Stripe’s Stablecoin Strategy

This month, Stripe finalized the $1.1 billion acquisition of Bridge. This strategic move signals Stripe’s commitment to blockchain-based payments, positioning it as a key player in the evolving digital finance landscape. Stablecoins (now a $200 billion market) have become integral to global transactions, powering nearly 50% of cross-border digital payments.

With projections pointing to $400 billion in market cap by year-end, Stripe’s integration of Bridge’s technology enables instant, low-cost settlements, enhancing merchant payouts and global transfers while competing with PayPal, Visa, and Circle. As regulators develop stablecoin frameworks, Stripe’s move highlights a broader shift: fintech giants adopting blockchain to enhance, rather than disrupt, traditional finance. The following paper, prepared by our team, examines the implications of Stripe’s stablecoin strategy, its role in the payments sector, and its impact on financial inclusion and institutional adoption.

1. Introduction

Founded in 2010 by Patrick Collison and John Collison, Stripe has become a leading force in fintech, renowned for its developer-centric payments infrastructure that powers businesses worldwide. By 2024, businesses using Stripe handled $1.4 trillion in payment volume (up 38% year-over-year) – an amount equivalent to ~1.3% of global GDP. Stripe’s client base spans from startups to large enterprises, including half of the Fortune 100 and 80% of top cloud and AI unicorns. After over a decade in online payments, Stripe has expanded into billing, treasury, and other financial services. Notably, Stripe turned profitable in 2024 and has heavily reinvested in R&D, far above industry peers. This strong financial footing allows Stripe to pursue emerging technologies like stablecoins and AI, which management sees as transformative forces reshaping the payments landscape.

Stripe’s relationship with crypto has come full circle. In 2018, Stripe withdrew support for Bitcoin payments due to volatility and low usage. But by 2022, Stripe re-entered crypto via partnerships – piloting USDC (USD Coin) payouts on Polygon to allow creators to receive earnings in stablecoin.

Stripe’s approach has been to abstract away blockchain complexity for users: “Stripe will handle all crypto-related complexity… platforms can avoid storing or transferring crypto themselves,” the company noted in its crypto payout launch.

In early 2024, Stripe declared “Crypto is back,” launching support for stablecoin payments (USDC and PayPal’s PYUSD) within its products. This return to crypto was driven by customer demand for faster, global payout options. By positioning stablecoins as just another currency within Stripe’s infrastructure, Stripe signaled its belief that Web3 technologies can integrate into mainstream finance seamlessly.

Stablecoins 101 – Role in Modern Finance

Stablecoins are cryptocurrencies pegged to stable assets (usually 1:1 to a fiat currency like USD). This peg allows them to combine the price stability of traditional money with the efficiency of crypto networks. In practice, stablecoins serve several critical roles:

Cross-Border Payments: Stablecoins enable near-instant, 24/7 cross-border transfers at low cost, without relying on correspondent banks. This is transformative for remittances and global business payments – using stablecoins can cut average remittance costs by ~4.5% compared to traditional channels. For example, a freelancer in Nigeria can receive USD stablecoins from a U.S. client in minutes and convert to local currency, bypassing high bank fees and delays.

DeFi and Liquidity: Stablecoins are the lifeblood of crypto trading and decentralized finance. They provide a stable medium of exchange and store of value on blockchain platforms. As of 2024, stablecoins were involved in over 30% of Ethereum transactionsand serve as the primary trading pair for cryptocurrencies, accounting for the main source of liquidity on exchanges. This deep liquidity anchors the DeFi ecosystem, allowing lending, borrowing, and trading without touching fiat.

Financial Inclusion and Dollarization: In countries facing high inflation or limited banking access, stablecoins offer an accessible dollar-based alternative. Users in Latin America, Africa, and elsewhere increasingly hold savings in USD-backed stablecoins to preserve value. They also facilitate e-commerce and microlending in regions where credit cards or PayPal aren’t widely available. By 2024, stablecoin usage in emerging markets had surged, with global adoption up 22% year-on-year driven largely by demand for inflation-resistant digital dollars.

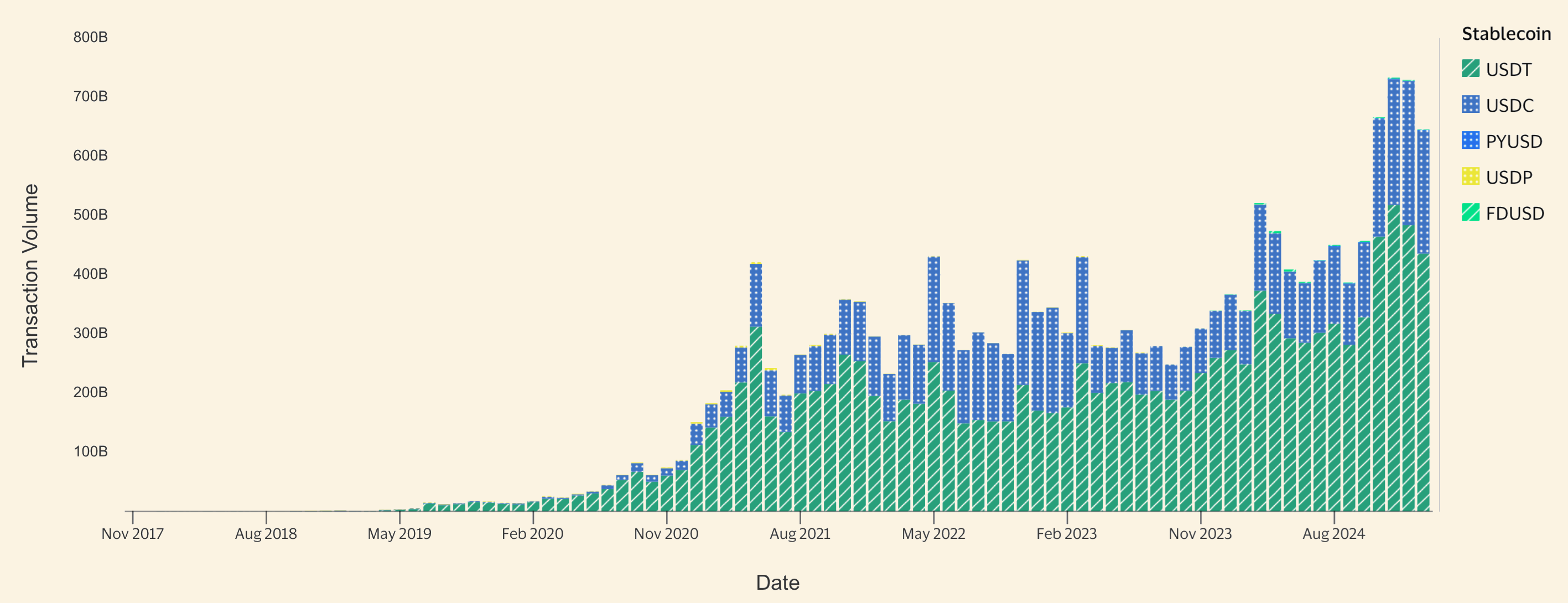

Stablecoin Market Size & 2025 Trends

The stablecoin market has grown from niche to a significant piece of the financial system. In late 2024, the total stablecoin market cap surpassed $200 billion for the first time, exceeding the previous peak from the 2021–22 crypto boom. This growth resumed as crypto markets recovered and more businesses adopted stablecoins for payments. Tether’s USDT – the largest stablecoin – reached a record

$139 billion in circulation, while Circle’s USDC stood near $41 billion, together dominating the space. Industry forecasts are optimistic: asset manager Bitwise predicts the stablecoin market could double to $400B in 2025 with the help of clear U.S. regulations. Beyond raw market cap, usage metrics show stablecoins gaining mainstream traction.

Over 70 countries now accept stablecoin payments in some form (either via exchanges or merchant platforms), and global stablecoin transaction volumes average $7B daily. Even payment giants are onboard – Visa expanded stablecoin settlement to the Solana blockchain in 2023 to speed up cross-border card payments, and Mastercard is piloting stablecoin integration for bank partners. Regulators, in turn, are intensifying scrutiny to ensure stablecoins are safely managed.

Why Stripe is Betting on Stablecoins

In this context, Stripe’s move into stablecoins is a logical extension of its mission to “increase the GDP of the internet.” Stablecoins can dramatically improve the speed and reach of online commerce – especially cross-border. By eliminating intermediaries, a stablecoin transaction can settle in seconds for pennies in fees, whereas a traditional international wire might take days and cost 5–10% in forex and banking fees. For Stripe, integrating stablecoins promises to unlock new markets and use cases (e.g. paying out sellers in countries where Stripe can’t easily send funds via banks) and to future-proof its platform as finance becomes more blockchain-powered. Importantly, Stripe can incorporate stablecoins without changing its user experience: merchants can price in USD as always, and under the hood Stripe can convert and deliver funds via stablecoin rails if that’s more efficient. In Stripe’s 2024 annual letter, the founders specifically highlighted stablecoins (alongside AI) as innovations that will “reshape the landscape” of payments in coming years. Expanding into stablecoin-powered payments aligns with Stripe’s strategy of offering a comprehensive financial toolkit for businesses – from card processing to treasury management – now augmented by crypto capabilities.

2. The Bridge Acquisition

In February 2025, Stripe completed its acquisition of Bridge (also referred to as “The Bridge”), a startup specializing in stablecoin infrastructure. This section provides an overview of Bridge’s technology and business, as well as the details of its fundraising and why it was a compelling target for Stripe.

Bridge is an API-first platform that enables developers and businesses to integrate stablecoin transactions into their applications with minimal effort. In essence, Bridge provides “stablecoin payments as a service”. A company can plug into Bridge’s APIs and gain the ability to send, receive, and convert stablecoins without having to build any blockchain plumbing themselves.

Key capabilities of Bridge

Multi-Currency Stablecoin Support

Bridge supports a range of major USD-backed stablecoins (USDC, USDT, PYUSD, etc.) and can interface with multiple blockchain networks (Ethereum, Solana, Polygon, among others). This allows customers to transact in whatever stablecoin or chain is most convenient, while Bridge handles the interchange. The platform also supports issuance of new stablecoins – meaning a business could create its own branded stablecoin or digital dollar through Bridge’s system. This issuance capability is akin to providing a private-label stablecoin mint, backed by reserves, which some fintechs or marketplaces might use for loyalty or internal purposes.

Orchestration & Conversion

A standout feature of Bridge is its ability to orchestrate complex money flows involving both fiat and crypto. For example, a U.S. company can use Bridge to pay a vendor in Mexico: dollars are converted to USDC, transmitted abroad, and optionally converted to local currency on the other end – all via Bridge. The platform handles on/off-ramps in various countries, connecting to local banks, mobile wallets, or cash-out services. Bridge has built relationships with regional payment processors (e.g. exchanges like Bitso in Latin America and fintechs like Yellow Card in Africa) to facilitate last-mile conversions. It essentially bridges (hence the name) the stablecoin world and traditional finance, so the end-recipient can receive value in whatever form they need (be it stablecoin or local fiat).

Speed and Cost Efficiency

By leveraging crypto rails, Bridge enables near real-time settlement. Transactions that might normally take days (through correspondent banks or wire transfers) can occur in seconds using stablecoins. Costs are also reduced – stablecoin transfers typically cost a fraction of equivalent bank fees, especially for cross-border payments.

Bridge’s Head of Revenue, Marco Mahrus, described this as building a new global framework atop existing financial systems: one where “no one will go back to…wait for SWIFT or wire transactions during bank hours” once they experience always-on digital dollar payments. This resonates with businesses that operate globally and need to move money 24/7.

Use Cases and Clients

Before acquisition, Bridge had already proven demand for its platform with an array of use cases:

Corporate Treasury: Notably, SpaceX was a Bridge client using stablecoins for global treasury management. SpaceX employed Bridge to convert and transfer funds across borders, leveraging stablecoins as an efficient medium. This real-world usage by a top private company underscores the traction stablecoins have gained outside of crypto trading.

Payouts and Payroll: Bridge was used by platforms like Airtm (a digital wallet) to pay gig workers and contractors worldwide in stablecoins. In one example, a data labeling firm uses Bridge to pay hundreds of remote freelancers; workers can choose to hold the stablecoins or convert to local cash via Bridge’s integrations. Such use cases demonstrate stablecoins’ utility in the global digital economy, enabling work opportunities across borders with less friction in paying out small amounts.

Fintech and Exchanges: Bridge partnered with fintech apps targeting emerging markets (including some in Africa and LatAm) to offer USD savings and payments. For instance, it worked with exchanges like Bitso to power a MXN-to-USD stablecoin remittance corridor for Mexican businesses. It also engineered conversions between different stablecoins for clients like Coinbase (e.g. swapping USDT on Tron to USDC on Coinbase’s Base network)– showcasing its interoperability across crypto ecosystems.

Humanitarian and Government: According to Bridge, even aid organizations and a U.S. government entity tapped its services for fast distributions. Stablecoins can be particularly useful for disaster relief or foreign aid, where getting funds to recipients quickly and transparently is critical. Bridge’s compliance and conversion features would allow an aid agency to send out stablecoin-based aid and recipients to cash out in local currency where needed.

Fundraising, Investors & Valuation Trajectory

Bridge emerged from stealth in 2024 with significant backing. Below is a breakdown of its funding history and key backers:

Seed Funding (Early 2022): Bridge was founded in April 2022 by Zach Abrams and Sean Yu, who were alumni of Coinbase and Square (Block). They had previously built a payments startup (Evenly) acquired by Square. Bridge’s seed financing in 2022 was not publicly announced in detail, but it included crypto-focused investors. Notably, 1confirmation participated, and a boutique fund called Department of XYZ (founded by Matt Homer, former NYDFS regulator who oversaw stablecoin policy) provided guidance on compliance. Jonathan Golden, a former Airbnb/Stripe product manager turned fintech investor, was also an angel backer.

Series A (Mid 2024): In August 2024, Bridge publicly launched and announced a $40 million Series A funding round. The round was co-led by top-tier venture firms Sequoia Capital and Ribbit Capital, with participation from Index Ventures and Haun Ventures (Katie Haun’s crypto fund). Also joining were fintech-focused funds like Oak HC/FT and earlier supporters (1confirmation, Department of XYZ, and others).

In total Bridge had raised $58 million by this point, since some seed funds were previously unannounced. The post-money valuation was about $200 million in this Series A. Achieving a $200M valuation within ~2 years of founding reflected investors’ conviction in Bridge’s technology and market fit. In fact, Sequoia revealed that by the time of the Series A, Bridge had already hit a $5 billion annualized payment volume run-rate, generating an estimated revenue of $5–12 million (assuming a 0.1–0.25% fee take) – impressive early traction that helped justify the valuation.Acquisition by Stripe (Oct 2024–Feb 2025): Rumblings of Stripe’s interest in Bridge began in October 2024. TechCrunch founder Michael Arrington broke the news that Stripe was in talks to buy Bridge for around $1+ billion.

By late October, Stripe’s CEO Patrick Collison tweeted about stablecoins as “room-temperature superconductors for financial services,” hinting at the strategic rationale.

The deal was confirmed and officially announced in February 2025 for $1.1 billion. At 5.5× the Series A valuation (within less than a year), this price underscores how critical Stripe deemed Bridge’s capabilities. It’s one of the largest crypto-related M&A deals to date, surpassing even some notable crypto acquisitions in prior years. For Stripe – still a private company – such a billion-dollar purchase is a major investment, on par with what an IPO-sized war chest might be used for. The acquisition was a mix of cash and stock (details undisclosed), and it brought Bridge’s ~45 employees onto Stripe’s team.

3. Strategic Rationale for Stripe

First and foremost, acquiring Bridge instantly gives Stripe a fully-built stablecoin capability rather than having to build one in-house over years. Stripe is famous for its developer APIs and could have attempted to develop a stablecoin API from scratch. However, the crypto domain – with its rapidly evolving protocols, regulatory hurdles, and need for specialist talent – posed a steep learning curve. Bridge brought a proven product and a team already steeped in both crypto and payments.

As an Architect Partners fintech report noted, “this single acquisition allows Stripe to immediately become a major contender in digital asset-based payments”.

In one stroke, Stripe obtained technology to support instant, global stablecoin transactions and a team experienced in running them at scale. Given that Bridge was already moving billions in volume for clients, Stripe could integrate the tech with far less risk than a greenfield project.

Payments Network

Stripe’s vision has always been to be the one-stop infrastructure for moving money online – from credit cards and bank debits to local payment methods. Stablecoins are emerging as the next rail in global payments, akin to a new kind of payment network that operates alongside Visa, SWIFT, and ACH. By integrating stablecoins, Stripe expands its coverage. A business on Stripe can eventually accept a payment from a customer’s crypto wallet or pay out earnings to a user’s stablecoin wallet, all through Stripe’s interface. Bridge’s API will likely be woven into Stripe’s existing products:

Stripe Connect & Treasury: Stripe Connect (used for marketplace payouts) can use Bridge to payout platform sellers or gig workers in stablecoins if desired, reaching users in countries where direct bank payouts are slow or costly. For example, an African ride-sharing app using Stripe could pay drivers in USDC instantly overnight, something not feasible with traditional banks. Stripe Treasury (which offers stored-value accounts to businesses) could allow holding stablecoin balances or swapping between fiat and stablecoin with one click. These features make Stripe’s ecosystem more powerful for global businesses.

Cross-Border Payments: Stripe could route international transactions through stablecoins to optimize speed and fees. If a customer in Brazil pays a US merchant, Stripe might internally convert the payment to a USD stablecoin, transmit it via blockchain instead of correspondent banks, then credit the U.S. merchant – compressing settlement time from days to seconds.

Neetika Bansal - Stripe’s business lead noted that stablecoin infrastructure is already making a “big impact” and “will play a critical role in turbocharging cross-border commerce”.

This hints at Stripe using Bridge to offer faster cross-border payout products, possibly competing with traditional remittance providers.

New Merchant Services: We may see Stripe offer an option for merchants to accept stablecoins from customers. Today, Stripe primarily processes traditional currency payments (card, bank, etc.) and then pays merchants in fiat. With Bridge, Stripe can act as a two-way bridge: not only paying out, but also accepting stablecoin payments on behalf of merchants and converting them to fiat. This would put Stripe in direct competition with crypto payment gateways (like BitPay or Coinbase Commerce), but with a huge advantage – integration into Stripe’s widely used checkout APIs and dashboards. A merchant could tick a box to “accept crypto”, and Stripe/Bridge would handle the stablecoin acceptance and conversion behind the scenes, settling in the merchant’s currency of choice. Such a service would attract crypto-centric customers to Stripe’s merchants while insulating merchants from crypto volatility (since stablecoins hold value and are auto-converted).

Corporate and Treasury Solutions: With Bridge’s tech, Stripe can cater to enterprise treasury needs. Big companies like SpaceX have already used Bridge for treasury ops; now Stripe could generalize that into a corporate product. For instance, a multinational could use Stripe to park funds in a USD stablecoin to hedge local currency risk, or to make intra-company transfers across borders on weekends. Stripe could even facilitate yield generation on stable cash (via DeFi lending or custody solutions) for clients, venturing toward fintech-meets-DeFi territory.

Competitive Positioning

The fintech and payments landscape is in an arms race to integrate crypto capabilities, and Stripe’s Bridge acquisition vaults it ahead in several dimensions:

PayPal and Traditional Players: PayPal made headlines in 2023 by launching PYUSD, its own U.S. dollar stablecoin, in partnership with Paxos. PayPal’s strategy is to leverage its vast consumer base (over 400 million accounts) to push stablecoin usage for payments and transfers. By end of 2025, PayPal aims to have 20 million+ merchants using PYUSD for payments or settlement. Stripe, however, serves a developer-driven audience and thousands of online platforms that collectively reach hundreds of millions of users as well. With Bridge, Stripe can offer a multi-stablecoin, network-agnostic solution (supporting USDC, USDT, PYUSD, etc.), which might be more flexible than PayPal’s single-coin approach. Moreover, Stripe’s core competency is providing infrastructure rather than consumer wallets, meaning it can power stablecoin transactions for many other fintechs and apps behind the scenes. In effect, Stripe could become the default backend for stablecoin payments across the web, whereas PayPal might focus on its own front-end ecosystem. This positions Stripe both as a competitor and a potential partner to firms like PayPal, Visa, and others that might tap Stripe’s stablecoin rails in the future.

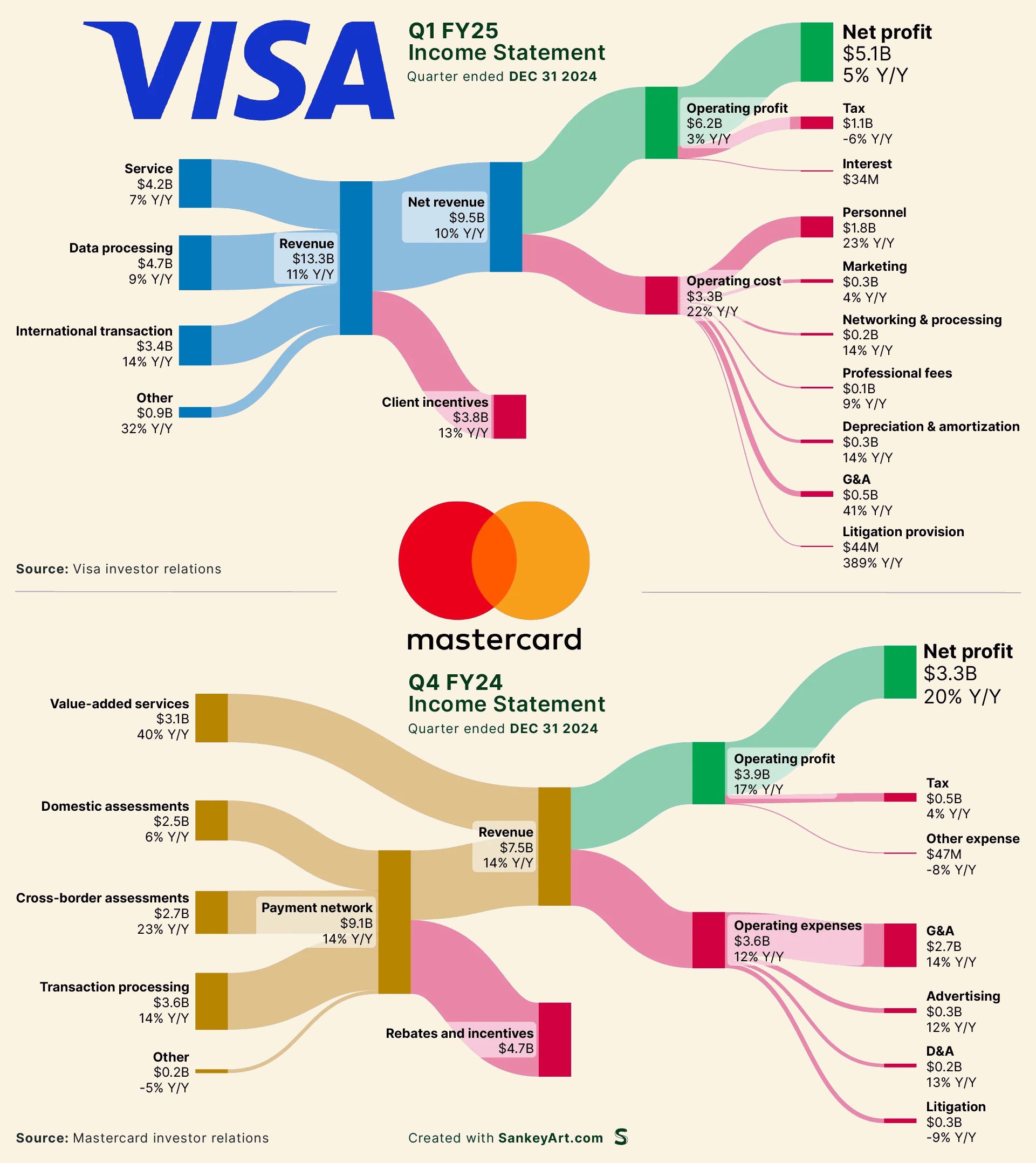

Card Networks (Visa/Mastercard): Visa and Mastercard have been experimenting with stablecoin settlements to improve their own cross-border processes. However, those efforts are largely invisible to end-users (they make the internal plumbing more efficient). Stripe, by contrast, will be exposing stablecoin capabilities to end-users (businesses and developers), effectively disintermediating some functions of the card networks for certain transactions. If a merchant can receive a payment via a stablecoin from a customer’s crypto wallet, that transaction might bypass Visa altogether. On the flip side, Stripe can also collaborate with card networks (e.g. using Visa’s USDC settlement to optimize Stripe’s payout to a merchant’s bank). In any case, having in-house stablecoin tech gives Stripe strategic optionality – it can choose the cheapest, fastest route for each payment (be it ACH, card, or stablecoin) and even blend them. This flexibility could lead to lower costs for Stripe’s clients and pressure on traditional network fees.

Visa & Mastercard - Income Statements Crypto-Native Providers: There are crypto-native companies like Circle (issuer of USDC) and Ripple (with its RippleNet for cross-border payments) aiming to provide services to fintechs and banks. For example, Circle offers APIs for businesses to accept and make payments in USDC, and has partnerships with Checkout.com and others. By acquiring Bridge, Stripe enters this arena aggressively – it can now offer a similar stablecoin API service but bundled with its broader suite (fraud prevention, identity verification, etc.). Stripe essentially internalizes what could have been a partnership with a Circle or a Ripple. It also outflanks smaller crypto payment processors. Few of those crypto startups have the trust and existing customer base that Stripe has. Now that Stripe can offer crypto payouts, a Web3 startup or a global marketplace has less reason to integrate a specialist provider; they can stick with Stripe for both fiat and stablecoin needs.

Stripe’s Motivation – Key Drivers:

Why was Stripe willing to pay over a billion dollars for Bridge?

Customer Demand for Faster Global Payments: Stripe powers many international businesses (SaaS companies, online marketplaces, gig platforms). These customers have pain points that stablecoins can solve – whether it’s paying a remote contractor in a country with limited PayPal coverage, or instantly moving funds between their own entities across regions. By delivering a stablecoin solution, Stripe addresses those pain points and increases its value to customers, which can improve retention and attract new volume.

Diversification of Revenue Streams: Stripe historically makes money from transaction fees on card payments. Stablecoin transactions have different economics (often extremely low on-chain fees). Stripe can create new revenue streams by charging for stablecoin conversion, custody, or API usage. For instance, Stripe might charge a small basis-point fee for off-ramping a stablecoin to a bank account, or for providing liquidity between currencies. Additionally, stablecoin float (the idle balances) could generate interest income if managed appropriately. With billions potentially flowing through stablecoins on Stripe, even ancillary fees or float interest could be significant. Essentially, Stripe can monetize the crypto flows in ways similar to how it monetizes card flows.

Defensive Move & Ensuring Relevance: If Stripe didn’t embrace stablecoins, others might fill the gap. Startups like Ramp Network or MoonPay are already enabling fiat-to-crypto on-ramps. Even traditional banks are exploring issuing their own stablecoins for settlement. Stripe risked disintermediation in certain emerging use cases (for example, Web3 gaming platforms might bypass Stripe for crypto-native payment solutions). By acquiring Bridge, Stripe ensures it stays the default choice for online businesses, covering both legacy and new forms of money movement. It’s a defensive hedge that solidifies Stripe’s moat against disruption.

Regulatory Readiness: One often overlooked reason to acquire instead of build is regulatory preparedness. Bridge had already secured money transmitter licenses in 22 U.S. states and even set up a regulated entity in Europe (Poland) for crypto activities. This legal groundwork is invaluable and time-consuming to replicate. With Bridge, Stripe gains a compliance framework for handling stablecoins (KYC/AML procedures, licensing, relationships with banking partners for redemption of stablecoins, etc.). Stripe’s leadership likely calculated that as soon as U.S. federal regulation allows stablecoin usage broadly, they want to hit the ground running. Bridge’s team, which included legal and compliance specialists, can help Stripe navigate upcoming laws (such as reserve requirements or registration for stablecoin facilitators). In summary, Bridge accelerates Stripe’s regulatory compliance in crypto by 1–2 years, which in a fast-moving space is a huge advantage.

Plans for Integration and Product Strategy

While Stripe has not publicly detailed its roadmap for Bridge integration (as of early 2025, specific plans were still under wraps), we can infer likely directions:

In the near term, Stripe will probably offer stablecoin payout functionality to merchants and platforms. This could mean an update to Stripe Connect where platforms can choose to pay their users in stablecoin (with Stripe handling conversion). Pilot programs might focus on regions like Latin America, Africa, and Southeast Asia, where stablecoin adoption is high and payout infrastructure is weakest.

Stripe may introduce multi-currency stablecoin settlements for cross-border transactions. A customer pays in one currency and the merchant receives another currency, with Stripe using stablecoins as the bridge for better rates. This could tie into Stripe’s existing FX conversion service but supercharge it with instant settlement.

For developer users, Stripe could expose new API endpoints (essentially rebranding Bridge’s API as Stripe Crypto or similar) so that any application can programmatically send stablecoins to a blockchain address or accept stablecoin payments. This turns Stripe into a competitor to crypto payment APIs like Coinbase Commerce. Given Stripe’s large developer community, this move could accelerate Web2 to Web3 integration across many services.

Security and custody will be a focus: Stripe will need to ensure that handling stablecoins (which are bearer instruments like cash) is done with robust security. It wouldn’t be surprising if Stripe partners with or acquires a custodial wallet provider or integrates hardware security modules to protect private keys for stablecoin transactions. User experience-wise, Stripe might abstract wallets away – e.g., a user could provide a blockchain address for payout, or if they don’t have one, Stripe could generate a custodial wallet for them to claim funds later.

Branding and user trust: Stripe might not expose the “Bridge” brand externally for long; it will likely wrap these features under the Stripe brand (e.g., “Stripe Stablecoin” or part of Stripe’s payments API). However, to institutional clients, Stripe can point to Bridge’s track record and the fact that Coinbase and SpaceX were already customers of this tech, lending credibility that Stripe’s stablecoin services are battle-tested.

Impact on Stripe’s Business (2025 and Beyond)

The acquisition and integration of Bridge could have profound implications for Stripe’s business model:

Stripe’s total addressable market expands. It can now tap into on-chain transaction volumes and potentially serve crypto-native businesses that it couldn’t before. This opens new client segments.

Stripe’s growth may get an extra boost. The company’s payment volume was already growing fast (38% in 2024); with stablecoins, it could grow even faster, or at least capture growth that would have gone to crypto competitors. It’s conceivable that by late 2025, a noticeable percentage of Stripe’s volume could be in stablecoin transactions rather than card swipes. Stripe highlighted that the revenue of businesses on its platform grows 7× faster than the S&P 500 average– stablecoin-enabled businesses (like global marketplaces) might push this even higher.

There may be margin implications. Crypto transactions can be cheaper to process than card payments (no interchange fees, etc.), so Stripe might not earn the same ~2-3% fee as it does on a credit card transaction. However, Stripe can structure fees differently – possibly charging a fixed fee per payout or a small conversion fee. If done well, stablecoin services could be a high margin add-on (since operating the blockchain infrastructure is relatively low cost once set up). Also, by serving more volume and new use cases, Stripe can make up in scale what it loses in per-transaction take rate.

Long-term, Stripe is positioning for a world where finance is hybrid: part traditional, part crypto. Should central bank digital currencies (CBDCs) emerge (e.g., a digital dollar), the infrastructure Stripe gains now with stablecoins could extend to CBDCs. Stripe could easily support a digital euro or digital dollar in the future, having already mastered handling digital fiat equivalents. In this way, the Bridge acquisition is also a hedge on the future of money – whatever form money takes (cards, bank accounts, stablecoins, CBDCs), Stripe intends to be the platform through which it flows.

4. The Future of Stablecoins & Stripe’s Role

With Stripe’s bold entry into stablecoins, it’s worth examining the broader context of where stablecoins are heading and how Stripe might evolve in the Web3 landscape. This section discusses macro trends in stablecoin adoption, regulatory developments, market projections, and potential strategic moves for Stripe going forward.

Macro Trends in Stablecoin Adoption

Stablecoins in 2025 stand at the convergence of traditional finance and crypto. Some notable trends:

Mainstream Institutional Interest: What was once the domain of crypto trading desks is now of interest to Treasurers and asset managers. We see major financial institutions exploring stablecoins – for instance, Bank of America was reported to be researching stablecoin applications for settlement and custody in early 2025. Payment companies are not alone; brokerages and even central banks are analyzing how privately issued stablecoins interact with the money supply.

Emergence of Non-USD Stablecoins: While USD stablecoins dominate (>95% share by market cap), there is growing interest in stablecoins denominated in other currencies (EUR, GBP, JPY) and even commodities (like gold-backed tokens). By 2025, Euro-backed stablecoins and others are slowly rising as regulatory clarity in Europe improves. This could lead to a more multi-currency stablecoin ecosystem. Stripe could down the line support non-USD stablecoins to facilitate, say, Euro-to-Euro on-chain payments for EU merchants, further integrating into local financial systems.

Consumer Payments and E-Commerce: Stablecoins are making inroads into consumer-facing use. Some crypto fintech apps come with debit cards that let users spend stablecoin balances, essentially using stablecoins for everyday purchases. A 2024 statistic noted retail stablecoin usage jumped 35% as more consumers used stablecoins for e-commerce checkouts and money transfers. Projects like Facebook’s (Meta’s) failed Diem aside, the concept of a globally used digital currency is being realized through USDT, USDC, etc., albeit organically. Stripe’s move can further catalyze this – if Stripe enables stablecoin payments at thousands of online shops, consumers might start seeing a “Pay with USDC” option alongside credit cards at checkout in the near future.

DeFi Integration with TradFi: Stablecoins continue to anchor DeFi applications (lending, yield farming, etc., with over $120B TVL in DeFi partly backed by stablecoins). Now TradFi players are eyeing that yield and functionality. For example, fintech startups are offering clients higher yields by putting cash into DeFi via stablecoins (within regulated frameworks). This blurring of lines suggests stablecoins will be treated as a new form of money market instrument in some contexts. Stripe could potentially partner with financial institutions to facilitate safe yield on stablecoin balances for merchants, effectively connecting Stripe clients to DeFi yields under the hood – a speculative but interesting possibility.

Regulatory Landscape

The rapid growth of stablecoins has regulators worldwide crafting rules to mitigate risks and integrate them into the financial system:

United States: The U.S. has been actively debating stablecoin-specific legislation. Key concerns for regulators are ensuring issuers have adequate reserves (to prevent runs), transparency, and guardrails against misuse (e.g., money laundering). A federal Stablecoin Act is expected to gain momentum in Congress in 2025. Such a law could require issuers to be licensed (or even banks), impose audits on reserves, and set standards for redemption. For Stripe, as a facilitator rather than issuer, the regulatory focus will be on compliance with money transmission and securities laws. Stripe will have to ensure any stablecoin it supports is reputable and regulated (thus, we can expect Stripe to primarily use fully reserved, regulated stablecoins like USDC or PYUSD, and be cautious with those like Tether which, while dominant, have faced transparency questions). Stripe may also lobby for clear delineation that payment processors using stablecoins are not the issuers and thus not subject to reserve requirements themselves, aside from normal safeguarding of client funds.

Europe: The EU has already passed MiCA (Markets in Crypto-Assets), a comprehensive framework that covers stablecoins (which it calls “asset-referenced tokens” or “e-money tokens”). MiCA will require issuers of significant stablecoins to be authorized and meet prudential requirements. It also allows stablecoins to be used across all member states once approved. This could standardize stablecoin usage in Europe by 2024–2025. Stripe, with Bridge’s Polish entity registered for crypto activities, is well placed to operate under MiCA. If anything, Stripe can leverage Bridge’s early mover advantage in compliance to confidently expand stablecoin services in Europe, potentially even supporting digital euros or working with European fintechs wanting stablecoin rails.

Developing Markets: In countries like Nigeria, Argentina, Turkey – where stablecoin adoption is high due to volatile local currencies – regulators face a dilemma. Some have placed restrictions on crypto, others are considering their own CBDCs. But even conservative central banks (e.g., in the Middle East and Asia) are acknowledging stablecoins. For instance, Hong Kong and Singapore have published guidelines to integrate regulated stablecoins into their financial hubs. The likely scenario is a patchwork of rules: some jurisdictions will embrace USD stablecoins as a parallel currency for faster remittances, while others might strictly control conversion points. Stripe will have to adapt features on a country-by-country basis (enabling stablecoin payouts only where legal, doing thorough KYC). It may also partner with local licensed crypto firms in regions where it doesn’t want to navigate directly – effectively extending Bridge’s model of connecting to local payment providers.

Projections

By the end of 2025, if bullish forecasts hold, the stablecoin market could approach the size of a Fortune 500 bank in terms of float. Even without doubling, stablecoins are on track to rival the circulation of major national currencies (for perspective, $400B would exceed the money supply of many countries). The implication is that stablecoins will increasingly be used not just within crypto markets but in everyday commerce and finance. The $44 trillion global B2B cross-border payments market that Matt Hougan projected stablecoins could dominate in the next 5 years is a staggering prize. It suggests stablecoins won’t just be peripheral; they could reshape how corporates settle invoices, how banks transfer funds among themselves (some banks might prefer sending stablecoins over using correspondent banking if regulations allow), and how individuals send money abroad. If this scenario plays out, Stripe stands to gain massively: being a facilitator of stablecoin flows in such a large market could position Stripe almost like a next-generation Visa network.

However, one must also consider stablecoin competition: governments might push CBDCs (Central Bank Digital Currencies) as an alternative. A U.S. digital dollar or digital euro could theoretically reduce the need for private stablecoins. But even in that case, Stripe’s platform could just as well handle CBDCs – the technical difference is minor. In fact, governments might rely on fintech middleware like Stripe for distribution of CBDCs. Stripe could then become an important partner in any CBDC rollout (for instance, helping the Fed distribute a digital dollar to businesses). Thus, whether the future is private stablecoins, public CBDCs, or (likely) a mix, Stripe’s role as an intermediary for digital value transfer is assured if it stays at the forefront.

Stripe’s crypto acquisition signals a broader push into Web3. It may deepen partnerships with stablecoin issuers like Circle (USDC) and Paxos (PYUSD), positioning itself as a key on/off-ramp for stablecoins. Expanding beyond stablecoins, Stripe could integrate Bitcoin and Ethereum payments while maintaining a focus on stable-value assets. Developer tools, acquisitions in wallets, security, and compliance, and deeper engagement with regulators could further solidify its role. Ultimately, Stripe is building the infrastructure to dominate crypto payments, much as it has with online transactions.

5. Conclusion

Stripe’s acquisition of Bridge and its broader stablecoin strategy represent a watershed moment in fintech – a signal that the lines between traditional finance and crypto finance are blurring, led by one of the most valued private fintech companies in the world. This concluding section synthesizes the significance of Stripe’s stablecoin foray and what it means for institutional investors and the fintech/crypto sectors.

By embedding stablecoins into its business, Stripe is future-proofing itself for the next decade of payments. Just as Stripe championed mobile and online payments in the 2010s, it is now embracing crypto-native payments to ride the next wave. This could significantly expand Stripe’s economic moat. The company’s long-term revenue growth may increasingly come from emerging markets and new financial services, areas where stablecoins give Stripe an edge. Moreover, Stripe’s valuation (last estimated around $70B in mid-2024) could be bolstered by this move – investors often reward companies that successfully pivot into high-growth areas. If Stripe executes well, it might capture a sizable portion of the stablecoin transaction value floating around, translating into a new growth story on top of its core processing business. This narrative could be powerful going into a potential IPO or next funding round, reassuring investors that Stripe will not be left behind by the crypto revolution but rather help lead it.

Fintech and Crypto Market Impact

Stripe’s stablecoin push is likely to have a ripple effect across both the fintech sector and crypto markets:

In fintech, expect an arms race: other major payment processors like Adyen, Checkout.com, or Square/Block may accelerate their crypto plans. Adyen, for example, might consider integrating stablecoin acceptance to keep up for global merchants. PayPal will certainly double down on PYUSD promotion to not lose mindshare. This competitive dynamic can speed up the adoption curve of crypto in payments significantly in 2025–2026.

In crypto markets, an endorsement by Stripe is incredibly validating. It suggests that the largest “crypto winners” may not just be standalone crypto companies, but could be hybrid players that merge with fintech. Crypto valuations (for relevant projects) could get a boost – indeed, after Stripe’s announcement, stablecoin trading volumes jumped as traders anticipated greater usage. It wouldn’t be surprising if the market cap of leading stablecoins grows faster now, with more real-economy volume backing them. Also, the prospect of a Stripe IPO with a crypto story could excite public market investors about crypto-related equities once again.

Users (businesses and end-consumers) stand to gain the most: more competition and integration mean better services and lower costs. If Stripe and competitors succeed, sending money globally might become as easy as sending an email, fulfilling a long-held promise of digital currency enthusiasts.

Links:

Stripe 2024 Annual Letter (Feb 27, 2025): assets.stripeassets.com

Year End 2024 Crypto M&A and Financing Report: architectpartners.com

Sources:

Stablecoin Transactions (data): visaonchainanalytics.com

*Note: Adjusted Volume from labeled CEX, DEX, or other entities, or addresses with ≤1k transactions or ≤10M transfer volume in 30 days

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer's views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.

Nice read!