing in Crypto: Nearly 47% of traditional hedge funds now hold digital assets, up from 29% in 2023.

These trends highlight the growing acceptance of cryptocurrencies as a legitimate asset class for diversification and alpha generation within the hedge fund industry.

Several high-profile hedge fund managers moved into crypto markets in recent years. For example, Brevan Howard and Tudor Investment launched crypto-focused funds, and quantitatively driven firms began arbitraging inefficiencies in digital asset markets. By 2024, 85% of asset managers surveyed were actively exploring cryptocurrency and digital assets for their clients.

Hedge funds often cite portfolio diversification and the strong returns of early crypto investments as motivation, while leveraging their trading expertise to manage volatile markets. Bitcoin and Ethereum remain popular choices—35% of institutional crypto holdings were in BTC and 15% in ETH by 2024. Additionally, some funds explore DeFi yield strategies or invest in crypto futures and options, with derivatives accounting for approximately 12% of institutional crypto exposure.

Beyond trading, hedge funds are testing blockchain technology to enhance operational efficiency, particularly in post-trade settlement and record-keeping. Some funds have experimented with private blockchain networks to reduce settlement times for securities trades, with reports of up to 70% faster settlement in trial runs. Faster settlement can reduce counterparty risk and free up capital – a clear advantage for hedge funds engaged in high-frequency trading or complex derivatives. Additionally, custody solutions for digital assets have matured (with major banks and custodians offering services), addressing a key hurdle that previously kept institutions away.

Global banks and financial institutions are also actively engaging with blockchain, albeit with a strong focus on infrastructure and compliance use cases. Leading banks see blockchain’s potential to streamline payments, settlements, and custodial services.

One prominent example is JPMorgan Chase, which has developed its own permissioned blockchain and a dollar-pegged stablecoin, JPM Coin, for internal transfers between clients. JPMorgan’s blockchain platform Kinexys has been used for overnight repo transactions and cross-border payments, reportedly handling trillions of dollars in volume. In 2022, JPMorgan even executed a pilot DeFi trade on a public blockchain (Polygon) as part of a Monetary Authority of Singapore trial – trading tokenized deposits and government bonds using modified Aave and Uniswap protocols. This was hailed as a “monumental step” showing that even regulated banks can harness decentralized finance rails in a controlled manner. Such experiments indicate that banks are willing to venture beyond private ledgers into public blockchain ecosystems when the use-case (e.g. real-time settlement) is compelling enough.

Other banking giants have also joined the fray:

BNY Mellon and State Street (two of the world’s largest custody banks) now offer crypto custody services, with BNY Mellon alone handling $1.5 billion in digital assets in its early rollout. This marks a significant stamp of approval, as these firms provide foundational infrastructure for institutional investors.

Goldman Sachs, Morgan Stanley, and Citigroup have each established digital asset teams or trading desks to facilitate client exposure to crypto. They are helping clients trade Bitcoin futures, invest in crypto funds, or issue tokenized securities.

European and Asian banks are launching blockchain-based platforms for things like trade finance, bond issuance, and interbank settlements. For example, HSBC and others used blockchain networks (like we.trade or Marco Polo) for trade finance pilots, and Singapore’s DBS Bank issued bonds as security tokens.

Crucially, banks often partner with crypto-native firms to accelerate adoption. Visa and Mastercard have integrated stablecoin settlement in collaboration with crypto companies, and Coinbase’s partnership with JPMorgan for banking services was noted as a sign of growing synergy between crypto firms and traditional banks.

Nubank’s Stablecoin Integration

As of March 2025, Nubank, Latin America's largest digital bank, has made significant strides in integrating stablecoin technology and expanding its customer base.

Stablecoin Integration:

USDC Launch: In December 2023, Nubank partnered with Circle to introduce USD Coin (USDC), a US dollar-backed stablecoin, into its platform. This initiative aimed to provide customers with a stable digital asset less susceptible to the volatility commonly associated with other cryptocurrencies.

Rewards Program Expansion: By January 2025, Nubank extended its USDC rewards program to all users of Nubank Cripto in Brazil. Customers maintaining a minimum balance of 10 USDC in their wallets now receive a fixed annual return of 4%, credited daily with immediate liquidity. This move followed a successful pilot program that tested variable rates with a select group of users throughout the previous year.

Crypto Swap Feature: In November 2024, Nubank introduced a cryptocurrency swap tool within its app, enabling users to exchange Bitcoin (BTC), Ethereum (ETH), Solana (SOL), or Uniswap (UNI) for USDC and vice versa, with reduced fees. This feature enhances the flexibility and utility of Nubank's crypto offerings.

Customer Growth:

Milestone Achievement: Nubank's customer base has experienced remarkable growth. In Q1 2024, the bank added 5.5 million customers, reaching a total of 99.3 million globally by March 31, 2024. By December 2024, Nubank surpassed 114 million customers, marking a 22% increase from the previous year. This expansion solidifies Nubank's position as one of the world's largest digital banks.

Berkshire Hathaway Investment

Nubank has garnered attention from prominent investors, notably Warren Buffett's Berkshire Hathaway, which invested $500 million in the company prior to its initial public offering in December 2021. In addition to Berkshire Hathaway, Nubank has attracted investments from several notable entities across various funding rounds. In June 2015, Tiger Global Management led a $30 million Series B round. Tencent invested $180 million in October 2018, acquiring a minority stake. In June 2021, Sands Capital led a $250 million extension to Nubank's Series G round, with participation from investors such as Canada Pension Plan Investment Board (CPP Investments), MSA Capital, and Sunley House Capital.

Through strategic integration of stablecoin technology and a focus on customer-centric services, Nubank continues to innovate in the digital banking sector, offering diversified financial solutions to its expanding user base.

Regulatory Challenges and Opportunities

An analysis of on-chain private equity and institutional crypto adoption necessitates a thorough examination of the regulatory landscape in the United States. Regulation remains both a significant hurdle and opportunity for integrating private assets on-chain. U.S. regulators, particularly the Securities and Exchange Commission (SEC), are tasked with adapting securities laws to accommodate blockchain-based assets, balancing innovation with investor protection.

Securities Laws and Tokenized Assets

In the U.S., most tokenized private equity interests are classified as securitiesunder the traditional Howey Test. Consequently, they must either be registered with the SEC or offered under specific exemptions (e.g., Regulation D for accredited investors, Regulation S for offshore offerings, Regulation A+ for limited public offerings). Historically, tokenized funds like KKR’s HCSG II were offered exclusively to accredited investors under existing exemptions, with tokens representing digital forms of limited partnership interests. The SEC has maintained that utilizing blockchain technology does not exempt entities from securities regulations—compliance with Know Your Customer (KYC), Anti-Money Laundering (AML), and disclosure requirements remains mandatory. This stance has largely restricted open-to-retail tokenized private equity offerings in the U.S.

Recent Regulatory Developments:

SEC Enforcement Actions: In June 2023, the SEC filed a lawsuit against Coinbase, alleging that the company had been operating as an unregistered broker, exchange, and clearing agency since 2019. However, in February 2025, the SEC dismissed its lawsuit against Coinbase, signaling a potential shift in regulatory approach.

Shift in Regulatory Approach: Under the Trump administration, the SEC has exhibited a more crypto-friendly stance, dropping investigations and legal actions against several major crypto entities, including Binance and Coinbase. This shift indicates a move towards encouraging innovation while still aiming to protect investors from fraud.

Lack of Clarity

Industry leaders have consistently argued that U.S. regulation has not kept pace with technological advancements. In January 2025, Robinhood CEO Vlad Tenev and BlackRock’s Larry Fink called for clearer regulations for tokenized securities in the U.S., warning that innovation could shift abroad if rules remain ambiguous. Tenev emphasized that outdated rules are blocking a major financial shift that could democratize private markets. This highlights the current tension: the U.S. possesses a highly developed capital market with stringent investor protection laws, which sometimes clash with the crypto ethos of open access. Regulators are concerned that allowing retail trading of private equity tokens could expose unsophisticated investors to excessive risk or fraud. Yet, without adapting rules, U.S. markets risk losing competitiveness as other regions progress.

Global Regulatory Competition

Other jurisdictions are advancing more rapidly to accommodate tokenization. The European Union’s Markets in Crypto-Assets (MiCA) regulation establishes a comprehensive framework for digital assets, providing more certainty for security tokens in Europe. Singapore, Dubai, and Switzerland have also issued regulatory sandboxes or licenses for tokenized asset platforms. This global progress pressures U.S. regulators: if U.S. firms and investors are excluded from on-chain markets, capital may flow to more accommodating regimes.

Conversely, the U.S. has an opportunity: by crafting thoughtful regulations (e.g., a new exemption or an update to the 1933 Securities Act for digital formats), it could modernize current frameworks to accommodate digital assets. Lawmakers have begun discussing bills on topics like stablecoins and tokenized assets, but as of March 2025, no comprehensive legislation has been enacted.

Key Regulatory Challenges:

Investor Accreditation and Protection: Determining whether the threshold to invest in tokenized private equity should remain high (accredited-only) or if new safeguards (such as investment size limits, enhanced disclosure via smart contracts) can enable wider access is crucial to achieving true democratization.

Secondary Trading & Liquidity: Under Rule 144, private securities typically can only be freely traded after a holding period (6–12 months) and among accredited investors. Applying these rules on-chain requires whitelisting and transfer restrictions coded into tokens. The SEC has licensed a few Alternative Trading Systems (ATS) platforms to trade security tokens within regulatory bounds. The expansion of regulated venues for token trading presents an opportunity to increase liquidity while remaining compliant.

Custody and Cybersecurity: Qualified custody of digital securities remains a gray area that the SEC is working to clarify. Recent guidance suggests stricter rules for crypto custody by investment advisers. Firms bringing private equity on-chain must ensure robust custody solutions (potentially using regulated custodians) to satisfy fiduciary duties. Smart contract vulnerabilities or key mismanagement could be disastrous; hence, regulators emphasize technological due diligence and insurance.

Transparency vs. Privacy: Blockchains are inherently transparent, which could aid regulators in monitoring transactions. However, sensitive financial information (investor identities, valuations) might require privacy. Solutions like permissioned blockchains or zero-knowledge proofs could address this issue, but regulators will need to become comfortable with new paradigms in monitoring compliance on-chain.

Opportunities

Overcoming regulatory hurdles could unlock substantial value. Tokenization could democratize private markets, allowing a wider range of investors to participate in asset classes previously limited to institutional investors. From a U.S. policy perspective, enabling broader investment in private markets could help individuals build wealth, provided appropriate safeguards are in place. Moreover, embracing on-chain finance could reinforce U.S. capital markets’ global primacy by hosting the platforms and exchanges where this new form of trading occurs, rather than ceding that to overseas hubs.

Sources:

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer's views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.