Stablecoins in Agentic Commerce

The global financial landscape as of March 2026, is characterized by the systemic transition from human-centric digital commerce to a paradigm of autonomous agentic commerce. This shift represents the most significant re-engineering of the transaction lifecycle since the introduction of the internet-native payment gateway.

Agentic commerce is defined as an economic system in which software entities act as independent actors—discovering services, negotiating complex terms, and executing financial settlement with minimal human intervention. This transformation is not merely a user-interface evolution but a structural replacement of synchronous, session-based authorization with asynchronous, mandate-based cryptographic delegation.

Underpinning this new economy is a sophisticated stack of protocols that bridge the divide between large language model (LLM) reasoning and rigid financial finality. Stablecoins, primarily USDC, have emerged as the programmable medium of exchange, now deeply integrated into both legacy card networks and native blockchain settlement layers. The market has converged on a unified model that treats retail goods and metered machine services as variants of the same underlying transaction stack, rather than separate tracks of development.

As of early 2026, agentic commerce has moved beyond prototyping into institutional adoption. AI agents are no longer treated only as decision support. They are increasingly treated as economic actors that can initiate purchases, authorize payments, and settle value transfers inside enterprise workflows.

What changed in 2025–2026

1) Standardized discovery for agents (UCP)

The Universal Commerce Protocol (UCP) standardizes how agents discover what a merchant can do using /.well-known/ucp manifests. In practice, it is becoming a common interface layer for “machine-readable commerce”, similar to what HTTP did for information exchange.

2) Verifiable intent becomes mandatory (AP2)

The Agent Payments Protocol (AP2) introduces Verifiable Digital Credentials (VDCs) so agent actions can be tied to explicit, deterministic human mandates (who authorized what, under which conditions), rather than relying on probabilistic model behavior.

3) HTTP 402 comes back for machine payments (x402)

The x402 protocol repurposes HTTP status code 402 Payment Required for M2M payments directly inside API calls. Reported adoption suggests it has scaled materially by end-2025, validating “pay-per-request” patterns without traditional checkout flows.

4) Card networks tokenize agents as first-class entities

Visa (Intelligent Commerce) and Mastercard (Agent Pay) extend network-token primitives to agent contexts. The goal is to bind payment credentials to specific agents, with consumer-defined constraints, while preserving existing risk, fraud, and dispute frameworks.

5) Stablecoin settlement becomes an institutional rail

Visa’s USDC settlement expansion signals stablecoins moving from “crypto-native” usage into institutional settlement for 24/7 money movement. The big operational impact is faster treasury cycles and lower collateral friction for participants.

6) Regulation starts to harden the perimeter

US regulatory steps in 2025 and follow-on guidance in 2026 have been clarifying expectations around stablecoin issuers (reserve backing, permissible activities, constraints around yield-like features), pushing stablecoin rails toward regulated financial-market infrastructure.

7) Micro-transactions become economically viable

Stablecoin-native batching and gasless execution designs make sub-cent payments realistic, enabling pay-per-inference, pay-per-call, and metered software business models that are awkward on cards.

8) A new trust layer forms (identity, reputation, Sybil defense)

Identity registries such as ERC-8004-style approaches aim to standardize agent identity and reputation, reducing merchant impersonation and Sybil risks in autonomous commerce.

9) Compliance-first orchestration emerges (CPN)

The Circle Payments Network (CPN) positions itself as an orchestration layer for institutions, embedding compliance requirements (for example Travel Rule data) and real-time FX into stablecoin payment flows.

10) One unified transaction stack replaces “two lanes”

The industry is converging on a layered model where retail checkout and API/services transactions share the same primitives: discovery, authorization/mandates, credentials, settlement, identity, and dispute or recourse mechanisms.

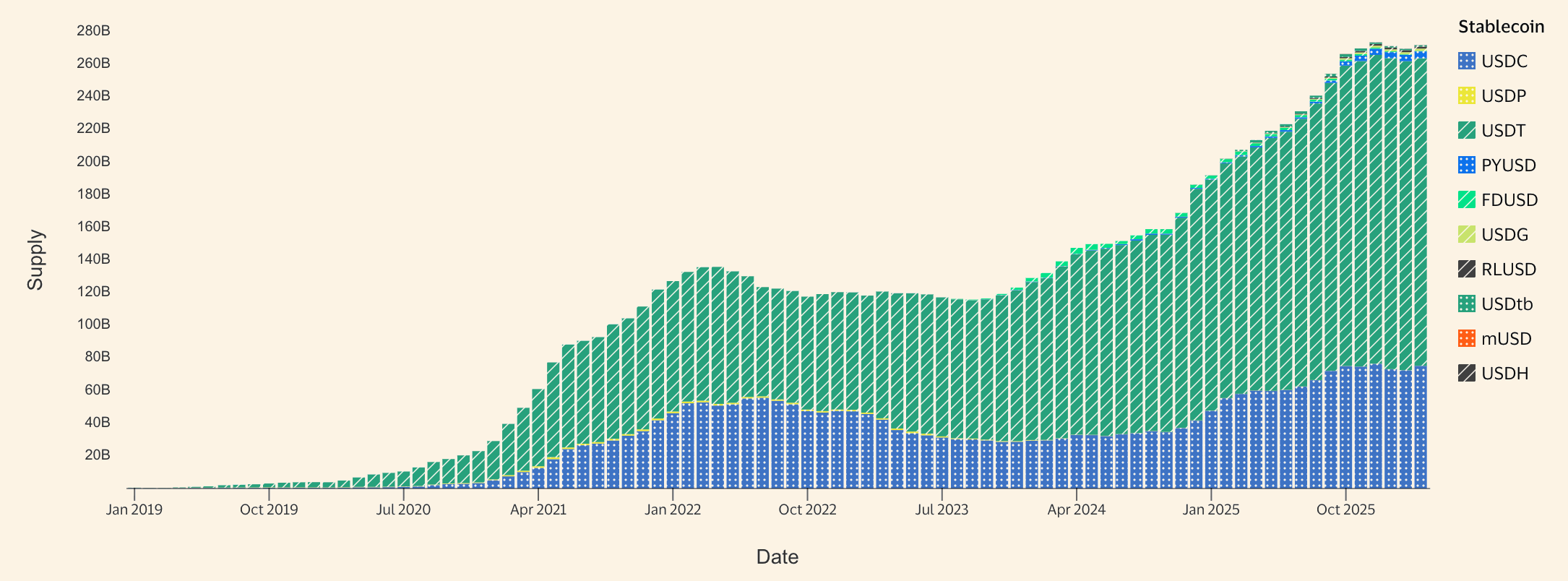

Stablecoin Rails

By 2026, stablecoins, especially USDC, are increasingly treated less like speculative crypto assets and more like programmable settlement infrastructure. In practice, they function as on-chain bearer instruments whose movement and conditions of release can be enforced in software, which makes them useful as a settlement layer for both institutions and machine-native commerce.

Why stablecoins work as a settlement layer

The advantages can be framed as four concrete properties:

Deterministic finality

On fast-finality networks, transfers can reach irreversible finality in sub-second time, reducing the operational uncertainty that comes with probabilistic settlement models.

7-day settlement

Stablecoin rails support continuous settlement, including weekends and holidays. For banks and payment intermediaries, this can reduce reliance on large pre-funding buffers used in correspondent and multi-hop settlement.

Atomic FX inside the payment flow

Orchestration layers such as CPN, paired with stablecoin issuance across multiple currencies, support RFQ-driven FX that can be executed during the payment itself. This enables atomic swaps like USDC to EURC as part of a single transaction flow, rather than a separate treasury step.

Conditionality plus escrow-by-default

Stablecoins can be locked in escrow and released only when a defined condition is met, for example cryptographic proof that a task completed. This is especially important for machine commerce, where payment and fulfillment can be tightly coupled.

Stablecoins under existing payment UX

The largest stablecoin adoption in 2026 is often invisible to end users. In this model, stablecoins are used for institutional settlement while the consumer experience remains card-native.

For example, Visa’s USDC settlement expansion is designed so issuer and acquirer partners can settle certain obligations in USDC while keeping the consumer card experience unchanged. The front end still benefits from familiar consumer protections and disputes, while the back end liquidity movement becomes faster and can operate on a near-continuous basis.

“So what” implications

For banks: Stablecoin-native settlement shifts operations from limited weekday windows to near-continuous availability, materially improving treasury management, liquidity ops, and automated reconciliation.

For merchants/platforms: To capture agent-driven demand, merchants need deterministic, machine-readable interfaces (UCP-style manifests). Discovery, comparison, and routing increasingly happen agent-to-agent, not human-to-browser.

For AI agent builders: The center of gravity moves to auditability. Embed verifiable intent (AP2 mandates + credentials) into runtimes so actions are attributable, constrained, and regulator and network compliant.

Direct stablecoin payments and the dispute gap

Direct stablecoin pushes, including API-native flows like x402, introduce a core challenge: blockchain transfers are final by default and do not include native chargeback mechanisms. To match card network expectations at the point of interaction, additional layers have to carry “recourse”.

Three emerging approaches show up repeatedly:

Reputation-based liability

Instead of legal chargebacks, failures are handled through an identity and reputation layer. If a provider takes payment and fails to deliver, the buyer agent can submit evidence, and the provider can be penalized via reputation loss or exclusion from future agent traffic.

Refund and reversal protocols

A second path is smart-contract mediated refunds, where a refund flow is standardized and enforceable on-chain. Some ecosystem proposals also explore reversible transactions in institutional contexts, especially where compliance and participant permissions are stronger.

Verification predicates with escrow release

For higher-value B2B and B2C flows, the design often shifts to escrow-first. Funds are released only when explicit verification predicates are satisfied, for example a Proof of Task Execution that meets a pre-agreed condition set.

Definitions and the Unified Agentic Transaction Stack

The emergence of agentic commerce necessitates a single conceptual framework that accounts for the diverse requirements of retail checkout and metered machine services. In this model, the “Agentic Transaction Stack” provides a layered approach where each level handles a specific aspect of the economic exchange, regardless of the fulfillment type.

Agentic commerce is the paradigm in which autonomous software agents complete the entire business lifecycle—from discovering callable services to assessing counterparty credibility, placing orders, and finalizing settlement—without required step-by-step human intervention, yet remaining anchored to a verifiable human mandate.

The Layered Agentic Transaction Stack

The stack is composed of six distinct layers, each providing a critical service to the autonomous economy.

Mapping Unified Flows: Retail Checkout vs. Metered Services

The following table demonstrates how seemingly disparate use cases map onto the identical layers of the unified stack.

The core difference between these two flows is not the architecture, but the parameterization of the layers. For retail, the stack is tuned for high-protection and moderate-latency. For machine services, the stack is tuned for high-velocity and finality-by-default.

Trust and Identity

In an autonomous economy, institutional adoption depends on one hard requirement: being able to prove that a specific, legitimate human approved a specific spend. Without that proof, enterprises cannot satisfy audit, risk, and compliance thresholds, no matter how good the agent UX becomes.

Operationally, a “Trusted Agent” is not just reliable software. It is a cryptographically attested identity that is recognized by payment networks or formal rails, bound to the exact merchant and checkout context to prevent replay or redirection, and anchored to a human delegation event (for example via a passkey/FIDO2) so the mandate is durable and non-repudiable.

The ecosystem is converging toward an ERC-8004-style trust stack built from portable identity, reputation signals, and independent validations (re-execution, zkML, TEEs, or oracles) so trust can scale with value at risk. The unresolved gap is legal accountability: mapping cryptographic agent identity to a legally responsible entity. Even as stablecoin issuers become more regulated, agent liability remains governed in practice by Merchant-of-Record structures and by audit trails (such as AP2-style mandates) that determine whether an action was truly “authorized” in the legal sense.

Where Stablecoins Actually Win

Useful frame comes from Noah Levine, Partner at a16z crypto, who argues that the “stablecoins vs cards” debate is often the wrong fight: cards will likely keep winning most agent-driven consumer commerce because they bundle credit, fraud tooling, and dispute rights, while the real stablecoin wedge opens where new merchants and services are too risky, too ephemeral, or too early to be underwritten.

The timing matters because the supply of these “non-traditional merchants” is now exploding: GitHub reported 36 million new developers joined in 2025, and YC publicly noted that about a quarter of the W25 batch had codebases that were 95% AI-generated, which is a proxy for how fast new software supply can appear and iterate.

At the same time, platforms like Bolt are pulling non-developers into production software creation, accelerating the formation of tiny, informal “micro-merchant” services that can sell functionality directly over an API rather than through a website or a sales process. In that world, the constraint is not settlement speed, it is underwriting and recourse: if a service has no operating history, unclear ownership, and unstable uptime, traditional processors are rational to say no because chargeback liability and fraud risk must land somewhere.

Levine’s point is that stablecoins win in the gap, not because they are “better than cards,” but because they are better than not getting paid at all for the long tail of unreliable, newly created services. This shifts the forward-looking question from “Which rail is cheaper?” to “Which stack can score reliability, bind identity, and price risk before an agent sends irreversible money?” The next phase of agentic commerce will be won by systems that make three things legible to machines: a verifiable merchant identity, a verifiable user mandate, and a verifiable fulfillment signal.

Where those proofs are weak, the market will default to escrow patterns, policy wallets, reputation systems, and facilitator models that can absorb risk and gradually graduate merchants into card-like protections. Where those proofs become strong, stablecoin settlement can behave like a native machine primitive, enabling new unit economics like pay-per-call and pay-per-inference without requiring a merchant account on day one. The core implication is subtle but decisive: the long-run opportunity is not disintermediating Visa or Mastercard, it is building the missing trust and underwriting layer for the millions of new “merchants that do not exist yet,” so agents can safely route value to them at internet speed.

Adoption Signals and Near-Term Roadmap

As of March 2026, the market is no longer being driven mainly by narratives. We now have production deployments, tagged specs, and institutional pilots that indicate real adoption.

Primary evidence of institutional adoption

1) Public specs have moved from drafts to tagged releases

UCP 1.0 (Jan 2026) and AP2 v0.1.0 (Sep 2025) progressed into versioned, published releases on GitHub, signaling stabilization of interfaces and naming conventions.

2) Live volume and usage are material

Visa reported monthly stablecoin settlement volume at a $3.5B annualized run rate as of Nov 30, 2025, rising to ~$4.5B annualized by mid-Jan 2026 (per Reuters reporting).

x402 launched in May 2025 to embed payments directly into HTTP via the long-unused 402 status code. Within months, it processed 100M+ payments across APIs, apps, and AI agents, enabling paid API calls and autonomous on-demand purchases of compute and data.

3) Institutional pilots are no longer theoretical

Mastercard completed live AI agent payment activity in Singapore with DBS and UOB.

Visa expanded its USDC settlement pilot to include Cross River Bank and Lead Bank on Solana, increasing the set of real institutional participants.

4) Embedded product launches are reaching consumers

OpenAI’s “Instant Checkout” in ChatGPT is an early mass-market implementation of the Agentic Commerce Protocol (ACP) and Stripe Shared Payment Tokens, pushing agentic checkout into a mainstream interface.

5) Regulatory posture is hardening into implementation

The OCC Bulletin 2026-3 (Feb 25, 2026) represents formal implementation steps tied to the GENIUS Act, reinforcing the direction that stablecoin issuers are being treated as part of core financial infrastructure.

2026 near-term outlook

Standardization accelerates at the “Discovery” and “Grammar” layers

By end-2026, expect merchants to push toward common standards (UCP and adjacent agent connectivity layers such as MCP) to reduce the cost of supporting multiple AI platforms and runtimes.

Fragmentation persists at “Trust” and “Reputation”

Identity and trust registries are still up for grabs. Competition is likely to continue between:

Network-led models (Visa, Mastercard) that extend card-era identity and liability frameworks into agents

Decentralized approaches (including ERC-8004-style registries) that push on-chain reputation and composable identity primitives

A durable two-track reality emerges

Business Governance Track (tokenized cards, fiat rails): likely to dominate most retail goods and consumer commerce due to embedded chargebacks, fraud protections, and mature liability regimes.

Native Settlement Track (stablecoins via x402-like patterns): likely to dominate the machine economy and high-frequency API markets where instant finality and sub-cent economics matter more than consumer dispute frameworks.

Additional: System Reference Architectures

To operationalize the unified model, we focus on concrete message flows. The business logic shifts, but the underlying primitives stay consistent: discovery, authoritative state, verifiable intent, credential delegation, and a verifiable settlement event.

Flow 1: Agent-Mediated Retail Purchase With Consumer Protection

Goal: A consumer-facing agent completes a retail purchase on behalf of a user while preserving chargebacks, fraud protection, and the existing card dispute stack through tokenized card rails.

Merchant capability discovery (UCP)

The agent retrieves the merchant’s UCP manifest from

/.well-known/ucp. The manifest advertises supported capabilities (for exampledev.ucp.shopping.checkout) and available payment handlers (for example Stripe, Shop Pay).Authoritative checkout state (Merchant of Record)

The agent calls the merchant’s commerce API to build a cart. The merchant remains the Merchant of Record (MoR) and returns an authoritative checkout object: line items, taxes, shipping options, total amount, and expiry rules.

Mandate generation and purpose binding (AP2)

If AP2 is supported, the checkout response includes a merchant signature that commits to the terms (price, items, delivery, refund policy references). The user reviews the cart in a trusted UI and approves via a strong authenticator (for example passkey/biometrics), producing a cryptographically bound Cart Mandate.

Credential delegation (Stripe SPT + network tokens)

The agent requests a Shared Payment Token (SPT) from the user’s wallet. Stripe provisions a scoped network token (Visa or Mastercard) aligned to the user’s mandate constraints. The agent receives a usable payment credential abstraction, never the raw PAN.

Execution and settlement (card rails, modernized treasury)

The agent submits to the merchant’s

/completeendpoint, attaching:

the SPT (credential token), and

the user-signed Cart Mandate (intent proof)

The merchant charges via its standard card integration (for example Stripe). Settlement runs on card rails, with optional stablecoin settlement between participating institutions where supported (treasury modernization), without changing the consumer-facing protections.

Dispute evidence packet (non-repudiation)

If a dispute occurs (non-delivery, misrepresentation), the signed Cart Mandate plus the merchant-signed checkout commitment form an auditable, non-repudiable evidence trail for issuers and network arbitration.

Key property: The agent never handles raw credentials, and disputes remain possible because the transaction terminates in the card network’s protection framework.

Flow 2: Paid API Request Using HTTP-Native Payments

Goal: An autonomous agent pays per request for a computational or data resource using web-native primitives, where the unit of sale is an HTTP call.

Initial request and challenge (HTTP 402)

The agent sends a normal HTTP request to a protected API endpoint. The server responds with

402 Payment Required.Discovery of payment requirements

The response includes a

PAYMENT-REQUIREDheader (or equivalent metadata) specifying:

price (for example

0.10 USDC),network (for example Solana), and

payToaddress (recipient)

Intent check and payload construction (mandate enforcement)

The agent’s policy wallet checks the request against a pre-approved Intent Mandate for that provider (limits, spend caps, allowed endpoints). If compliant, it constructs and signs a payment authorization payload (for example EIP-712-style typed data) that matches the server’s requested terms.

Retry with proof (payment signature header)

The agent retries the same HTTP request, now including a

PAYMENT-SIGNATUREheader carrying the signed authorization payload.Verification and finality (facilitated execution)

A third-party facilitator (for example an institutional developer payments platform) verifies the signature off-chain and executes the on-chain transfer, sponsoring gas to keep UX fast and enable sub-cent economics.

Delivery and confirmation (settlement receipt)

The server returns

200 OKwith the requested data and aPAYMENT-RESPONSEheader containing a settlement receipt (for example a transaction hash).

Key property: No merchant account onboarding is required; the payment is embedded in the HTTP interaction and terminates in an on-chain settlement event.

Final perspective

Rewiring the transaction lifecycle for software agents is a structural shift. By 2026, the performance of a financial institution, merchant, or platform increasingly depends on whether it can interoperate across the Agentic Transaction Stack (discovery, authorization/mandate, credentials, settlement, identity, and recourse).

Stablecoins are emerging as a form of programmable settlement logic that legacy fiat ledgers do not natively provide. The main execution risk over the next 18 months is governance lag: autonomous systems will scale faster than the liability, identity, and audit frameworks required to constrain them safely.

Sources:

https://developers.googleblog.com/under-the-hood-universal-commerce-protocol-ucp

https://www.occ.treas.gov/news-issuances/bulletins/2026/bulletin-2026-3.html

Cover Artwork

Landscape with Merchants

Claude Lorrain, c. 1629

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.

a lot to take in but the noah levine framing is the most useful part: stablecoins don't beat cards, they just serve the merchants cards won't touch.